Uttar Pradesh CM Yogi Adityanath is persistent in increasing the tax revenue of the state. UP with the current count of 1.4 million registered taxpayers, CM of the state is intending to increase the numbers and reach up to 2.5 million marks by the next financial year.

Highlights of the meeting of tax officials with CM said that he has announced the target of Rs. 1 Trillion GST collection in FY 2020-21 which is currently Rs. 77,640 crore in FY 2019-20. In the meeting, it was decided to take serious action on curbing tax evasion which would contribute to increasing the tax revenue of the state. The tax department personnel have rolled up their sleeves to get through the orders of CM.

According to ‘Koshvani’, the UP government’s interface for tax and non-tax revenue statistics, the commercial tax/GST/Value Added Tax (VAT) collection during the first 7 months (Apr-Oct) of 2019-20 stood at Rs 22,622 crore compared to Rs 25,690 crore in 2018-19, thus showing a dip of Rs 3,068 crore or nearly 12 percent year-on-year.

CM Yogi has released orders for state tax officials to cope up with tax collection so that future targets could be accomplished. He stressed implementing various laws and procedures for channelizing tax collection in the state. The state’s tax department is launching an extensive campaign for traders registered under GST.

CM has suggested tax employees keep in mind the convenience of the taxpayers and to maintain harmony with the new UP Traders Welfare Board and ordered not to bother bonafide traders.

Before this, the state’s finance minister Suresh Kumar spoke on lower tax collection and poor dealing of tax officials with traders in the state.

For instance, the legal authorities have decided to impose cess on sand import from Madhya Pradesh, while the proposal to start the auction of stone quarries was being considered.

UP has its targets fixed for FY 2019-20 tax collection including Rs. 1.4 trillion, which is 4.4% more than the estimates of Rs. 1.34 trillion in FY 2018-19.

In 2019-20, the UP government has predicted the total collection of Rs 3.91 trillion, including tax and non-tax collection, both arising from state and its share from tax and non-tax revenue of the Centre, apart from the central grants of Rs 68,000 crore.

Out of the total revenue of Rs. 2.93 trillion, Rs. 1.4 trillion would be accumulated from the state’s own assets while Rs. 1.53 trillion would be bagged from the state’s share in central taxes.

According to UP Budget 2019-20, tabled in the legislature on February 7, 2019, the state has accumulated the tax of Rs 77,640 crore from State GST (SGST) and VAT, while excise tax is recorded Rs 31,517 crores.

The GSTR 9 is a GST annual return form to be filed by the regular taxpayer once a year with all the consolidated details of SGST, CGST and IGST paid during the year. Here, SAG Infotech Pvt. Ltd. briefs all the details and rules and regulations for GSTR 9 online filing along with step-by-step compliance procedure.

Get to know all the related information of GST return 9 annual filing procedure, format, eligibility & rules along with proper screenshots and filing guidance at each and every step. For any query and question, ask our experts and professional chartered accountants which will resolve all your doubts as soon as possible. The eligible taxpayers can download and view the GSTR 9 form in PDF format.

Note: Filing of form GSTR-9 for those taxpayers who (are required to file the said return but) have aggregate turnover up to Rs. 2 crores made optional for the said tax periods for FY 2017-18 and FY 2018-19 by GST Council 37th meeting. Read Official Press Release

Latest News/Updates of GSTR 9

Who is Required to File?

Different Sorts of Annual GST Returns

Due Dates Extension & Penalty Norms

How to File?

GSTR 9 Filing By Gen GST Software

GSTR 9 General Queries

GSTR 9 Offline Tool

Here, we are going to discuss the complete GST Annual Return form under the goods and services tax.

Latest News/Updates of GSTR 9 Form

The central board of the indirect taxes department has once again revised the due date of GSTR 9 & 9C.

GST Annual Return (GSTR 9, 9A & 9C) May Be Discarded For Small Taxpayers (the notification may be disclosed by GST Council in the next 37th meeting). More

Easy Guide to GSTR 9C Part II Reconciliation of Gross Turnover. More

Meaning of Filing GSTR 9 (GST Annual Return Form)

It is meant for a return form which is required to be filed once in a year by the regular taxpayers concerning GST regime. It is further categorized in IGST, SGST, and CGST. Under the heads, the taxpayers fill information about supplies made and received in a year separately. It is a consolidated form which comprises the details mentioned in the monthly/quarterly returns in a year.

Who is Required to File GSTR 9 (GST Annual Return Form)?

All the registered regular taxpayers are required to file a form under the GST regime except below list:

Taxpayers opting composition scheme

Casual Taxable Person

Non-resident taxable persons

Persons paying TDS

Input service distributors

What are Different Sorts of Annual GST Returns?

Different kinds of annual return under GST:

GSTR-9 Annual Return Form: The regular taxpayer who files 1 and 3B forms are required to file the GSTR-9.

GSTR-9A: The composition scheme holder under GST is required to furnish GSTR-9A.

GSTR-9B: All the e-commerce operators who have filed GSTR-8 are required to file GSTR-9B in a financial year.

GSTR-9C: The taxpayers whose annual turnover cross Rs. 2 crores are required to file GSTR-9C in a financial year. All those taxpayers are needed to obtain the accounts to be audited and furnish a copy of reconciliation statement of tax already paid, audited annual accounts and tax payable according to the audited accounts with GSTR-9C.

Due Date Extension for Filing GST Annual GSTR 9 Return Form

Once again, the CBIC department has extended the due date of GSTR 9 annual return form for both financial year (Read Press Release)

Financial Year 2017-18 – 31st December 2019

Financial Year 2018-19 – 31st March 2020

Note: “Central Board of Indirect Taxes & Customs (CBIC) notified the amendments regarding the simplification of GSTR-9 (Annual Return) and GSTR-9C (Reconciliation Statement) which inter-alia allow the taxpayers to not to provide split of input tax credit availed on inputs, input services and capital goods and to not to provide HSN level information of outputs or inputs, etc. for the financial year 2017-18 and 2018-19.”

Penalty Norms When you Miss the Due Date of GSTR-9 Filing

As per the penalty provisions of GSTR-9 annual return form, the taxpayer has to pay Rs. 200 per day as a penalty in which Rs. 100 consist of SGST and Rs. 100 for CGST. Also, it is to be noted that the total penalty cannot exceed 0.25% of the total turnover on which the said penalty is being levied.

GST Annual Return Form Major Revisions By Council’s 31st Meeting

Change of headings in the forms to specify that the return in FORM GSTR 9 FORM GSTR-9A would be related to supplies etc. ‘made during the year’ and not ‘as declared in returns filed during the year’

FORM GSTR-1 & FORM GSTR-3B returns are required to be filed before the filing of return FORM GSTR-9 & FORM GSTR-9C

FORM GSTR 9 & FORM GSTR-9C cannot be used to avail ITC

The information would be auto-populated in Table 8A of FORM GSTR-9 for all invoices pertaining to previous FY (irrespective of the month in which such invoice is reported in FORM GSTR-1)

Value of “non-GST supply” including the value of “no supply” may be reported in Table 5D, 5E, and 5F of FORM GSTR-9

How to GSTR 9 Return Offline Tool (v1.1)

The main purpose behind inventing and designing an excel based GSTR-9 offline tool is to facilitate the taxpayer in the offline preparation of the GSTR-9 return. To download the utility, there are some systems requirements. So, before downloading the same, we must ensure that our system is compatible.

System Requirement

Compatibility ensures the smooth functioning of the tool. Make sure that you have Operating system – Windows 7 or above and Microsoft Excel 2007 & above, installed in your system.

GSTR 9 Annual Return Form- Complications & Sorting Out Tips

There are many difficulties with Form GSTR 9 and bewilderment with its format which was released in September last year (2018). The most difficult problem with this Form is that the information would not get auto-populated in this Form, despite the fact that the same information has been filed previously in the monthly and quarterly akin periodic returns. To ease and simplify the process of filing an annual return, the GSTN revamped the form and thus sorted out most of the inconveniences. But still, there are some issues which remained unresolved. We are presenting those issues with some suggestions to sort them out.

GSTR 9 requires HSN which was not required while filing GSTR 3B: In the Annual Return Form GSTR- 9, HSN of inward supplies is needed although it was not needed while filing monthly GSTR 3B. The HSN summary is mandatory to be reported only for those HSN which accounts for the minimum 10% of the total inward supplies.

Suggestion: The reporting of HSN of inward supplies becomes irksome if not maintained previously. But we have a solution for this, GenGST fills the table 18 in the GSTR 9 automatically. Table 18 consists of HSN codes of the inward supplies which get automatically filled from the purchase register by GenGST software.

Details of ITC needs to be mentioned as Inputs/Input services/ Capital Goods: An isolated detail of availed ITC needs to be mentioned as Inputs/Input services/ Capital Goods in the Form GSTR 9.

Suggestion: The division of ITC availed as Inputs/Input services/ Capital Goods in the Form GSTR 9. Will take the assessee back to rework on the accounting entries because of the absence of these details in the periodic returns. Here, Gen GST facilitates the assessee to report this bifurcation with ease in the GSTR 9 while filing it.

Reporting of altered transactions: In the Annual Return Form GSTR- 9, we need to report the altered transactions of the FY 2017-18 filed in the current FY returns’ of April to September or till the annual return filing of FY 2017-18 i.e. 31 Dec 2018, whichever is earlier.

Suggestion: Gen GST has a feature of reconciliation and reporting through which it reconciles the altered transactions of FY 2017-18 filed in the current financial year and report the same in the annual return accordingly.

How to File the GST Form GSTR 9 Annual Return with Latest Format

The GSTR 9 is divided into six parts and 19 tables and the most important thing as suggested by CBIC that there is no revise facility on the GST Portal.

Here you go:

Part I: Basic Details has the following three sections and four tables:

1. Financial Year for which return is being filed. Note: For FY 2017-18, it will contain details for July 2017 to March 2018 period.

2. GSTIN of the taxpayer

3A Legal Name of the registered person

3B Trade Name (if any) of the registered business

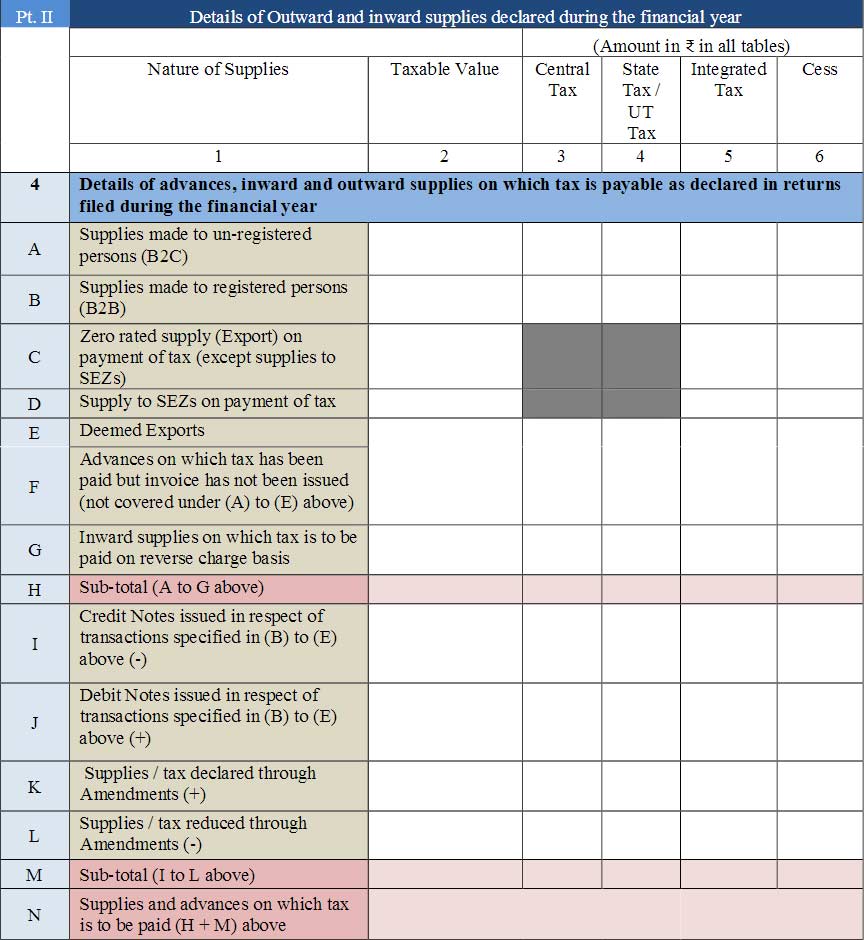

Part II: It consists of details of Inward and Outward supplies made during the particular financial year for which the return is being filed. In short, this part contains a consolidated data of all the supplies reported by the taxpayer in all his/her returns filed during that year. It has been divided into the following sections and tables.

4. This section will contain the details of advances, inward and outward supplies on which tax is payable as declared in returns filed during the financial year.

4A Supplies made to un-registered persons (B2C): The table will contain the aggregate value of supplies made to unregistered persons such as consumers, including the supplies made via e-commerce means, on which the supplier paid tax.

4B Supplies made to registered persons (B2B): The table will contain the aggregategstr_9_gen_gst value of supplies made to registered persons, including the supplies made to UINs, on which the supplier paid tax. It will also contain details of the supplies made through e-commerce websites on which tax was paid by the supplier.

4C Zero rated supply (Export) on payment of tax (except supplies to SEZs): This field will contain details of zero-rated supplies such as exports on which tax has already been paid.

4D Supply to SEZs on payment of tax: The supplier will declare an aggregate value of supplies made to SEZ units on which tax has been paid.

4E Deemed Exports: Provide the aggregate value of supplies of deemed exports nature on which the supplier has paid the tax.

4F Advances on which tax has been paid but invoice has not been issued (not covered under (A) to (E) above): Mention details of unadjusted advances on which tax has been paid but invoices are not issued in this financial year.

4G Inward supplies on which tax is to be paid on reverse charge basis: It will contain an aggregate value of all input supplies (purchases), including supplies made by registered and unregistered persons and import of services, on which tax is to be paid by the recipient on the reverse charge basis.

4H Sub-total (A to G above)

4I Credit Notes issued in respect of transactions specified in (B) to (E) above (-): the Consolidated value of credit notes issued in respect of transactions mentioned in the above fields (4B to 4E) goes here.

4J Debit Notes issued in respect of transactions specified in (B) to (E) above (+): the Consolidated value of debit notes issued in respect of transactions mentioned in the above fields (4B to 4E) goes here.

4K Supplies/tax declared through Amendments (+): Details of tax added through amendments in the above-mentioned details.

4L Supplies/tax reduced through Amendments (-): Details of tax reduced through amendments in the above-mentioned details.

4M Sub-total (I to L above)

4N Supplies and advances on which tax is to be paid: 4H + 4M (above)

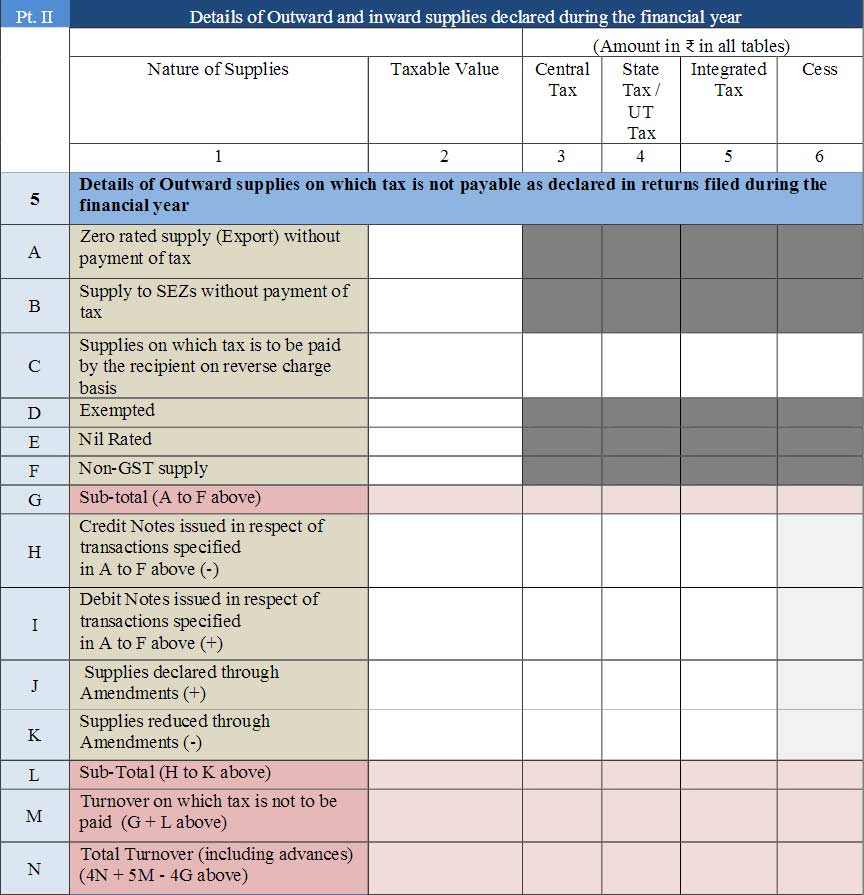

5. Details of Outward supplies on which tax is not payable as declared in returns filed during the financial year

5A Zero rated supply (Export) without payment of tax: This field will contain details of zero-rated supplies such as exports on which tax has not been paid.

5B Supply to SEZs without payment of tax: Contains details of supplies made to SEZ units on which tax has not been paid.

5C Supplies on which tax is to be paid by the recipient on reverse charge basis: Mention here the total value of supplies made to registered persons on which GST was paid by the recipient on RCM basis.

5D (Exempted)/ 5E (Nil Rated)/ 5F (Non-GST supply): an Aggregate value of exempted, Nil Rated and Non-GST supplies shall be declared here. Table 8 of FORM GSTR-1 may be used for filling up these details. The value of “no supply” shall also be declared here.

5G Sub-total (A to F above)

5H Credit Notes issued in respect of transactions specified in A to F above (-): an Aggregate value of credit notes issued in respect of supplies declared in 5A,5B,5C, 5D, 5E and 5F shall be declared here. Table 9B of FORM GSTR-1 may be used for filli compliance procedure.Get to know all theng up these details

5I Debit Notes issued in respect of transactions specified in A to F above (+): an Aggregate value of debit notes issued in respect of supplies declared in 5A,5B,5C, 5D, 5E and 5F shall be declared here. Table 9B of FORM GSTR-1 may be used for filling up these details.

5J and 5K Supplies declared through Amendments (+), Supplies reduced through Amendments (-): Details of amendments made to exports (except supplies to SEZs) and supplies to SEZs on which tax has not been paid shall be declared here. Table 9A and 14 Table 9C of FORM GSTR-1 may be used for filling up these details.

5L Sub-Total (H to K above)

5M Turnover on which tax is not to be paid (G + L above)

5N Total Turnover (including advances) (4N + 5M – 4G above): Total turnover including the sum of all the supplies (with additional supplies and amendments) on which tax is payable and tax is not payable shall be declared here. This shall also include a number of advances on which tax is paid but invoices have not been issued in the current year. However, this shall not include the aggregate value of inward supplies on which tax is paid by the recipient (i.e. by the person filing the annual return) on the reverse charge basis.

Part III: It consists of details of ITC as declared in returns filed during the financial year

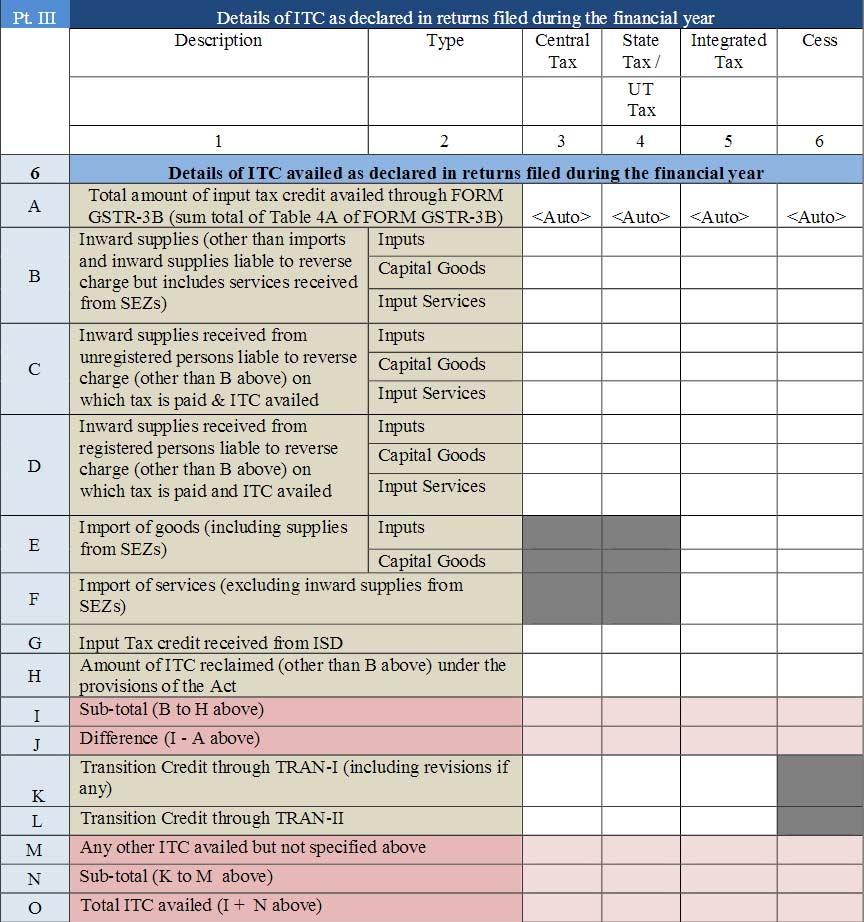

6. This section will contain the details of ITC availed as declared in returns filed during the financial year:

6A Total amount of input tax credit availed through FORM GSTR-3B (the sum total of Table 4A of FORM GSTR-3B): Total input tax credit availed in Table 4A of FORM GSTR-3B for the taxpayer would be auto-populated here.

6B Inward supplies (other than imports and inward supplies liable to reverse charge but includes services received from SEZs): an Aggregate value of input tax credit availed on all inward supplies except those on which tax is payable on reverse charge basis but includes the supply of services received from SEZs shall be declared here. It may be noted that the total ITC availed is to be classified as ITC on inputs, capital goods and input services. Table 4(A)(5) of FORM GSTR-3B may be used for filling up these details. This shall not include ITC which was availed, reversed and then reclaimed in the ITC ledger. This is to be declared separately under 6(H) below.

6C Inward supplies received from unregistered persons liable to reverse charge (other than B above) on which tax is paid & ITC availed: Aggregate value of input tax credit availed on all inward supplies received from unregistered persons (other than import of services) on which tax is payable on reverse charge basis shall be declared here. It may be noted that the total ITC availed is to be classified as ITC on inputs, capital goods and input services. Table 4(A)(3) of FORM GSTR-3B may be used for filling up these details

6D Inward supplies received from registered persons liable to reverse charge (other than B above) on which tax is paid and ITC availed: an Aggregate value of input tax credit availed on all inward supplies received from registered persons on which tax is payable on reverse charge basis shall be declared here. It may be noted that the total ITC availed is to be classified as ITC on inputs, capital goods and input services. Table 4(A)(3) of FORM GSTR-3B may be used for filling up these details.

6E Import of goods (including supplies from SEZs): Details of input tax credit availed on the import of goods including the supply of goods received from SEZs shall be declared here. It may be noted at the total ITC availed is to be classified as ITC on inputs and capital goods. Table 4(A)(1) of FORM GSTR-3B may be used for filling up these details.

6F Import of services (excluding inward supplies from SEZs): Details of input tax credit availed on the import of services (excluding inward supplies from SEZs) shall be declared here. Table 4(A)(2) of FORM GSTR- 15 3B may be used for filling up these details.

6G Input Tax credit received from ISD: an Aggregate value of input tax credit received from input service distributor shall be declared here. Table 4(A)(4) of FORM GSTR-3B may be used for filling up these details.

6H Amount of ITC reclaimed (other than B above) under the provisions of the Act: an Aggregate value of input tax credit availed, reversed and reclaimed under the provisions of the Act shall be declared here.

6I Sub-total (B to H above): 6J Difference (I – A above): The difference between the total amount of input tax credit availed through FORM GSTR-3B and input tax credit declared in row B to H shall be declared here. Ideally, this amount should be zero.

6K Transition Credit through TRAN-I (including revisions if any): Details of transition credit received in the electronic credit ledger on the filing of FORM GST TRAN-I including revision of TRAN-I (whether upwards or downwards), if any shall be declared here.

6L Transition Credit through TRAN-II: Details of transition credit received in the electronic credit ledger after the filing of FORM GST TRAN-II shall be declared here

6M Any other ITC availed but not specified above: Details of ITC availed but not covered in any of heads specified under 6B to 6L above shall be declared here. Details of ITC availed through FORM ITC01 and FORM ITC-02 in the financial year shall be declared here.

6N Sub-total (K to M above)

6O Total ITC availed (I + N above)

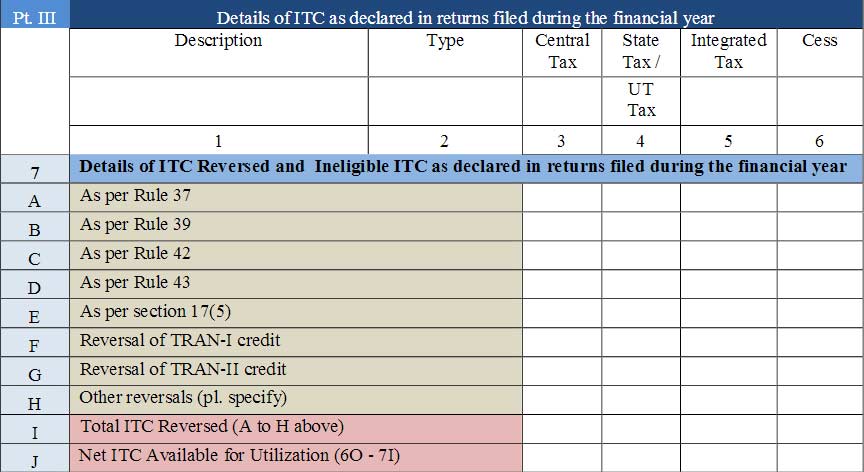

7. It consists of details of ITC Reversed and Ineligible ITC as declared in returns filed during the financial year.

7A As per Rule 37

7B As per Rule 39

7C As per Rule 42

7D As per Rule 43

7E As per section 17(5)

7F Reversal of TRAN-I credit

7G Reversal of TRAN-II credit

7H Other reversals (pl. specify)

7I Total ITC Reversed (A to H above)

7J Net ITC Available for Utilization (6O – 7I)

Details of input tax credit reversed due to ineligibility or reversals required under rule 37, 39,42 and 43 of the CGST Rules, 2017 shall be declared here. This column should also contain details of any input tax credit reversed under section 17(5) of the CGST Act, 2017 and details of ineligible transition credit claimed under FORM GST TRAN-I or FORM GST TRAN-II and then subsequently reversed. Table 4(B) of FORM GSTR-3B may be used for filling up these details. Any ITC reversed through FORM ITC -03 shall be declared in 7H.

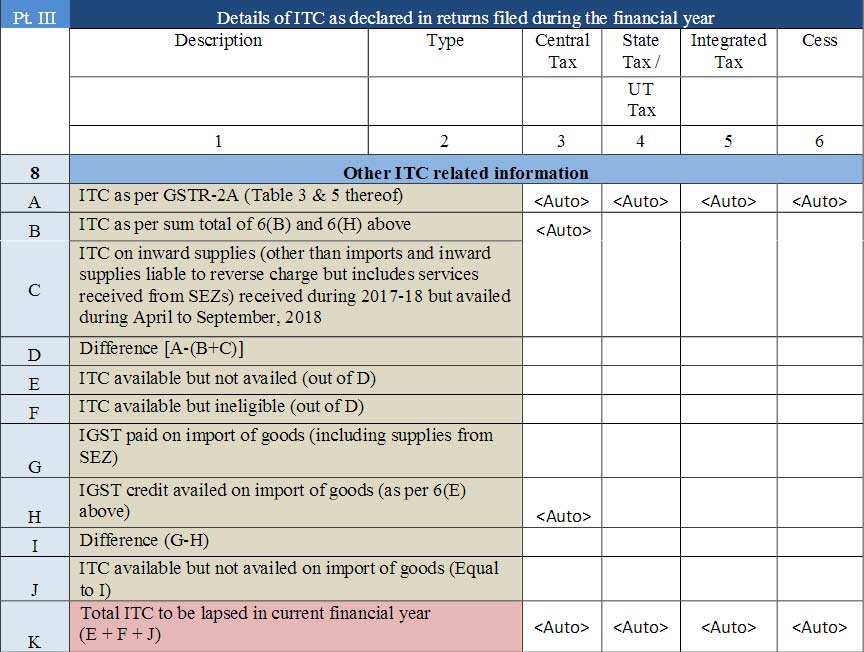

8. Other ITC related information will be provided in this section.

8A ITC as per GSTR-2A (Table 3 & 5 thereof: The total credit available for inwards supplies (other than imports and inwards supplies liable to reverse charge but includes services received from SEZs) received during 2017-18 and reflected in FORM GSTR-2A (table 3 & 5 only) shall be auto-populated in this table. This would be the aggregate of all the input tax credit that has been declared by the corresponding suppliers in their FORM GSTR-I.

8B ITC as per sum total of 6(B) and 6(H) above: The input tax credit as declared in Table 6B and 6H shall be auto-populated here. 8C ITC on inward supplies (other than imports and inward supplies liable to reverse charge but includes services received from SEZs) received during 2017-18 but availed during April to September, 2018: Aggregate value of input tax credit availed on all inward supplies (except those on which tax is payable on reverse charge basis but includes supply of services received from SEZs) received during July 2017 to March 2018 but credit on which was availed between April to September 2018 shall be declared here. Table 4(A)(5) of FORM GSTR-3B may be used for filling up these details.

8D Difference [A-(B+C)]

8E ITC available but not availed (out of D) and 8F ITC available but ineligible (out of D): an Aggregate value of the input tax credit which was available in FORM GSTR2A (table 3 & 5 only) but not availed in any of the FORM GSTR-3B returns shall be declared here. The credit shall be classified as credit which was available and not availed or the credit was not availed as the same was ineligible. The sum total of both rows should be equal to the difference in 8D.

8G IGST paid on import of goods (including supplies from SEZ): an Aggregate value of IGST paid at the time of imports (including imports from SEZs) during the financial year shall be declared here.

8H IGST credit availed on the import of goods (as per 6(E) above): The input tax credit as declared in Table 6E shall be auto-populated here

8I Difference (G-H)

8J ITC available but not availed on the import of goods (Equal to I)

8K Total ITC to lapse in the current financial year (E + F + J): The total input tax credit which shall lapse for the current financial year shall be computed in this row.

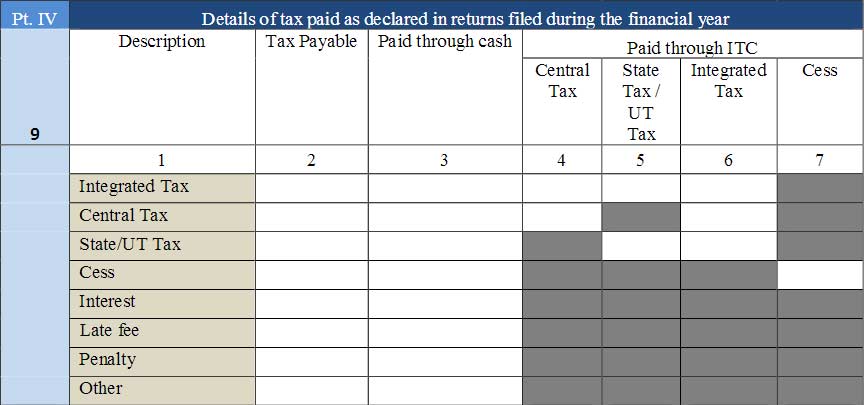

Part IV: Details of tax paid as declared in returns filed during the financial year

9. Details of tax paid as declared in returns filed during the financial year

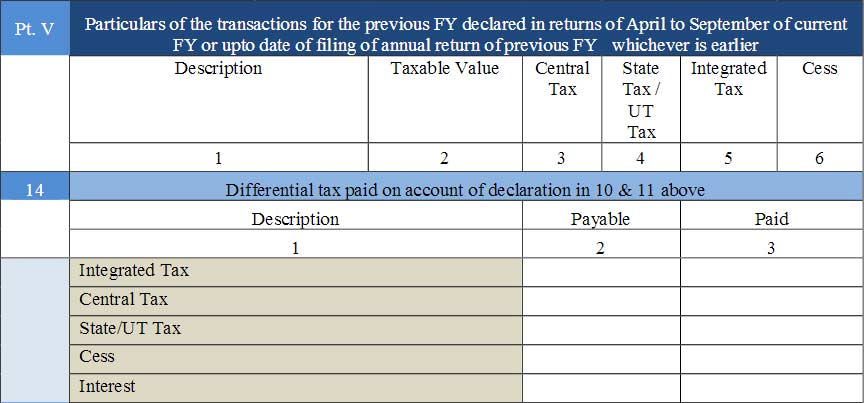

Part V: Particulars of the transactions for the previous FY declared in returns of April to September of current FY or up to the date of filing of annual return of previous FY whichever is earlier

10 Supplies / tax declared through Amendments (+) (net of debit notes) and 11 Supplies / tax reduced through Amendments (-) (net of credit notes): Details of additions or amendments to any of the supplies already declared in the returns of the previous financial year but such amendments were furnished in Table 9A, Table 9B and Table 9C of FORM GSTR-1 of April to September of the current financial year or date of filing of Annual Return for the previous financial year, whichever is earlier shall be declared here.

12 Reversal of ITC availed during the previous financial year: an Aggregate value of reversal of ITC which was availed in the previous financial year but reversed in returns filed for the months of April to September of the current financial year or date of filing of Annual Return for previous financial year, whichever is earlier shall be declared here. Table 4(B) of FORM GSTR-3B may be used for filling up these details.

13 ITC availed for the previous financial year: Details of ITC for goods or services received in the previous financial year but ITC for the same was availed in returns filed for the months of April to September of the current financial year or date of filing of Annual Return for the previous financial year whichever is earlier shall be declared here. Table 4(A) of FORM GSTR-3B may be used for filling up these details.

14 Differential tax paid on account of declaration in 10 & 11 above

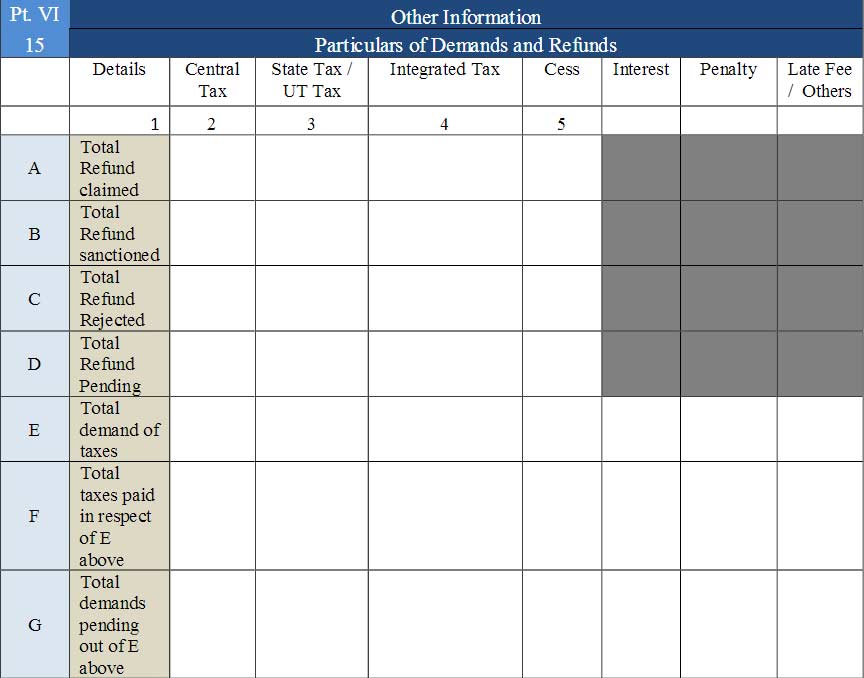

Part VI: Other Information

15A, 15B, 15C, and 15D: Particulars of Demands and Refunds: an Aggregate value of refunds claimed, sanctioned, rejected and pending for processing shall be declared here. Refund claimed will be the aggregate value of all the refund claims filed in the financial year and will include refunds which have been sanctioned, rejected or are pending for processing. Refund sanctioned means the aggregate value of all refund sanction orders. Refund pending will be the aggregate amount in all refund application for which acknowledgement has been received and will exclude provisional refunds received. These will not include details of non-GST refund claims.

15E, 15F, and 15G: Total demand of taxes, Total taxes paid in respect of above, Total demands pending out of E above: an Aggregate value of demands of taxes for which an order confirming the demand has been issued by the adjudicating authority shall be declared here. The aggregate value of taxes paid out of the total value of confirmed demand as declared in 15E above shall be declared here. The aggregate value of demands pending recovery out of 15E above shall be declared here.

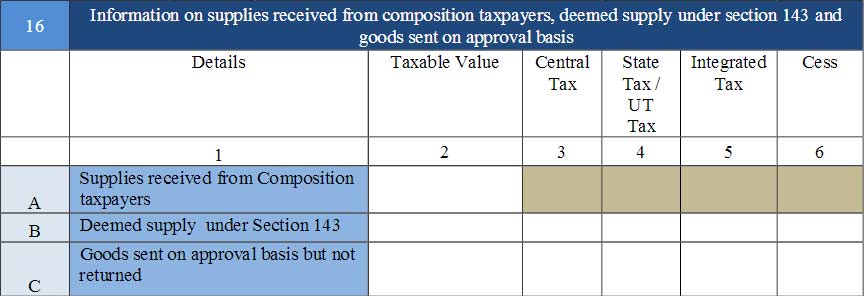

16. Information on supplies received from composition taxpayers, deemed supply under section 143 and goods sent on the approval basis

16A Supplies received from Composition taxpayers: an Aggregate value of supplies received from composition taxpayers shall be declared here. Table 5 of FORM GSTR-3B may be used for filling up these details.

16B Deemed supply under Section 143: an Aggregate value of all deemed supplies from the principal to the job-worker in terms of sub-section (3) and sub-section (4) of Section 143 of the CGST Act shall be declared here.

16C Goods sent on approval basis but not returned: an Aggregate value of all deemed supplies for goods which were sent on approval basis but were not returned to the principal supplier within one eighty days of such supply shall be declared here.

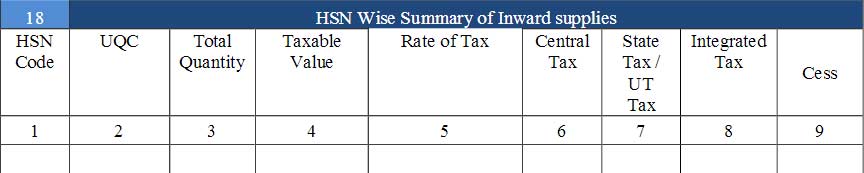

17. HSN Wise Summary of outward supplies and 18. HSN Wise Summary of Inward supplies: Summary of supplies effected and received against a particular HSN code to be reported only in this table. It will be optional for taxpayers having annual turnover up to ₹ 1.50 Cr. It will be mandatory to report HSN code at two digits level for taxpayers having an annual turnover in the preceding year above ₹ 1.50 Cr but up to ₹ 5.00 Cr and at four digits’ level for taxpayers having an annual turnover above ₹ 5.00 Cr. UQC details to be furnished only for the supply of goods. Quantity is to be reported net of returns. Table 12 of FORM GSTR1 may be used for filling up details in Table 17.

19. Late fee payable and paid: Late fee will be payable if annual return is filed after the due date.

General Queries on GSTR 9 Form

Q.1 – What are the rules and regulations for filing GST Annual Return?

The rules and regulations for filing the annual GST return which is referred to as GSTR-9 are controlled by the CGST Act u/s 35(5) and 44(1). According to Section 44(1) of the CGST Act, with Rule 80 (1) of CGST rules indicates to every registered person excluding

Input Service Distributor

TDS Deductor u/s 51 (TDS)

TCS Collector u/s 52 (TCS)

Casual Taxable Person

NRI taxpayer

Q.2 – What is the last date for filing the GST Annual Return?

The person who is registered under the GST must submit the GST annual return digitally in form GSTR-9 on or before 31 December after the end of every fiscal year.

Q.3 – Who can apply for GST Tax Audit?

All the rules about the Tax audit is discussed u/s 35(5) of CGST Act. Every person registered under GST with a turnover during the fiscal year above the threshold limit i.e. Rs 2 crore must-

Get his/her fiscal statements audited by a cost accountant or a chartered accountant

Submit a copy of the annual GST audit report

The reconciliation statement u/s 44(2)

Other documents like this can be determined

Q.4 – In the case of a tax audit, how will the annual GST return be filed?

Through Form GSTR 9C, the annual return must be filed in case of the tax audit which is also known as the annual audit form.

Q.5 – What is the Reconciliation statement in the GST Audit?

With annual audit form GSTR 9C, the taxpayer must also submit a reconciliation statement along with the GST audit certification. The reconciliation statement is the extra details given with GSTR 9C, which confirms the reconciliation of data according to GST annual return as per the accounts book and data.

Q.6 – Who should file GSTR-9?

Every person who has registered under the GST has to file the GSTR-9 according to Section 44(1) of CGST Act 2017. Therefore, despite Annual Turnover, all the registered individuals under the GST must complete the procedure of the annual GST Return Filing.

Q.7 – Who should not file GSTR-9?

As per Section 44(1) of CGST Act-2017 taxpayers that should not file the GSTR-9 are-

Input Service Distributor

TDS deductor u/s 51 (TDS)

TCS collector u/s 52 (TCS)

Casual taxable person

NRI Taxpayer

Q.8 – Can GSTR-9 be filed even in the case of Nil Turnover?

Yes, all registered individuals will have to file GSTR-9 as per their turnover. But, during the Nil turnover, the GSTR-9 can be submitted on one click.

Q.9 – Will transactions for the period before July 2017 be included in GSTR-9?

No, transactions for the period before July 2017 will not be included in GSTR-9 because the GST authority has said that only the details for the period between July 2017 to March 2018 will be considered while filing the GSTR-9.

Q.10 – Define Form GSTR-9A?

Form GSTR-9A is the Annual return that has to be filed at any time during the fiscal year by every registered individual under the composition scheme u/s 10 of CGST Act 2017.

The income tax department has started sending queries to top-notch banks and companies if the common costs such as the CEO’s salary, are dispersed by them to its divisions & branches.

A few top companies with the centre of operations in Pune, Delhi and Mumbai are being interrogated by the IT department on cross-charging of costs.

The IT department wants a proportionate supply of common costs from companies to its various subdivisions ranging from head office to branch office and to consider this distribution of costs as supply under GST.

The supply will attract 18% GST on the total amount i.e. the amount of supply plus 10% of it.

Goods & Services Tax regime is structured in such a way that it spares nothing for free and that also taken into consideration the common operations including Legal and Audit fees, IT operations, Human Resource, etc carried out at the company’s headquarters or head office of the bank.

According to Rohit Jain who is a partner with law firm ELP, not treating the employees of subdivisions as employees of the whole organisation is legally irrational. He says, “The interpretation adopted by the tax authorities is that an employee of an organisation should be considered as an employee of a particular office only (not the organisation as a whole) for GST-related purposes. Such an interpretation is legally and factually incorrect,”

For example, if the annual salary of the chief executive officer of a company is Rs 5 crore than this earning of CEO would be treated as a cost for the head office as the executive is located there. The tax department wants the proportionate cross charge of this cost under GST by the company to all its branches and treats this as supply which attracts GST @ 18%.

According to the theory of Income Tax department, this cost of Rs 5 crore should be apportioned to other branches located in different states and treat this as a supply of services from the head office to the branches.

According to the Tax experts, the mixup mystification about the cross-charging could imply an actual cost for the organisations. Almost in every organisation, this would have ultimately neutralised the revenue.

Read Also: Insurance & Pension Facility for GST Registered Traders

“Few sectors such as hospitals and power where no output GST is payable and in cases where the time period to avail credit has lapsed, this GST liability will lead to a significant cost,” stated by Jain.

Ritesh Kanodia who is a partner at Dhruva Advisors said, “Tax authorities have started issuing preliminary notices to companies and sought details about the methodology followed for distribution of such credits, though in either of the methods, the GST credit gets distributed as per the intent of the law. The taxpayer has been contending that the services are being consumed by the head office for carrying out its support functions and therefore require issuing a supply/cross charge invoice,” Ritesh Kanodia, partner at Dhruva Advisors.”

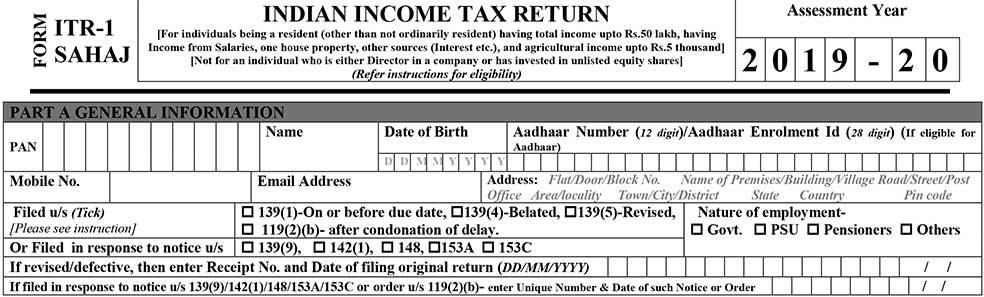

ITR 1 Form is filed by the taxpayers and the individuals being a Resident (other than Not Ordinarily Resident) having Total Income up to INR 50 lakhs, having Income from Salaries, One House Property, Other Sources (Interest etc.), and Agricultural Income up to INR 5 thousand. (Not for an Individual who is either Director in a company or has invested in Unlisted Equity Shares). Also to note down, from now onwards, as mentioned by the tax department, furnishing PAN and Aadhaar card details on the official website of the Income Tax Department is mandatory.

The income tax department has notified ITR forms for taxpayers based on their source of income in order to create a simple tax compliance structure. Therefore, you are required to furnish the return as per the source of your income.

Read Also: Gen IT Software – Fastest & Easy Income Tax Return E-Filing Software

Eligibility To File ITR 1 Online For AY 2019-20

ITR-1 is filed by the taxpayers whose income is up to Rs 50 lakhs from below-mentioned sources:

If the income is from one house property (the case where losses of previous years are carried forward are not included in this ITR)

If the source of income is pension or salary

If the source of income is other sources

If the clubbed income of minor or wife is shown, then ITR-1 can be filed only in case their source of income as mentioned in the above points.

Not Eligible for ITR 1 Filing Online for AY 2019-20

The taxpayer whose income is more than Rs 50 lakhs is not eligible to furnish this form.

Non-residents and RNOR (Residents not ordinarily resident) cannot file ITR 1.

Taxpayers who have two or more house properties are not eligible.

Assessees having income under business or profession head are not eligible.

Taxpayers who have long or short-term capital gains

Taxpayers whose income from agriculture means is greater than Rs. 5,000

The taxpayer who claims relief for foreign taxes paid or claim double taxation relief as mentioned in section 90/90A/91.

ITR 1 cannot be used by residents having any asset (including financial interest in any entity) located outside India or signing authority in any account located outside India.

Penalty if Miss the Income Tax Return Filing Deadline

As per revised rules under section 234F of IT act from 1st April, 2017 notifies that an individual is liable to pay maximum INR 10,000 penalty after missing the 31st July deadline of ITR filing. The income tax department has extended the due date till 31st August 2019 (Read notification here). While in case an individual total income does not exceed 5 lakhs then a penalty of only INR 1,000 is applicable.

Late Filing Fee Details

E- Filing Date

Total Income Below INR 5,00,000

Total Income Above INR 5,00,000

31st August 2019

INR 0

INR 0

Between 1st Sept to 31st Dec 2019

INR 1,000

INR 5,000

Between 1st Jan 2020 to 31st March 2020

INR 1,000

INR 10,000

Modifications Details in ITR 1 Sahaj Form

INR 40,000 standard deductions

No applicability on directors of any company

No applicability on individuals holding unlisted equity shares of any company

No changes in computation

ITR 1 & ITR 4 offline availability for senior-most citizens aged more than 80 years

Section wise return filing is segregated within the normal filing return and response to the notice

Salary bifurcation will be done as the standard deduction, entertainment allowance and professional tax

Pensioners column has been added in the nature of employment

A new deduction of 80TTB has been added in the deductions column

The individual income from one house property, salaries and other sources summing up to 50 lakhs, this condition retains its place even after changes

Due Date for Filing ITR 1 Online AY 2019-20

Every year ITR -1 has to be filed on or before 31st July of the following year. After that, a late fee under section 234F is levied

Applicable Income Tax Rates for FY 2018-19 (AY 2019-20)

Guide to File Income Tax Return (ITR) 1 Online:

ITR 1 is divided into 7 sections where:

Part A – General Information

This tab includes details of the following general fields:

Name

Address

PAN number

Mobile no.

Email address

Aadhar number

Return filing details

Nature of employment viz Govt/PSU/Pensioners/Other

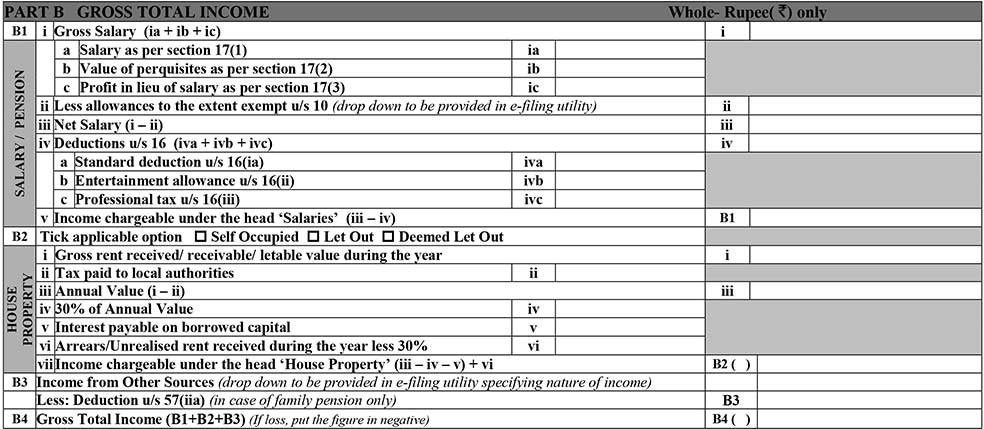

Part B – Gross total income

This tab includes details related to gross total income:

Part B1

Salary details

All the allowances which are exempted

All the value of perquisites

Net salary

Deduction in u/s 16

Income chargeable under the head ‘salaries’

Part B2

Gross Rent received

Tax paid to local authorities

Annual value

30% of the annual value

Interest payable on borrowed capital

Arrears/unrealized rent less than 30%

Income chargeable under head ‘house property’

Part B3

Income from other sources

Part B4 – Gross total income

(B1 + B2 + B3)

Part C – Deductions u/c VI-A and Taxable total income

This tab includes all the deductions and taxable total income

Here the deduction limit will be as per income tax act

80C

Value of Total deduction

Total income (B4 – C1)

Part D – Computation of tax payable

This tab includes all the valuation of tax payable

D1 Tax payable on total income

D2 Rebate u/s 87A

D3 Tax after rebate

D4 Cess on D3

D5 Total tax and cess

D6 Relief u/s 89(1)

D7 Interest u/s 234A

D8 Interest u/s 234B

D9 Interest u/s 234C

D10 Fee u/s 234F

D11 Total tax, fee, and interest

D12 Total tax paid

D13 Amount payable

D14 Refund

Exempt income

Part E – Other Information

This tab includes banking details

IFSC Code of the bank

Name of the bank

Account Number

Schedule-IT: IT Details of advance tax and self-assessment tax payments

BSR code

Date of deposit

Serial number of challan

Tax Paid

Schedule-TDS: TDS details of TDS/TCS

TAN of deductor/ PAN of tenant

Name of deductor

Gross payment

Year of tax deduction

Tax deducted

TDS/TCS credit

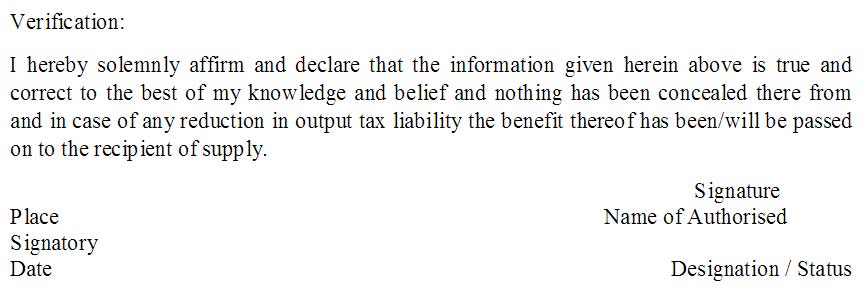

Verification

The taxpayer has to verify and self-attest the form at the last by signing the verification content after entering all the details such as name, parent name and PAN details.

Medium To Online Furnish Income Tax Return 1 (ITR)

An ITR-1 form can be furnished either in online or offline mode. In online mode, either XML needs to be uploaded or client can directly login to income tax portal and select the submission mode as “prepare and submit online”. In the case of online filing, some data can be imported from the latest ITR or form 26AS.

Also, super senior citizens (Age of 80 years or more) are exempted from the online filing of ITR.

Offline here means to furnish the return form in paper format.

File ITR 1 Online or Electronically:

While furnishing ITR-1 online, feed the details and e-verify return using EVC via Bank Account/Net Banking/Demat Account/Aadhar OTP or

Feed the details using electronic medium and send a physical copy of ITR V to Centralized Processing Centre (CPC), Bengaluru through speed post or normal post.

When you furnish the ITR-1 return form using electronic medium, the receipt will be seen in the inbox of the registered email id. It can also be downloaded from the official income tax website manually. After downloading the acknowledgement, you need to sign the form and then send to the CPC office, Bangalore before completing 120 days counting from the e-filing date. On the other side, it is not required to send the ITR V to the CPC if EVC/OTP option is used.

File ITR 1 SAHAJ Form Offline

If the age of the person is 80 or more years during the respective tax period or in the previous year.

Important Terms To Understand In ITR-1 SAHAJ Form

Notice Number: Notice Number is required to be mentioned when the taxpayer furnishes the return in answer to the notice issued by the Income Tax Department.

Revised Return: There is an option of re-file, so if you have made certain mistakes, you can rectify them again. For the FY 2018-2019, the taxpayer can furnish the revised return on or before 31 March 2020.

Advance Tax: If the tax on other income is above Rs. 10,000 in a year, the assessee is required to calculate and deposit the advance tax. This advance tax is to be paid on a quarterly basis such as on, June, December, September and March.

Annexure-less Return: Annexure-less return which means it doesn’t require to affix any documents with the ITR-1 Form.

Let’s Go Through ITR-1 Return Filing FAQs

Q.1 What documents one needs to submit while filing ITR 1 returns?

No document is needed to be submitted while filing income tax returns. However, one should keep basic documents like Form 16, balance sheet and P and L accounts of the business, shreds of investment evidence, audit reports and so on ready with him/herself. Because in some cases when the income tax department sends notice, these documents are required to be presented before the tax authorities on a later date.

Q.2 – What are the heads under which Pension and family pension are taxable?

Income from salary’ is the head for levying a tax on pension whereas family pension is taxable under the head ‘Income from other sources.

Q.3 – Who is eligible to file taxes via paper form rather than e-filing an ITR?

YEvery income tax assessee has to mandatorily e-file income tax returns. However, there are some exceptions to the standard rule wherein they can submit paper ITR forms and they do not have to file the ITRs online. They are as follows:

At present, Super senior citizens who are above 80 years of age.

PFrom AY 2019-20 onwards, Individuals having an annual income below Rs. 5 lakh and not having any refund due.

Q.4 – What amount will attract tax if the value of the gift is more than Rs. 50,000?

When the value of the gifts received from friends on any event except the wedding during a year is Rs 50,000 then the whole amount will attract tax under the head ‘Income from Other Sources’ head.

Note: Gifts are taxed on the total value of all the gifts received in the year and not on the value of the individual gifts.

Q.5 How bank accounts are reported in ITR-1?

Details of savings and current accounts which are held during any time of the previous year must be reported in Part E of the ITR form which seeks – other information. The account number must comply with the Bank’s Core Banking Solution (CBS) system. However, one need not provide details of dormant accounts which is not working since 3 years.

Q.6 – Can ITR-1 be filed in case of exempt agricultural income?

Yes, one can file ITR-1 when the agricultural income is not more than Rs 5000. But when it exceeds Rs 5000, one needs to file ITR 2.

Q.7 – Is it necessary to file an ITR if the annual income does not exceed Rs 250,000?

No, it is not necessary to file an ITR if the annual income is less than Rs 250,000. But in this case, a ‘Nil Return’ should be filed to upkeep a record which is an employment proof required while applying for a passport or loan.

Q.8 – Does dividend income from Mutual Funds need to be included in it?

Yes, dividend income from mutual funds should be included under the head ‘Exempt Income(others)’ as it is an exempt income u/s 10(35).

Q.9 – Can I file ITR-1 if I have a House Property loan?

Yes, you can file ITR-1 if you have a house property loan.

Q.10 – Should I file ITR-2 or ITR-1, if my maximum exempt income is more than Rs. 5,000? What much amount of income will be considered as exempt income?

ITR-2 has to be filed if the amount of aggregate exempted income is more than Rs. 5,000. Some incomes are tax exempt as per Section 10 of the Income Tax Act. A few examples of exempt income are as follows:

Income from Agriculture

Long term capital gain on listed shares and securities (Section 10(38)

Gratuity, Pension and Leave encashment are exempt u/s 10 of the Income Tax Act.

Maturity amount of LIC (Section 10 (10D)

Q.11 – Can I file ITR-1 if I have a Rental Income?

Yes, you can file ITR-1 if you have a rental income. Refer our guide for the step-by-step process.

Q.12 – Should Interest Income be mentioned under the head ‘Income from Other Sources ‘ while filing ITR-1 when TDS has already been subtracted?

Yes, Interest Income should always be mentioned under the head ‘Income from Other Sources’ even when tax has already been subtracted by the bank.

Q.13 – Do I still need to furnish my Bank Account details in the ITR if there is no refund due to me?

Yes, furnishing the bank details in the ITR is mandatory, regardless of refund is due or not. It is mandatory because many taxpayers pay more taxes than their tax liability. So, to enable the Income Tax Department to send refunds on time, bank account details need to be furnished.

Q.14 – How can I download the Income Tax Return Form?

Income tax return forms are available on the official website of the Income Tax Department. Simple steps to download forms are as follows:

Go to the Income Tax Department website

Click the option ‘Form/Downloads’ on the homepage.

Choose the option of ‘Income Tax Returns’ from the drop-down menu.

Now you will be redirected to the ‘Income Tax Return’ webpage. Now download the form which is appropriate according to your source of income and A.Y.

Q.15 – What is the meaning of ITR XML file?

ITR XML is a kind of file format which is generated when you file the important data of your ITR in an offline utility.

Under GST surveillance GSTR 3B is the monthly compliance form that needs to be furnished by the taxpayer mentioning the details of the outgo of his goods or services which were released during the whole month along with paying the relevant amount of tax applicable on those transactions. The form contains a separate section for mentioning the Input Tax Credit which a dealer (taxpayer) claims on his purchase of inputs for that particular month.

GSTR 1 is yet another compliance form required to be filed by the regular taxpayer seeking the details of the invoices issued by him under the purchaser’s GSTN number, the taxable amount and total invoice value. Mentioning such information in B2B invoices is mandatory as this will be computed while determining the Input Tax Credit

Parallel to this is another mechanism in which all B2B invoices get recorded in the GSTN system and automatically appear on the GSTR 2A of the purchaser. GSTR 2A form allows entries of purchases done by the recipient.

To be Noted: As per current laws, the cap of 20% (i.e. Credit reflected in GSTR 2A plus 20% ) on input tax can be availed by the taxpayer on his purchases i.e. an additional benefit of 20% is extended to the taxpayer apart from the ITC shown on his GSTR 2A return.

There are certain instances as follows:

Purchaser cum taxpayer is honest in his tax dealings but the seller fails to upload the invoice for a month and is planning to upload it in the next month.

Purchaser cum taxpayer is honest in his tax dealings but the seller uploads the invoice mentioning the incorrect GSTN, as a result, an incorrect credit is reflected in GSTR 2A of the purchaser.

Purchaser cum taxpayer is honest in his tax dealings but the seller deliberately skips to upload any of his invoices in GSTR 1.

There are disputes between the seller and purchaser related to the information entered in the forms by any of the two parties on which the purchaser can claim ITC. Invoice claimed to be uploaded in GSTR 1 of the seller and are not reflected in the GSTR 2A of the buyer causes the case of collusion and fraud.

By looking at the above examples it is clear that the recipient has paid the valid tax on the goods he has purchased from the supplier. In the majority cases, the people falling under the last category are fraudsters who want to make some quick money. The amendment made through Rule 36 (4) of the Central Goods and Service Tax Rules, 2017 is aimed at the fourth category only.

It is absolutely weird that according to a sub-rule (4) in Rule 36 which the legal administration penalises the genuine taxpayers who initiate to curb frauds committed by some fraudsters who against them. Now it is the duty of every taxpayer (Purchaser) to check on a frequent basis that his purchases are entered by his supplier correctly in the GSTR 1 form filed by him so that the same is visible in his GSTR 2A.

Moreover, the government is in action to bring in the limelight such fraudulent transactions on the basis of which some fraudsters claim the wrong availment of ITC.

Adding on to this government has made provisions to ensure that the honest purchasers get the right ITC which they deserve.

A solid mechanism in GST forms which where the purchaser can enter the details of invoices mentioning the GSTN of the supplier which can be matched back at the end of the GSTN system in the sales details entered by the supplier. Presently only the input tax credit figure which is being claimed by the taxpayer is required to be declared in the GSTR 3B form.

If a mismatch in the details entered by the honest purchaser and the seller is spotted then the notice is sent to the seller demanding the payment of the correct amount and interest charges on the unpaid tax and sales undeclared.

In the notice, the seller is either asked to pay the tax and interest charged or give his justification which will ultimately give a buzzer that whether the details by the purchaser is correct or the justification by the seller is genuine.

Tax will be paid only after filing GSTR 1 and GSTR 3B with this one can make sure that the suppliers have uploaded correct invoices by the 20th of the next month so that GSTR 2A of the purchaser gets populated with the input tax credits at the earliest.

FAQs on Availment of ITC by the Taxpayer

Q.1 For which invoices/debit notes restrictions under rule 36(4) of CGST shall apply?

Restrictions under section 36(4) of ITC is applicable to invoices/debit notes on which the credits are availed after 09/10/2019. Restrictions on claiming ITC is imposed related to invoices/debit notes, the details of which have not been uploaded by the supplier under sub-section (1) of section 37. Once the details are inserted by the supplier, the taxpayer can avail full ITC on IGST paid by him.

Q.2 The restrictions on claiming ITC are calculated supplier wise or on a consolidated basis?

Restrictions on availed ITC is not computed supplier wise. Under section 36(4) of ITC, the total payable credit is calculated by the tax officials based on the invoices eligible for credit. For invoices on which ITC cannot be claimed will be detached while calculating ITC.

Q.3 What is section 36(4)?

As per the provision under the CGST Act, there are restrictions on the availment of ITC related to invoices or debit notes for which there is no entry by the supplier in his Form GSTR 1.

Q.4 What is GSTR 1 and GSTR 2A?

Form GSTR 1 is filed (monthly or quarterly) by the seller putting in details of all his supplies along with the invoices/debit notes of supply to confirm the details. GSTR 2A is the form for the purchaser in which the details are auto uploaded as the supplier fills in his GSTR 1. Based on the information in GSTR 2A of the purchaser, ITC is availed by him.

Q.5 Can ITC be availed by the taxpayer (the purchaser) for which the invoices or debit notes are not uploaded by the supplier? If yes, how much?

ITC claimed by the taxpayer on invoices which are still not uploaded by the supplier should not go beyond 20% of the total ITC applicable on invoices uploaded by the supplier under section 37(1). The same will be confirmed by the auto-populated Form GSTR 2A of the taxpayer (purchaser). The supplier must file GSTR 1 on or before the due date.

Q.6 Is it possible for a registered taxpayer to avail ITC on Form GSTR 3B for the invoices which are not yet uploaded by the supplier in Form GSTR 2A?

Yes, but ITC claimed by the taxpayer on invoices which are still not uploaded by the supplier should not go beyond 20% of the total ITC applicable on invoices uploaded by the supplier under section 37(1).

Let’s take up an instance, where taxpayer A is eligible for ITC on 100 invoices i.e. Rs 10 Lakhs for October month which he has to mention under ITC section in Form GSTR 3B for October.

Case 1: Details of supplier’s invoices in GSTR 1 – 80 invoices involving ITC of Rs. 6 Lakhs.

20% eligible credit on missing invoices – Rs. 1,20,000 (20% of 6 Lakhs)

Total payable ITC – Rs. 6 Lakhs (for 80 invoices) + Rs. 1,20,000 (for missing invoices) = Rs. 7,20,000 (to be claimed by the taxpayer).

Case 2:

Details of supplier’s invoices in GSTR 1 – 80 invoices involving ITC of Rs. 7 Lakhs.

20% eligible credit on missing invoices – Rs. 1,40,000 (20% of 7 Lakhs)

Total payable ITC – Rs. 7 Lakhs (for 80 invoices) + Rs. 1,40,000 (for missing invoices) = Rs. 8,40,000 (to be claimed by the taxpayer).

Case 3:

Details of supplier’s invoices in GSTR 1 – 75 invoices involving ITC of Rs. 8.5 Lakhs.

20% eligible credit on missing invoices – Rs. 1,70,000 (20% of 8.5 Lakhs)

Total payable ITC – Rs. 8.5 Lakhs (for 75 invoices) + Rs. 1,50,000* (for missing invoices) = Rs. 10,00,000 (to be claimed by the taxpayer).

To be noted: In case 3, the eligible amount of ITC is deducted ensuring that the total payable amount does not cross the eligible ITC amount i.e. 10 Lakhs.

Q.7 When can one avail the ITC on the pending invoices to be uploaded by the supplier?

Taxpayers can get the credit on balance invoices added up to the succeeding month once the supplier uploads all the invoices (balance + new invoices). He can claim ITC based on the calculations of balance + current invoices uploaded by the supplier.

What is DIN (Director Identification Number) Under GST?

The Central Board of Indirect Taxes and Customs (CBIC) has taken the initiative to digitize and secure all the communication sent by it to the registered individuals & taxpayer by starting a system that would generate a Director Identification Number (DIN) as the communication will be sent by tax authorities to the taxpayers.

Director Identification Number Under Income Tax

DIN was first introduced under Income Tax Law. Now with an intent to protect the interests of GST taxpayers and to increase the accountability & transparency under the indirect tax mechanism, CBIC is starting its use under GST.

Initially, the income tax department had started this campaign which knocked off the need for the taxpayer to physically visit the Income Tax Office (IT Office) to answer the income notice.

When DIN Code Will be Used?

According to the orders by CBIC, DIN will be used in GST cases whose inquiries are going on and arrest & search warrants pertaining to them have been issued. According to the board, the documents issued post 8th November 2019 will have DIN. A DIN will confirm the authenticity of the communication.

The authenticity of such communications can be ascertained by the recipient. For this, the recipient will have to quote the CBIC-DIN of the specific communication in the window “VERIFY CBIC-DIN” on the CBIC’S official website —> www.cbic.gov.in.

The window will showcase the information about the communication only if the communication is genuine, otherwise not.

All About Director Identification Number (DIN) Code

DIN code is a digitally generated alphanumeric code by the system in the format of CBIC-YYYY MM ZCDR NNNN, wherein YYYY denotes the year in which DIN is generated, MM denotes the month in which DIN is generated, ZCDR denotes the Zone Commissionerate Division Range Code and NNNN denotes alphanumeric randomly generated code by system.

Benefits of DIN (Director Identification Number) Code

The latest introduction of director identification number code has made some of the best changes in the procedure through which the tax department and taxpayer communicates.

Lets see how the DIN provides advantages to the taxpayers:

Transparency Within the Government Department Working

Complete Conversation Between Taxpayer and Tax Department

Solve Problems of the Taxpayers

Protect the Rights of the Taxpayers

After a month of E-Assessment scheme implementation, now DIN accompanied/based communication has become mandatory. After 8th November 2019, an e-communication without digitally generated DIN under GST would be deemed to be invalid and treated as never happened communication.

The scheme of E-invoice was officially approved by the GST Council in the 37th Council Meeting. If you are looking to generate an e-invoice under GST, this is the step-by-step guide to help you.

What is GST E-invoice?

E-invoice is not an invoice that you can download or generate through the GST Portal, but it is a process of validating all the B2B invoices electronically by the GST Network (GSTN). It’s not feasible to generate e-invoices directly from the common portal.

E-invoicing or authentication is required to ensure that the invoices generated by your accounting software are valid to be used for processes like e-way bill creation and return filing. The process involves the submission of business invoices created by different accounting software to the GST Portal in order to get them verified in a common manner.

Since the invoices created by different GST return filing software may have different formats, they cannot be all fed directly to the GST system by the software. So, the government decided to introduce a standard format (Schema), which requires all the accounting software to follow a common format which can then be uploaded to the GST portal for authentication and validation.

To sum up, E-invoice is a standard mechanism or schema for data exchange between different GST billing software of different manufacturers.

How is the GST E-invoicing System Beneficial?

Reporting and authentication of B2B invoices from the common portal will ensure that GST ANX-1 and ANX-2 are auto-prepared in the new format. IT also auto prepares GSTR 1 for B2B supplies.

E-invoicing can be further used for creating e-way bills by providing only vehicle details.

Invoices uploaded by suppliers for authentication will be automatically shared with buyers for reconciliation.

The system will auto-match input credit liability with output tax. E-invoice can be created for Debit/Credit Notes, Invoices and other eligible documents.

E-invoice can be created for Debit/Credit Notes, Invoices and other eligible documents.

Step by Step Guide to Generate an E-invoice Under GST

The taxpayer or business is responsible to generate the invoice/s and then submit them to Invoice Registration Portal (IRP) for approval.

After successful verification, the portal will return the invoice to the supplier along with a unique reference number, digital signature and a QR code. The e-invoice will also be shared with the corresponding buyer on the email id provided.

Step 1: Invoice Creation

The seller/supplier will create an invoice in the prescribed format (e-invoice schema) using his/her accounting or billing software. It must have the mandatory details.

The accounting software of the supplier will generate a JSON for each B2B invoice. The JSON file will be uploaded to the IRP.

Step 2: IRN Generation

The next step would be to generate a unique Invoice Reference Number (IRN) by the seller using a standard hash-generation algorithm.

Step 3: Invoice Uploading

Now, the seller will upload JSON for each of the invoices, along with IRN, to the Invoice Registration Portal, either directly or through third-party software.

Step 4: Authentication and Signing

IRP will validate the hash/IRN attached with JSON or generate an IRN if not already uploaded by the supplier.

Then, it will authenticate the file against the central registry of GST.

Upon successful verification, it will add its signature on the invoice and a QR code to JSON.

Hash generated earlier will become the new IRN of the E-invoice. It will be the unique identity of that e-invoice for the entire financial year.

Step 5: Sharing of Data

The uploaded data will be shared with the E-way bill and GST system.

Step 6: E-invoice Downloading

The portal will send the digitally-signed JSON along with IRN and QR code back to the seller. The invoice will also be sent to the buyer on their registered email id.

Determined by Fitch Solutions, India’s fiscal deficit forecast has increased to 3.6% of the GDP for this FY from 3.4% mentioned earlier. This hike is because of the week revenue collections which is again due to dismal economic growth and government’s widening corporate tax rate cut.

“We at Fitch Solutions are revising the fiscal forecast for the central fiscal deficit which is at 3.6% of GDP (for March-April FY 19/20) which was earlier 3.4%, reflecting our view for a larger slippage versus the government’s 3.3 per cent target”.

“This is believed to be the result of weak revenue collection which is again due to depressing economic growth and a sweeping corporate tax rate cut in September”.

The council on 20 September announced to bring down the rates of corporate income taxes for domestic companies to 22% from earlier 30% including all the additional levies it will reach to 25.2%. Manufacturing units registered after 1 October will get the benefit of paying only 15% corporate tax which was previously 25%.

Fitch Solutions even stated the revenue growth forecast of 8.3% (revised by Fitch) is down the expectations of the government’s budget estimation i.e. 13.2% growth. Corporate tax rate cuts and GST collections are again held responsible for the same.

FS gave estimations on private consumption growth which is already more than half as compared to last year (3.1% in Quarter 1 of FY 2019/20) which was 7.2% in Quarter 4 of the last fiscal year 2018/19. Responsible for this is the collapse of a dominant Non-Bank Finance Company (NBFC) in the industry, the Infrastructure Leasing & Financial Services Ltd (IL&FS), in September 2018, it added.

The IL & FS’s failure between fraud accusations also caused a credit crisis for industry rivals and a subsequent surge in their borrowing costs. This saw NBFCs significantly cut back on lending activity in the months that followed which resulted in six consecutive months of year-on-year contractions in vehicle sales from March-September 2019.

According to Fitch, the growth in merchandise imports is at a low pace owing to the hike in tariff rates charged on certain goods brought in FY 2019/20 Union Budget for tax. Fitch’s expenditure growth forecast for FY 2019/20 is 12.1% (earlier 13.7%) which is again below the government’s estimated 13.4%.

Declared by FM Nirmala Sitharaman in September that the government is not cutting down on expenditures and that the distressed revenue collection will eventually be controlled owing to the government’s ability to maintain its spending targets.

It is believed that the government might restore growth through fiscal spending given a really low 5% GDP growth in Quarter 1 of FY 2019/20 vs 5.8% Growth during FY 2018/19.

The government is expecting a large capital income from RBI through its interim dividend paid in March after which it is expected that the percentage of the central deficit will be less than the Fitch’s forecast.

Read Also: GST Impact on Gross Domestic Product (GDP) in India

The RBI follows a 12-month period from July to June and pays an interim and final dividend to the government based on its profits.

Looking at the government’s earnings from RBI the interim dividend of Rs. 28,000 Cr. has been paid in March 2019. Above that, the government has received Rs. 67,400 Cr. from the central bank to brace its finance for FY 2019/20.

The biggest tax reform i.e. Goods and Services Tax is now a part of Indian Economy. A new and unified tax structure is followed for indirect taxation on the place of various tax laws like Excise duty, Service Tax, VAT, CST etc. and for sure the new tax regime is determined to eliminate the cascading effect of tax on transaction of products and services, and it will result in availability of product and services to consumers at lower price.

Recently, India accounted 5 percent growth for the Q1 of FY 2019-20, and it is now lower than China’s GDP growth rate of 6.2 percent for the same period.

Latest Update on GDP Data for FY 2019-20 1st Quarter (April to June 2019)

As per the recent data by CRISIL, the Indian economy may not see a rise over above 6.3% for the fiscal year 2020. The current data have opposed the previous suggestion of 6.9% GDP for the year.

The news is in the air due to the disclosure of the lowest 5% GDP of the country in recent years. As per the statement by crisil, “We expect growth to get some lift from the low base effect of 6.3 per cent in the second half of the FY19.”

There is a lowered 0.6% of GDP for the given financial years due to slowdown in the overall economy and revelation by the economics department responsible for foir the maintenance of the financial health of India.

GDP Data for FY 2018-19 Last Quarter (January to March 2019)

India’s GDP has been recorded at 7.7 percent in the quarter of January – March, with a fast approach towards better number than 7.0 in the previous quarter. With some expectations for 6.7 percent in the financial year 2018, to the 7.3 percent and 7.5 percent in the FY 19 and FY 20 respectively. There is some hindrance to the GDP number due to GST as speculated by the experts but still, many economists are likely to maintain around 6.5 percent.

So here in this article, we will see the GST impact on the Indian Economy.

Read Also: GST Impact on E-commerce Sector in India

GST Positive Impact of GDP

Now, There is only one tax rate for all which will create a unified market in terms of tax implementation and the transaction of goods and services will be seamless across the states.

The same will reduce the cost of the transaction. In a survey, it was found that 10-11 types of taxes levied on the road transport businesses. So the GST will be helpful to reduce transportation cost by eliminating other taxes.

After GST implementation the export of goods and services will become competitive because of nill effect of cascading effect of taxes on goods and products. In a research done by NCAER, it was suggested that GST would be the key revolution in Indian Economy and it could increase the GDP by 1.0 to 3.0 percent.

GST is more transparent in comparison to the previous law provision so it will generate more revenue to the Government and will be more effective in reducing corruption at the same time. Overall GST will improve the tax Compliances.

In a report issued by the Finance Ministry, it was mentioned that Make In India programme will be more benefited by the GST structure due to the availability of input tax credit on capital goods.

As the GST will subsume all other taxes, the exemption available for manufacturers in regards of excise duty will be taken off which will be an addition to Government revenue and it could result in an increase in GDP.

The GST regime has although a very powerful impact on many things including the GDP also. The Gross Domestic Product has the tendency to loom on the shoulders of revenue generated by the economy in a year. Still, a worthwhile point includes that the GST has the capability to extend the GDP by a total of 2 percent in order to complete the ultimate goal of increasing the per-capita income of every individual. Also, the GST scheme will certainly improve the indirect revenues to the government as the tax compliance will be further enhanced and rigid, extending the tax paying base which will add to the revenue. The increased income of the government will redirect towards the developmental projects and urban financing creating an overall implied scenario.

GST Negative Impact on GDP

In a report, DBS bank noted that initially, GST will lead to the rise in inflation rate which will remain for a year but after that GST will affect positively on the economy.

As we know Real Estate also plays an important role in Indian economy but some expert thinks that GST will impact the Real Estate business negatively as it will add up the additional 8 to 10 percent to the cost and reduce the demand about 12 percent.

GST is applied in the form of IGST, CGST AND SGST on the Center and State Government, but some economists say that there is nothing new in the form of GST although these are the new names of Central Excise, VAT, CST and Service Tax etc.

As every coin has two faces in the same way we tried here to familiarize the things related to GST with both perspective i.e. positively and negatively in this article. Despite having some factor which is being expected to affect the Economy adversely there are so many other things which are expected with a positive impact on GDP.

Now with this insertion of this sub-rule (4) under the CGST Act, the reconciliation of invoices and GSTR-2A form is mandatory, which will increase the monthly workload of taxpayers professionals or practitioners. Keeping a close eye or following up with suppliers about the uploading of invoices will also become mandatory for taxpayers claiming ITC.

The reckless reporting of B2B transactions as B2C by suppliers due to this amendment will result in non-appearance of invoices/debit notes in the recipient’s GSTR-2A. Such a time lag will also make it difficult for them to claim ITC.

Taxable entities with few suppliers belonging to the MNC/organized sector won’t be largely affected due to such an amendment. Reconciliation and follow-up will be easy for such players. However, taxable persons at lower belts with multiple vendors, especially in the FMCG sector, will find it difficult to comply with such an amendment.

CBIC Notification for CGST Rules, 2017

“(4) Input tax credit to be availed by a registered person in respect of invoices or debit notes, the details of which have not been uploaded by the suppliers under sub-section (1) of section 37, shall not exceed 20 per cent of the eligible credit available in respect of invoices or debit notes the details of which have been uploaded by the suppliers under sub-section (1) of section 37.” Check Notification

Issues that Need to be Addressed

Addressing the Mismatch Problems Between GSTR-1 and GSTR-2A:

As we know, GSTR-2A gets auto-populated based on the detailed filled in GSTR 1 from suppliers end even after passing of due date. Hence, a mismatch between invoices and updated GSTR 2A is common, making reconciliation challenging for taxpayers.

Quarterly GSTR-1 Filings by Suppliers:

The taxpayers with annual turnover less than INR 1.5 crores file quarterly returns as per GST rules. However, with Monthly ITC claiming via GST 3B return form, it is nearly impossible for anyone to reconcile monthly invoices with GSTR 2B (as it would be generated after the given quarter).

Miscellaneous Problems:

The newly inserted sub-rule has left ambiguity in terms of scenarios when the supplier needs to report invoice/debit note for a given tax period. Whether such amount will be a part of the eligible ITC for a reported tax period is still unclear. ITC can be taken as a credit of a FIFO basis or as a pro-rata basis, is also not clarified.

Legal Difficulties on Input Tax Credit

Based on Section 164(1), the government has the authority to form rules for applying the provisions of CGST Act 2017, on the basis of the recommendation of the Council. However, the provision of the CGST Act: section 16 and section 17 is not a part of such an embargo. So, invoking such restrictions by a rulemaking make is certainly not an accurate legal position. Also, it is very clear that a rule cannot override the provisions of the Act.

In actuality, Article 14 of the Constitution of India formed by Delhi High Court has been violated by the insertion of sub-rule(4) in CGST Act as it does not offer clarity between bona fide cases (the mismatch is due to the fault of the supplier) and non-bonafide cases (bogus credit claim by the recipient).

The last legal difficulty related to the insertion of new sub-rule in Act includes violation of the basic principle of law viz., Lex non-cognit ad impossibly, i.e., the law should not compel a person to do something which is impossible. With the current rule, the recipient is restricted from claiming Input Tax Credit because of the failure of the supplier in furnishing details in Form GSTR-1 on time.