The government has to put in extra efforts to achieve its tax collection targets for FY 2019-20, stated by Lok Sabha. As per the data accumulated for the first seven months of the current fiscal year, the direct tax collected and the Goods and Service Tax are 38% and 49.21% respectively of the decided Budget for FY 2019-20.

Anurag Thakur, Minister of State for Finance, in a written reply to Lok Sabha said that the Budget Estimate for direct taxes for FY 2019-20 is ₹13.35-lakh crore. But in the seven months (i.e. From April 1 to October 31), the net collection of direct taxes was ₹5.18-lakh crore. Till now the direct tax collection is approximately 38% of the BE against 44% in the same time period for FY 2018-19.

Goals can be achieved only if the tax collection growth rate is constant at 30% per month for the rest of the year. The GST council meeting held on 20 September 2019 gave its judgment on cutting the corporate tax. This could prove to be a permanent loss of revenue (around Rs. 1.45 Lakh Crore) from the government’s treasury. This provision is a set back in achieving the goals.

As far as the tax collection is concerned, Anurag Thakur said the actual net mop up for the Centre (CGST) was around ₹3.26-lakh crore during the April-October period against the BE of ₹6.63-lakh crore which means the monthly CGST share alone should remain constant to ₹67,000 crores for the rest of the current FY. In the case of the States then the average monthly collection has to remain constant to more than ₹1.10-lakh crore a month for the rest of the year. The figures are hard are quite challenging for the government.

Anurag Thakur further stated that the decreasing or increasing revenue collection with regards to its BE can be calculated only at the end of the financial year. Due to some experts, the downfall in revenue collection is estimated to be more than ₹2-lakh crore after considering the loss of ₹1.45-lakh crore owing to the Corporate tax rate cut.

The slowdown in the economy is one of the prominent reasons for the lower tax collections. Consumption is low having an adverse effect on the GST collection. Since the corporate sector has not been touched, this has resulted in low or no increment in salary for employees. This has led to lower consumption and the increased risk of not being able to achieve tax collection targets.

Filing GST is a massive task involving document compilations, computations, GST calculations, verification and so on. People with deficit knowledge are often seen struggling with GST filing and reviewing the documents for accuracy.

GST invoice is one of the major components used while computing tax, one wrong invoice will affect the figures in GST returns leading to more tax outgo. The particular write-up highlights the importance of revising tax invoices under GST and how to revise a GST invoice for its accuracy.

GST Invoice Tax Introduction

A GST Invoice is basically an electronically generated supply bill issued at the time of goods or service trades. Indexed in a proper GST invoice are issue date, HSN code of the product, SAC code, SGST, CGST, IGST amounts and the final taxable value of the goods and services sold. One must fill all the details accurately in order to get the exact amount of tax that has to be paid and also the amount of credit that has to be availed.

Revising a GST Tax Invoice for Accuracy in Figures

There are probabilities of issuing a wrong GST invoice which if not modified will lead to inappropriate tax outgo. To escape such cases revision of the invoice is needed.

While revising an tax invoice taxpayer may consider:

Downward revision in prices of goods and services that are supplied.

Upward revision in prices of goods and services that are supplied.

Changes in GST rate and so on.

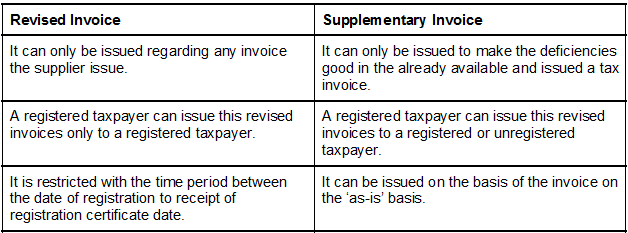

Upward revision of the invoice is possible via a Supplementary invoice and Downward revision can be done via a credit note. In some cases, there is a complete revision in the invoice hence a revised invoice is issued.

Currently, there are no rigid provisions for the revised invoice under GST laws. Registered taxpayers operating in the country are assigned a GSTIN number. Following the completion of the necessary formalities, taxpayers will be assigned a formal registration number under GST.

Starting from the date of execution of GST till the registered dealers getting a formal GST ID number, issuing a revised invoice for every billing is a must. The tax invoice must adhere to the terms of GST and is mandatorily be issued within 30 days from the day of issuing the original registration certificate.

It is quite obvious from the above sentence that no revised invoice shall be considered valid after issuing the registration certificate to the registered taxpayers. Gen GST Billing Software caters to all the invoice related requirements of the taxpayer (small or large businesses).

Understanding Supplementary GST Invoices

Original receipt/invoice may lack certain parameters but the supplementary GST invoice is efficient in every field. There are occurrences where the original invoice lacks details of the taxable value of goods and services supplied. Such is the case when Supplementary Invoices are referred for correct knowledge. Supplier must generate the Supplementary invoice to accumulate such additional changes. SI includes debit and credit notes, hence serving both upward and downward revisions.

No format is pre-defined by the GST Law for supplementary invoices still there are certain headings that are required to be mentioned in such invoices. Particulars are as follows:

Valid details of the Supplier’s name and address

Supplier’s GSTIN

Nature of invoice, i.e. “Debit Note,” “Credit Note,” “Revised Invoice” or “Supplementary Invoice.” must be mentioned in bold.

The invoice must be written in an alpha-numeric serial number, particularly as per the accounting year

The date of issuing the invoice.

Name and address of the Recipient

Recipient’s GSTIN

In case if the customer is an unregistered taxpayer then proper address and place of delivery shall be mentioned along with the State Code.

The original invoice serial number must be provided for which the supplementary invoice is to be issued.

The differential amount of tax, the taxable value of the goods or services or rate of tax

Signature of an authorized person for the physical document, or digital signature for the electronic invoice.

To be Noted: With the help of Supplementary Invoice, one can claim an extra ITC on the tax he is paying to the government.

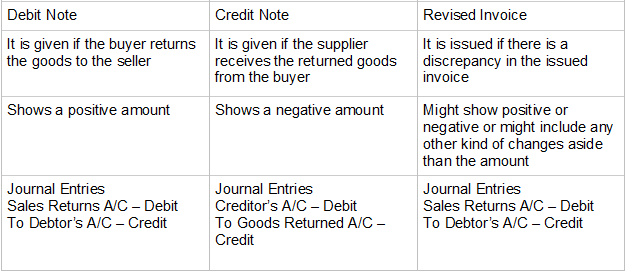

Understanding Credit Note

In accordance with the current GST law, section 2(35) read with section 24(1), credit note can be issued only if there is an original tax invoice issued for goods and services sold and in case if the tax mentioned in the invoice is more than the tax that is supposed to be paid on the respective supply.

Credit Note is applicable in case if:

The registered taxpayer issues an original tax invoice for the supply of Goods and Services.

The invoice displays the amount of tax greater than the actual payable amount

Credit notes fulfill the accounting requirements of a GST invoice correctly adjusting the values and declaring valid tax amounts.

Contrasting Revised and Supplementary Invoice

Revised and Supplementary invoices differ on the following basis.

Differentiating Debit Note, Credit Note, and Revised Invoice

FAQs on GST Tax Invoice Revision

Q.1 Return once filed providing all the invoices can be altered? If yes then how can the return or invoice be revised?

There is no such provision of altering already filed returns under GST Law. Amendments can be made in the invoice by issuing the supplementary invoice or credit or debit notes.

Q.2 What is the prescribed time limit for issuing the supplementary invoice by the taxpayer?

Supplementary Invoice should be raised within 30 days starting from the day of receiving the original invoice.

Q.3 Is there any time limit for updating the supplementary invoice in the returns for further computing the taxable value of goods and services?

Supplementary invoices are required to be updated on the GSTN portal on monthly basis. In case of an interstate supply or where the taxable value of the goods and services is less than a hundred and fifty thousand rupees, a consolidated invoice is issued

Q.4 When and where do we need to raise a supplementary invoice?

Circumstances where raising a Supplementary Invoice is mandatory:

The customer/recipient rejects the goods prevailing low quality.

Change in the rates of tax.

If there are amendments in the taxable value of the goods or services.

If there is a short receipt of materials from the recipient

If the supplier charges a refund to the supplier

Q.5 I am a recipient of the goods, and I reject the same upon receipt. Will I able to raise a debit note? Is a taxpayer eligible for issuing a debit note in case if he rejects the goods upon receiving them?

It is possible as it is normal accounts but will have no effect under GST. Each credit or debit note issued by a taxpayer have a significant commercial impact. Still, a proper setup is awaited under GST for debit note issued by the recipient.

An array of services such as laser photography, Jewellery photography, clothes photography, wedding video recording, pre-wedding video shooting, aerial photography, fluorescent photography. etc come under the category of Videography and Photography service and fall under Goods and Services Tax (GST) purview. This is a complete guide to know about the GST Rate on Photography and Videography Services. Let’s dive right in.

Eligibility of Photography & Videography Services for GST Registration

SAC Code For Photography & Videography Services

GST Return for Photography & Videography Services

Time of supply for Videography & Photography Services

GST ITC For Photography & Videography Services

Related

GST Rate on Photography & Videography Services

GST @ 18% is applicable on the Photography & Videography Services. Services are as follows:

Portrait photography services

Advertising & related photography services

Event photography & event videography services

Speciality photography services

Restoration & retouching services of photography

Photographic & video graphics processing services

Other Photography & Videography and their processing services n.e.c.

If the rate for a service is not explicitly specified by the GST Council then the default rate of 18% GST applies to these services.

Recommended Post: GST Impact on Wedding Services in India

Eligibility of Photography & Videography Services for GST Registration

Section 22 to 25 of the GST Act specifies the threshold limit of goods & services to be surpassed and other requirements that make an individual eligible for the registration under GST.

As per these sections, a supplier of Photography & Videography services is eligible to be registered under the GST if he duly meets the following conditions:

Turnover > 20 Lakhs

When the aggregate turnover of taxable supply of goods or services in a fiscal year is more than Rs. 20 Lakhs.

Turnover > 10 Lakhs

When the aggregate turnover of taxable supply of goods or services in a fiscal year is more than Rs. 10 Lakhs, provided the supplier resides at North Eastern area – Arunachal Pradesh, Assam, Himachal Pradesh, Manipur, Meghalaya, Nagaland, Sikkim, Jammu & Kashmir, Tripura & Mizoram and Uttarakhand.

Note: Voluntary GST registration can be obtained by a service provider (if needed)

SAC Code For Photography & Videography Services

SAC Code under GST for Photography & Videography and their processing Services is a 6 digital numerical code. First two digits i.e. 99 of the code are alike for all the Photography & Videography services, whereas the next two and last two digits of the SAC code signify as major service and nature of the service, respectively.

SAC Code For Photography & Videography Services is as follows:

SAC Code 998381 – Portrait photography services

SAC Code 998382 – Advertising and associated photography services

SAC Code 998383 – Event photography and videography services

SAC Code 998384 – Specialty photography services

SAC Code 998385 – Restoration and retouching photography services

SAC Code 998386 – Photographic & video graphics processing services

SAC Code 998387 – Other Photography & Videography and their processing services

GST Return for Photography & Videography Services

Following GST Return has to be filed by Photography & Videography Services Providers:

Monthly Return GSTR 3 B to be filed by the 20th of the subsequent month.

Monthly/ Quarterly (based on turnover)GSTR-1 to be filed all GST registered supplier.

Annual GST returnsto be filed by all GST registered supplier on or before the due date of 31st December.

Time of supply for Videography & Photography Services

GST on Photography & Videography Services becomes payable at the time of supply of such services. Time of supply for Videography & Photography Services is:

As soon as the invoice is issued

Or

When an invoice is not issued within 30 days from the date of supply of service

Or

Date when the services are received in recipient’s books of account

whichever is earlier.

GST ITC For Photography & Videography Services

An income tax credit of GST on Photography & Videography Services can be claimed by a registered taxpayer on inward supplies if he holds valid invoice and the supplier has duly deposited the taxes to the government.

Also Read: GST Rate on Event Management Services

Eligibility to claim ITC

A recipient of goods and services become eligible to claim ITC only if he duly meets all the following conditions:

He has valid tax invoice or Debit Note or Bill of Entry.

He has received Goods or Services.

His supplier has paid the taxes to the government.

GSTR is filed.

Note: ITC claimed by a recipient gets reversed if he fails to pay the amount for the goods or services supplied to him along with tax payable on that amount within a time-frame of 180 days.

Urging on the need to call for a GST council meeting, Bengal Finance Amit Mitra said that there should be a meeting to discuss the unsteady GST collections, various GST rates and the ways to cut down tax evasion.

Amit Mitra in a written statement to Union Finance Minister Nirmala Sitharaman stressed the point that the business intelligence unit has to be planted in every state to bring in limelight various frauds taking place under the GST regime.

Depicting the current scenario, Mitra said that there still remain some unmatched invoices allowing corrupt dealers to still claim Input Tax Credit (ITC) by generating fake GST invoices. This calls for a need to conduct a council meeting that is centric to only tax frauds and other systematic issues. “However, the date of the next GST council meeting is yet to be finalized by the concerned authorities”, Mitra says.

Collections under GST have sloped down as compared to last year’s collection in months of September and October, this has led to the need for involvement of a business intelligence team.

Statistics say that GST collection for October 2019 is Rs 95,380 crore which is 5.2% lower than the collections of Rs 1,00,710 crore in October 2018. GST revenue collections tumbled to a 19-month low of Rs 91,916 crore in September this year.

Bengal FM further stated that he tried to drag the tax leak issue in the last GST Council Meeting held on 20 September 2019, but it was never discussed during the meeting.

The Insurance Corporation Employees Union has put forth a demand to remove GST on premiums. In 2014, GST at the rate of 18% was imposed on premiums for insurance policies by the Central Government. At the same time, interest for loans on policies and policies renewal were also not escaped by GST implementation.

According to the N.P. Ramesh Kannan, general secretary of the union, Implementation of GST on insurance policies is a demotivation for people to invest in policies. Today, Life insurance corporation of India is the largest insurance company with an asset value of above $370 billion which provides huge capital to the Government of India (GOI) because it allows long-term savings. So, a government should remove GST from premiums for insurance policies because that would be a booster for investors to invest in insurance policies which will further upsurge the capital for GOI.

“There is also GST on the service charge for changing nominations. This is affecting policyholders across the nation. Life insurance corporation of India is one of the biggest capital providers for the government as it attracts long-term investments. The government should, in turn, encourage people to invest in insurance. Instead, the imposing of GST is discouraging,” said N.P. Ramesh Kannan, general secretary of the union.

Many requests have been made to the GOI, to remove the Goods and Services Tax from an insurance policy, by the union and the letters collected from well-known personalities of India in this regard, have also been sent to GST council membersGet to know the details about GST council and how it works for GST implementation in India? We also describe its constitution, functions, quorum and decision-making. Read More .

“We have urged the government through various campaigns and have also reached out to 22 lakh policyholders regarding this. Recently, we collected letters from 3,295 famous personalities from the Madurai division of LIC, comprising six districts, including MLAs and MPs across political parties. We will submit those letters to the State GST Council Member,” said union president G. Meenakshi Sundar.

An income tax rebate of ₹1,00,000 has been demanded by the union to provide refunds to the insurance policyholder as a measure to stimulate the investment in insurance.

Small town based tax officials have sent written GST notices to many companies catering the financials services seeking details about the tax paid, revenue generated and organisational framework. This has germinated fear within these companies that if their compliance burden would rise.

Indirect tax officials have started scrutinising the companies based across India. A Mumbai based financial services company has received a written notice that reads, “Provide brief note of organisational structure, details of turnover whether taxable, exempt, nil rated or non-GST turnover.. details of place of supply,”

Almost in every case, companies are already adhering to GST compliance and giving details to the same state’s capital based tax officials.

Under the GST regime, every company must have a Goods & Services Tax (GST) registration in every state. However, queries (if any) in this regard are raised by tax officials of the city.

In the context, mofussil tax officers turn their back on under a specific section of the GST Act which interprets that any company from any part of the nation can be interrogated by any indirect tax officer regarding any transaction.

Taking an example of Andhra Pradesh. Andhra Pradesh based companies are registered in Hyderabad but they are receiving written queries from state’s small-town based indirect tax officials.

However, top-level employees and partners of such financial services company do not go to bat for this interpretation by GST officials as they are of the view that GST has already increased compliance burden on service providing companies and if the indirect tax officials from any part of the world would begin questioning them, it would lead to pressure upsurge on the companies.

In this regard, MS Mani, partner, Deloitte India, said, “The compliance requirements in GST for service providers are significantly higher than the erstwhile service tax regime and the need to respond to inquiries from various parts of the country leads to additional pressures on businesses. A single authority should be empowered to enquire/investigate all GST issues of a service provider instead of multiple authorities, which will lead to efficiencies on both sides,”

Abhishek A Rastogi, partner, Khaitan & Co. suggested, “The jurisdiction has been a subject matter of debate and in an ideal situation the jurisdictional officer should seek information related to compliance, procedure and other legalities”.

The states of India which are under the surveillance of non-BJP rulers like Punjab, Kerala, Rajasthan, West Bengal and Delhi spoke about their concerns related to GST compensations. They voiced against the Centre claiming that states are in the situation of the financial crisis to which centre needs to look upon.

GST compensation is still awaited by such states for the months of August and September which was supposed to be given by the central government in the month of October, declared by the statement by these five states. The states’ treasure is sloping downwards leading them into the pit of financial crisis due to which the concerned authorities are using central bank’s ways and facilities or overdrafts to meet their financial requirements.

On the other hand, Bengal FM Amit Mitra in his statement stressed upon appealing to the Union FM Nirmala Sitharaman to personally pay attention to the issue keeping in mind the provisions passed by Parliament of India.

This won’t be less than a calamity for the states if the centre does not give them their justified compensation. He said, “It is a dangerous situation”. Further to this, he said, it is for the first time in history that the centre has failed to transfer the committed funds to the concerned states. The due amount for West Bengal is Rs. 1,500 Crores.

Thomas Issac Kerela FM says that their state relied upon the centre for compensation of Rs. 1,600 Crore and that the state is under overdraft for almost a week now. This is for the first time in history that the state is facing such a huge crisis and that immediate action is expected by the centre.

Punjab FM in his statement revealed that the state is lying in wait of Rs. 2,100 crore in compensation from central government and if the dues are not paid on time then the state is in danger of overdraft.

Read Also: Annual Return Clarifications Issued via Circular No. 124/43/2019 Under GST

The same was the tone of Delhi CM Manish Sisodia who declared that the delay in releasing GST compensation by the Central Government has led to Delhi outstanding Rs. 2,355 Crores.

The Joint Statement by all the states said that 60% of tax revenues for states come from GST and most of the states are already in debt up to 50% of the total GST. Such deficits are prominent in hindering the pace of development for any state literally bringing the activities of states to a halt.

The Joint statement even revised the scenario when the states agreed to join GST only if there is a provision of compensation inserted in the Constitution of India. Adding on to this the statement said that the current delay in granting GST compensation has shaken the confidence of the states that had so far supported GST.

Overlooking the disparities of GST, states were always by the side of the GST Council supporting them with all their major and minor decisions, the statement said.

As proposed by many states issue of delayed Goods and Services Tax compensation should be the main agenda of the next GST council meeting and also how the proper revenue collection mechanism can be incorporated providing timely compensations to all the states in the future.

The Central Board of Indirect Taxes and Customs (CBIC) is contemplating on taking stringent actions against the non-filers which may also lead to cancellation of registration by Goods & Services Tax (GST) officials. Besides, the procession made in this context will also be updated daily as decided by the GST department.

Tax officials figure out the amount of tax that should have been collected and the amount of tax actually collected by tax officials, with the help of returns filed by taxpayers. When taxpayers do not file returns, it becomes difficult for tax authorities to estimate the tax collection. As a matter of fact, 20% of assessees do not file GST returns which disturbs the tax collection.

In a meeting held on November 13 by the Central Board of Indirect Taxes & Customs (CBIC) with the Principal Chief Commissioner and Commissioner of GST & Customs, PK Dash, chairman of CBIC, hinted his disagreement on the decision regarding cancellation of non-filers’ registration on not filing the Form GSTR 3B for 6 months and more.

“…the task of cancellation of registration of such non-filers of GST returns should be taken on priority basis and should be furnished by November 25,” is a part of communication from the office of the Principal Chief Commissioner of GST & Central Excise, Mumbai to Principal Commissioner/Commissioner. The same communication was posted in the jurisdiction.

Under the GST regime, its mandatory for a registered person to file returns. A normal supplier has to file monthly returns and supplier under composition scheme has to file quarterly returns.

Similarly, an ISD (Input Service Distributor) has to file monthly returns to report details of credit distributed in the specific month and a TDS deductor & a TCS collector has to file monthly returns to furnish details about TDS & TCS, respectively, in a particular relevant month.

Conditions and events that lead to cancellation of registration are mentioned in Section 29 of the Central Goods & Services Tax (CGST) Act. These conditions include violation of Act’s provisions, non-commencement of business within six months time from the voluntary registration, returns not filed by a taxpayer registered under GST composition scheme for three successive tax periods or by a non-composition assessee for a continuous six months and registration acquirement through the means of fraud, facts suppression or willful misstatement. It has been clearly stated in the provision that cancellation of registration can not take place without providing a chance of being heard to the person.

Notably, the cancellation of registration will not cancel any kind of tax liability or any other dues. Non-filers whose registration gets cancelled will have to pay an amount, by debiting the same in the electronic credit ledger or electronic cash ledger. The amount shall be equal to the credit of input tax w.r.t inputs available in stock and inputs present in semi-finished or finished goods available in stock/ capital goods/ plant and machinery on the date just next to the date on which such cancellation took place or the output tax-liability payable on such products, whichever is higher.

Income tax is a mandatory return to be filed by every taxpayer once in a year and here we will gain some of the basic as well as important insight into the Income tax-related question with the help of relevant frequently asked questions on income tax returns. We will go through the FAQs with easy and meaningful understanding over each question which will further make the viewers get all the details on the tax-related compliance followed by the taxpayer.

Q.1 What is the Meaning of Income Tax Return?

An Income Tax Return (ITR) is a statutory form in a specified format with the particulars of annual income earned and tax liabilities paid on it by a person in a financial year. In short, an ITR is a reporting, of income & tax liabilities, by a person to the income tax department. Different Income tax return Forms have been prescribed for different kinds of income and its status which means depending on the nature & status of the income, a taxpayer chooses as to which ITR form he needs to download and file. The form is available for download on the www.incometaxindia.gov.in

Q.2 What are the Different Ways of Filing an ITR?

The different ways of filing an ITR are as follows:

Furnishing a paper return

Furnishing an electronic return with digital signature

Electronically furnishing/transmitting the data in the return with EVC (Electronic Verification Code)

Electronically furnishing/transmitting the data in the return followed by submission of return verification in Form ITR-V.

It is to be noted that if the taxpayer if filing the returns in the way in point (iv) without digital signature, then he shall have to take two printed copies of Form ITR-V. One copy of ITR-V will need to be duly signed by the taxpayer, and sent to “Income-tax Department – CPC, Post Bag No. 1, Electronic City Post Office, Bangalore-560100 (Karnataka) within the specified time-frame i.e. 120 days) through an ordinary post or speed post. Another copy shall be retained by the taxpayer and kept for the record.

Q.3 What are the Ways to File an Income Tax Returns Online?

Income Tax Return can be e-filed online with the income tax software provided by the Central Board of Direct Taxes. This is a Java-based secure software which is available for free. ITR can also be e-filed using paid software of the third party like SAG Infotech, Karvy; which are experts in taxation & accounting software development. This software is government-certified and is capable of performing all the operations executed by the Government utility such as auto calculating the Income Tax as per the prevailing tax rate, uploading the ITR on the official website of Income Tax department and so on.

Q.4 How an Excess Tax Paid by a Taxpayer is Refunded?

Taxpayer can claim the excess tax as refund by filing an ITR. Income Tax department refunds the excess tax to the taxpayer by crediting the amount in the taxpayer’s bank account via ECS transfer

Q.5 What are the Advantages of Filing an ITR?

Filing of return is a statutory obligation which should be duly executed as it not only keeps in good books of government but also makes you a contributor in the national development. Besides, an income-tax return act as evidence of your creditworthiness before banks and other financial institutions and so facilitates you with easy availing of loans. It also helps you carry forward the losses and claim the tax return when an excess tax has been paid.

Q.6 What are the Steps to Electronically File an Income Tax Return?

An Income Tax Return can be filed electronically on the e-filing portal developed by Income-tax Department for the easy & glitch-free e-filing of ITRs. The taxpayers can e-file an ITR by logging www.incometaxindiaefiling.gov.in. Besides, third-party software like Gen IT software for filing of ITR you can also use.

Steps to e-file an ITR

Log on to the portal (www.incometaxindiaefiling.gov.in).

Download the relevant ITR form.

Enter details from Form 16.

Compute all appropriate tax details such as tax payable, pay tax etc.

Confirm the furnished details and submit the return.

Digital sign the file.

Receive confirmation from ITR verification

E-verify your Return through Demat account number, Bank account number, etc.

Q.7 Do We Need to Attach any Documents with the Income Tax Return?

No, a taxpayer need not attach any documents such as TDS certificates, investment proof, etc with the Income Tax Return whether e-filed or filed manually. However, such documents should be kept safely by the taxpayer, so that it can be presented readily before the tax authorities whenever needed under circumstances of inquiry, assessment, etc.

At the same time, it should be noted that the taxpayers who needs to file an audit report u/s 10(23C)(iv), 10(23C)(v), 10(23C)(vi), 10(23C)via), 10A, 10AA, 12A(1)(b), 44AB, 44DA, 50B, 80-IA, 80-IB, 80-IC, 80-ID, 80JJAA, 80LA, 92E, 115JB or 115VW or to give a notice u/s 11(2)(a) shall e-file such audit reports or notice on or before the deadline of filing the ITR.

Q.8 What is e-filing Utility Provided by the Income-tax Department?

A free e-filing utility has been provided by the Income-tax Department. The software is in Java & excel and facilitates easy & online filling and filing of ITR. The e-filing utility provided by Department is easy, user-friendly and also displays instructions on how to use it. The utility is available for free download on the website – www.incometaxindiaefiling.gov.in

Q.9 Is it Mandatory to File an Income Tax Return?

Yes, filing an ITR is mandatory. Government of India (GOI) has made the e-filing of income tax returns (ITR) mandatory for all the assesses who are earning an annual Income above INR 5 Lakhs.

Read Also: Free Download Demo of Income Tax Return Filing Software

Q.10 What are the Advantages of Income Tax Return Filing?

ITR reflects the taxes paid by an assessee on his annual income in a given FY. In some cases, when the tax paid by the assessee exceeds his actual tax liability then he shall become eligible for tax refunds claims which can be availed only when you are an ITR filer. Many other advantages of filing tax returns are:

Easy loan approval

Bolster your creditworthiness for future loans

Easy availment of Presumptive Taxation Scheme

Refund of excess taxes paid

Carry forward of Losses

Depreciation claim

Defends from prosecution, interest, penalties & embarrassments.

Convenient Foreign VISA Stamping

Q.11 How is e-filing Different from E-payment?

E-payment refers to the process of electronic payment of tax like payment through net banking or using banks’s debit/credit card. Whereas e-filing refers to the process of electronically or online furnishing of Income Tax Return. A taxpayer may integrate the two processes and execute his tax-related liabilities easily and rapidly.

Q.12 What are the Advantages of Filing an ITR Electronically?

Advantages of e-filing are: It is less time consuming, cost-effective and effortless. On can file an ITR online from anywhere at anytime easily and quickly. The returns filed online are processed must faster than those filed manually.

Q.13 Do I Need to File an ITR for a FY in which I have not Generated Any Income?

Yes, you need to file an ITR before the due dates if you have incurred any loss in a financial year and you want to carry forward it to the subsequent year for its adjustment against the income of the subsequent year(s).

Q.14 Can a Return be Revised if I Find any Mistakes Later in the ITR Filed by Me?

A return can be revised and a Revised return can be e- filed u/s 139(5) if an assessee encounters any fault, omission or any incorrect statement in the return already furnished by him.

Note: If the return is filed manually or in paper format initially, then it cannot be revised electronically or in online mode.

Q.15 What is the Time Limit within Which an ITR Can be Revised?

An ITR can be revised within prescribed time limit i.e. before the end of the Assessment Year

before the completion of the assessment; whichever is earlier.

Q.16 How can We Check the Status of Our Income Tax Return?

The status of the income tax return can be checked easily in two easy ways. First is by using acknowledgement number without login credentials and second is with login credentials.Steps to be Followed in the Former Method

Step1. Click on “Check the ITR Status” which is present on the extreme left of the homepage of the e-filing website under the services tab.

Step2. Make sure you are redirected to a new page

Step3. Fill your PAN number, ITR acknowledgement number and the captcha code.

Step4. Click “Submit”.

Steps to be followed in the former method

Step1. Login to the e-filing website.

Step 2. Click the option “View Returns / Forms” present on the dashboard.e

Step 3. Select income tax returns and assessment year from the dropdown menu and submit.

Now, the status of your ITR will be displayed on the screen whether it is just verified or it has been processed.

Uttar Pradesh CM Yogi Adityanath is persistent in increasing the tax revenue of the state. UP with the current count of 1.4 million registered taxpayers, CM of the state is intending to increase the numbers and reach up to 2.5 million marks by the next financial year.

Highlights of the meeting of tax officials with CM said that he has announced the target of Rs. 1 Trillion GST collection in FY 2020-21 which is currently Rs. 77,640 crore in FY 2019-20. In the meeting, it was decided to take serious action on curbing tax evasion which would contribute to increasing the tax revenue of the state. The tax department personnel have rolled up their sleeves to get through the orders of CM.

According to ‘Koshvani’, the UP government’s interface for tax and non-tax revenue statistics, the commercial tax/GST/Value Added Tax (VAT) collection during the first 7 months (Apr-Oct) of 2019-20 stood at Rs 22,622 crore compared to Rs 25,690 crore in 2018-19, thus showing a dip of Rs 3,068 crore or nearly 12 percent year-on-year.

CM Yogi has released orders for state tax officials to cope up with tax collection so that future targets could be accomplished. He stressed implementing various laws and procedures for channelizing tax collection in the state. The state’s tax department is launching an extensive campaign for traders registered under GST.

CM has suggested tax employees keep in mind the convenience of the taxpayers and to maintain harmony with the new UP Traders Welfare Board and ordered not to bother bonafide traders.

Before this, the state’s finance minister Suresh Kumar spoke on lower tax collection and poor dealing of tax officials with traders in the state.

For instance, the legal authorities have decided to impose cess on sand import from Madhya Pradesh, while the proposal to start the auction of stone quarries was being considered.

UP has its targets fixed for FY 2019-20 tax collection including Rs. 1.4 trillion, which is 4.4% more than the estimates of Rs. 1.34 trillion in FY 2018-19.

In 2019-20, the UP government has predicted the total collection of Rs 3.91 trillion, including tax and non-tax collection, both arising from state and its share from tax and non-tax revenue of the Centre, apart from the central grants of Rs 68,000 crore.

Out of the total revenue of Rs. 2.93 trillion, Rs. 1.4 trillion would be accumulated from the state’s own assets while Rs. 1.53 trillion would be bagged from the state’s share in central taxes.

According to UP Budget 2019-20, tabled in the legislature on February 7, 2019, the state has accumulated the tax of Rs 77,640 crore from State GST (SGST) and VAT, while excise tax is recorded Rs 31,517 crores.