For many service class people, it is a struggle to file the income tax return (ITR) or to make savings declarations at the beginning of the financial year, because many people do not have a better understanding of it. And worthwhile, by making accurate savings declarations, the individual can avoid heavy income tax and can also plan his expenses for the year.

A similar declarations is made by people who live in rented houses, and who receive house rent allowance (house rent allowance or HRA) in salaries. House rent allowance is a component of salary provided by employer to an employee to meet his rental expenses. An employee who lives in rented house can declare his rent paid for the year and claim deduction from HRA received.

To Get the Details in Quick, Let Us Go Through Some Points Mentioned:

First of all, you have to understand that the individuals who are entitled to income tax exemptions on the house rent allowance must have HRA component in salaries, and one can claim the deduction paid for the house.

HRA is a special allowance specifically granted to an assessee by his employer to meet expenditure incurred on payment of rent in respect of residential accommodation occupied by the assessee, having regard to the area or place in which such accommodation is situated and other relevant considerations.

As per section 10(13A) of the income tax act, No exemption will be available if :

the residential accommodation occupied by the assessee is owned by him, or

the assessee has not actually incurred expenditure on payment of rent (by whatever name called) in respect of the residential accommodation occupied by him

Another important thing to remember is that if you are paying home rent more than Rs.1,00,000 per year (i.e. 8,333 rupees per month), you should enter the PAN number of the landlord (even if they are a mother or father or wife) which obliges them for the income tax payment. So, in order to get income tax exemption on the house rent allowance, it is important to have pan number of the holder if the rent paid exceeds Rs. 100000 in a year.

Quantum of Exemption

Rule 2A of the income tax act prescribes the quantum of exemption available, which will be the least of the following :

HRA actually received

Rent paid in excess of 10% of salary

40% of salary (50% in case of metro-cities)

Recommended: Solved! Name Mismatch Problem (Aadhar and PAN Card) for ITR Filing?

The GSTR 3B form is a return form declared by the Indian government for the return filing only of GST implementation. The GSTR 3B form will continue till June 2019 according to the notification No. 13/2019 – Central Tax. You can read entire help guide for filing the 3B form on Indian government portal here: GSTR 3B Creation-Submission PDF, download GSTR 3B offline utility or download the 3B form in PDF format here.

A Registered dealer is mandated to file average three Returns in every month and 1 return annually under the GST. So, that total comes 37 Returns every year for the registered taxpayer. Initially, the GSTR 1, 2 and 3 were extended for the filing by the taxpayers till the next council meeting.

GSTR 3B Return Due Date

Interest and Penalty Charges

GST Council Meeting Updates

General Queries on GSTR 3B Form

Step to Filing GSTR 3B Form Online

GSTR 3B Filing By Gen GST Software

Some of the Features of Return Form GSTR 3B

Form 3B to be filed mandatorily by all normally registered taxpayers

Nil returns to be filed in case of no business. Recently, GSTN portal offers a simple and fast procedure to file GSTR 3B return. In the latest offering, the taxpayers who are filing nil returns are free from extensive filing details and will be forwarded to simple return form with minimum details. No extra tiles and details are required for this new functionality.

Summary of information about sale and purchase, available input taxcredit, tax payable, tax paid is to be furnished

All input tax credit availed and utilized will be posted in the ITC ledger

Unutilized ITC can be used in subsequent months

While filing up form 3B, don’t forget to Save partially filled form by clicking save GSTR 3B button

After pressing submit, no modification is possible therefore check the details carefully before pressing submit

If form GST TRAN-1 is submitted Click Check balance button to view the balance available for credit under the integrated tax, Central tax, State tax and Cess (including transitional credit also)

The finance ministry rolled out special provision for the form 3B return taxpayers by giving them accessibility to adjust and change the tax liability along with rectification in monthly return of form 3B. The decision has been taken in order to help the taxpayers to claim the input tax credit on the correct basis while the penalty will be exempted in the procedure. In the latest CBEC statement, it is cleared that, “as the return in Form GSTR-3B does not contain provisions for reporting of differential figures for the past month(s), the said figures may be reported on net basis along with the values for the current month itself in appropriate tables.”

The Process of GSTR 3B Filing Simplified

GSTN-3B application has been finally simplified by the GSTN of the last Wednesday. It is now user-friendly, but there are several signs that it may be used after the 31s march. Keeping in mind the problems faced by the public before, there are several changes done to modify the filing for the easy use. This is a very important step as it makes the system less rigid and reduces the chances of inadvertent errors.

GSTN has made following key changes in GSTR-3B return filing form, said by the PWC partner:

Tax Payment: In the revised version of the form, the public can see whether the tax liability is being paid by cash or credit in tax liability, before submitting the form. But in the earlier filing, a taxpayer was required to Submit the return to ascertain the tax liability amount. After submission, no changes were allowed.

Challan Generation: Now the challan gets prepared with cash amount required to be paid after taking into account the balance available in cash ledger and suggested the utilization of ITC (Income Tax Credit) in the table, with a click of a button. Earlier, the challan had to be manually filled with the amount to be paid in cash. However, the taxpayers can make the edition in the credit amount to be utilized and not to use the credit amount filled by the system.

Download Facility of Draft Return: Earlier, there was not any downloading option to save details for offline re-checking. But now there is a new option available for public convenience where drafts return can be downloaded at any stage to verify the saved details offline.

Auto-fill of Tax Amount: This step is taken to save the time and reduces the error as taxpayers now either have to fill CGST or SGCT/UTGCT, other tax amounts will be auto-filled manually.

All don’t have to Submit GSTR 3B Return Form?

(ISD) input service distributor

Composition supplier

TDS deductor

TCS collector

OIDAR (online information data access and retrieval)

Due Dates for GSTR 3B Filing

November 2018

20th December 2018

December 2018

20th January 2019

January 2019

22nd February 2019 (Due Date Revised) | 28th Feb 2019 for J&K Read Notification

The due date for return filing of GSTR 3B form for all the taxpayers is 20th of every succeeding month of filing for the month of July 2019 to September 2019. Read Notification

“The late fee shall be completely waived in case of GSTR-3B for the time period of months/quarters July 2017 to September 2018, which are furnished after 22nd December 2018 but on or before 31st March 2019”

“All the newly migrated taxpayers, a due date extended for furnishing GSTR-3B for the time period of July 2017 to February 2019 respectively till 31st March 2019”

“Press Release – Extension of due dates for filing GST returns for districts affected by Cyclone Titli and Cyclone Gaza.”

Interest on Late GST Payment & Missing GST Return Due Date Penalty

Those taxpayers, who do not pay their taxes on time as per the date scheduled by the GST Council, will have to pay an additional late fee amount at 18 percent per annum, depending on the number of days they delay the payment.

For example, If you fail to pay your tax liability on the due date, you will have to pay additional 1000*18/100*1/365 = Rs. 0.49 per day as of late fee Where Rs. 1000 is the tax liability amount, 1 is the number of delayed days and 18 is the rate of interest (annual). See the official doc attached below for complete details of GST interest late fee and penalties https://cbec-gst.gov.in/CGST-bill-e.html

In case if a taxpayer does not file his/her return within the due dates mentioned above, he shall have to pay a late fee of Rs. 50/day i.e. Rs. 25 per day in each CGST and SGST (in case of any tax liability) and Rs. 20/day i.e. Rs. 10/- day in each CGST and SGST (in case of Nil tax liability) subject to a maximum of Rs. 5000/-, from the due date to the date when the returns are actually filed.

The GST council and government again worked for the betterment of the taxpayers and gave relief by waiving off the late fees on the filing of GSTR 3B for the month of August and September. It was also learned that if in case any taxpayers paid the late fees, it would be credited back to the taxpayers’ ledger.

General Queries on GSTR 3B Form

Q. What is the difference between GSTR 3 and GSTR 3B?

GSTR 3 which was previously issued by the GST council was further replaced by the GSTR 3B which is a consolidated monthly return filing form for the payment of the net liabilities (output tax – input tax) i.e. GSTR 3B is a consolidated return form whereas GSTR 3 is a detailed form including sale/purchase details of the month

Q. How to show credit note in GSTR 3B?

For showing the credit note in the GSTR 3B, one can deduct or net-off the amount of credit note from total outward taxable supplies. GSTR 3B is only showing an aggregate total amount

Q. ITC reversal in GSTR 3B?

ITC reversal can be shown in the GSTR 3B on tab 4 B (1) “As per rule 42 & 43 of CGST/SGST rules” and 4 B (2) “Other”.

Q. How to rectify GSTR 3B?

Previously there was a reset tab in GSTR 3B and now it has been removed by the GSTN portal, hence once the GSTR 3B gets filed, it cannot be rectified now

Q. What is ITC in GSTR 3B?

The input tax credit is that amount of the tax which you have already paid on input and now will be deducted from the total amount of tax you need to pay on output. For instance When you purchase a product or service then you pay taxes on every purchase to a registered dealer and the same way you collect taxes when you sell , then the tax you paid initially on purchases will be adjusted against the taxes you collected i.e output tax (tax on sales) and balance liability of tax (tax on sales minus tax on purchase)will have to be paid to the government. This process refers to the utilization of input tax credit. So, in short, you can say Input Tax Credit is the initially paid tax on purchases or inputs.

Q. How to pay taxes while filing GSTR 3B?

One can pay taxes while filing GSTR 3B by Logging in and Navigating to GSTR-3B – Monthly Return page. Then fill up the details in Section – 3.1 i.e. Tax on outward and reverse charge inward supplies and Section – 3.2 i.e. Inter-state supplies. After that Enter ITC Details in Section – 4 i.e. Eligible ITC.

Q. How do I check my GSTR 3B status?

The steps to check GSTR 3B status are as follows:

Step 1: Access GST Portal via https://gst.gov.in.

Step 2: In the main menu, click on Track Application Status under Services.

Step 3: Enter the ARN Number. Enter the ARN number in the field provided and complete the CAPTCHA.

Step 4: Now view Status.

Q. What is the difference between GSTR 3B and GSTR 2A?

Form GSTR – 3B is a month-based summary return filed by the taxpayer by the 20th of the next month to declare their summary GST liabilities for the tax period and the completion of these liabilities in time.

Form GSTR – 2A is an auto-populated form generated in the recipient’s login, carrying all the outward supplies (Form GSTR – 1) declared by his suppliers, from whom goods and/or services have been procured by the receiver taxpayer, in a respective tax period.

A normal taxpayer needs to file GSTR-1, 2, & 3 returns for every tax period. When the due dates for filing of GSTR-1 and GSTR-2 get postponed then GSTR-3B has to be filed. And there is any mismatch between the system generated 3B and initially filed 3B then the taxpayer is compelled to pay additional tax, liability and other dues.

Form GSTR -2A is auto-populated from the Form GSTR-1/5, Form GSTR-6 (ISD), Form GSTR-7 (TDS), and Form GSTR-8 (TCS).It is generated for a recipient when the Form GSTR-1/5, 6, 7 (Tax Deductor) & 8 (Tax Collector) is filed by the supplier taxpayer. The details can be viewed by the recipient and can be updated as and when supplier taxpayer add or alter any details in their respective Form GSTR, for the given tax period. Form GSTR-2A of a tax period is available for view only.

Q. Can I file a GSTR 3B without paying the tax?

As per section 27 (3) of GST Law, GST return will be valid only if the full tax is paid by the registered taxpayer and only the valid return would certify the taxpayer to claim an input tax credit (ITC). In other words, the supplier has to pay the entire self-assessed tax and file his return to be eligible for ITC.GST returns are treated as void if filed without making GST tax payment against such GST returns. Section 28 does not allow ITC on invalid return and defines such taxable person as unqualified for utilizing such credits before clearing his self-assessed tax liability.

Q. Is there any provision for the rectification of errors in GSTR 3B?

However, there is no concept of revised return available in GST, whether for Form GSTR-3B or your regular return which means one can not modify the data after the submission of return in the GST Portal. Yet some errors can be rectified:

The Form GSTR-3B is just an interim return and the actual return for July is to be filed in Form GSTR-1, Form GSTR-2 and Form GSTR-3 by 10 October; 31 October; and by 10 November 2017 (revised dates) respectively. Hence, any correction in GSTR-3B can be duly reported via Form GSTR-1 and Form GSTR-2.

Any alterations regarding outward supplies are to report in Form GSTR-1 when the supplies are incorrectly filled FORM GSTR-3B.

While any corrections regarding inward supplies need to be reported in Form GSTR-2 like when the ITC, tax liability of inward supplies liable for the reverse charge; or any other details of inward supplies are submitted erroneous in the Form GSTR-3B.

Based on the correct details reported in the Form GSTR-1 and Form GSTR-2, the revised tax liability and eligible ITC will be displayed in your e-ledger and these details will get auto-populated in Form GSTR-3 of July 2017.

Because of the absence of the revised return concept the data can only be rectified as long as the GST form is in save status before the submission, but cannot be modified after the final submission of return.

GSTR 3B Form Revisions Under 31st GST Council Meeting

FORM GSTR-1 & FORM GSTR-3B returns are required to be filed before the filing of FORM GSTR-9 & FORM GSTR-9C

The recipient is required to avail invoice issued by the suppliers within the time period of FY 2017-18 in context to ITC till the due date for the purpose of furnishing Form GSTR 3B for the month of March 2019 pertaining to particular conditions

An additional time-window for completion of the migration process has been opened. The due date shall be extended till 31.01.2019 for the taxpayers who had not filed the complete FORM GST REG-26 but have received the Provisional ID (PID) only till 31.12.2017 for furnishing the requisite details to the jurisdictional nodal officer. Also, the due date shall be extended till 31.03.2019 for furnishing FORM GSTR-3B and FORM GSTR-1 for the period July 2017 to February, 2019/quarters July 2017 to December 2018 by such taxpayers

All taxpayers who furnish FORM GSTR-1, FORM GSTR-3B & FORM GSTR-4 for the months/quarters July 2017 to September 2018 after 22.12.2018 but on or before 31.03.2019 will not have to pay any Late Fee

Step by Step Procedure of Filing GSTR 3B Form Online

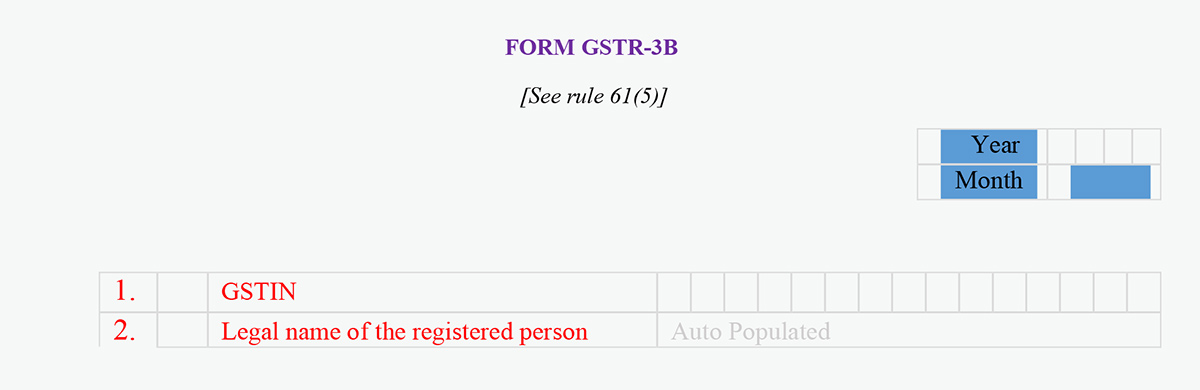

Step:1 First of all the taxpayer will have to enter his GSTIN ID very precisely with no errors. And in the second point, the legal of registered individual.

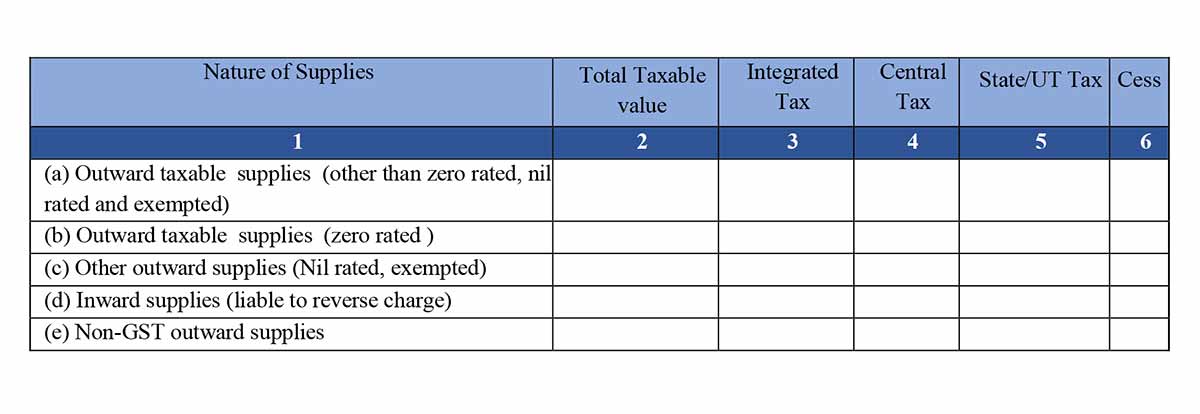

Outward taxable supplies (other than zero-rated, nil rated and exempted) – In this column, fill out all the general and non-taxable items which are sold by the business on a regular basis.

Outward taxable supplies (zero-rated ) – In the column, only zero rate tax items will be included, if any.

Other outward supplies (Nil rated, exempted) – In the column, only exempted tax items will be included, if any.

Inward supplies (liable to reverse charge) – All the supplies of inward supplies must be mentioned here which are liable for the reverse charge.

Non-GST outward supplies – Include all the Non-GST outward supplies which are not covered by the GST tax scheme.

All the details must be filled along with Nature of Supplies, Total Taxable value, Integrated Tax Central Tax, State/UT Tax, and Cess.

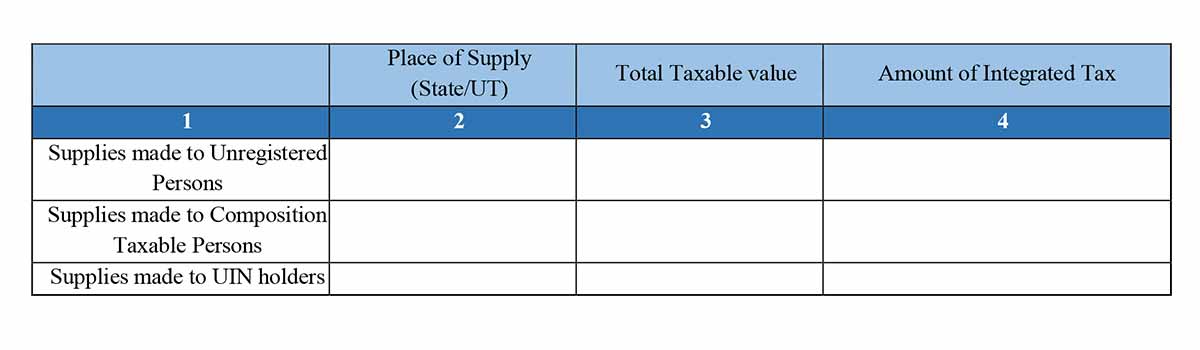

Step 3: Now the box, Of the supplies shown in above, details of inter-State supplies made to unregistered persons, composition taxable persons, and UIN holders.

Supplies made to Unregistered Persons – All the supplies details with the item name and HSN codes in the column which has been done to an unregistered dealer or individual.

Supplies made to Composition Taxable Persons – All the supplies details with the item name and HSN codes in the column which has been done to a composition scheme dealer or individual.

Supplies made to UIN holders – All the supplies details with the item name and HSN codes in the column which has been done to a UIN holder.

All the supplies must be entered with details of Place of Supply (State/UT), Total Taxable value, Amount of Integrated Tax.

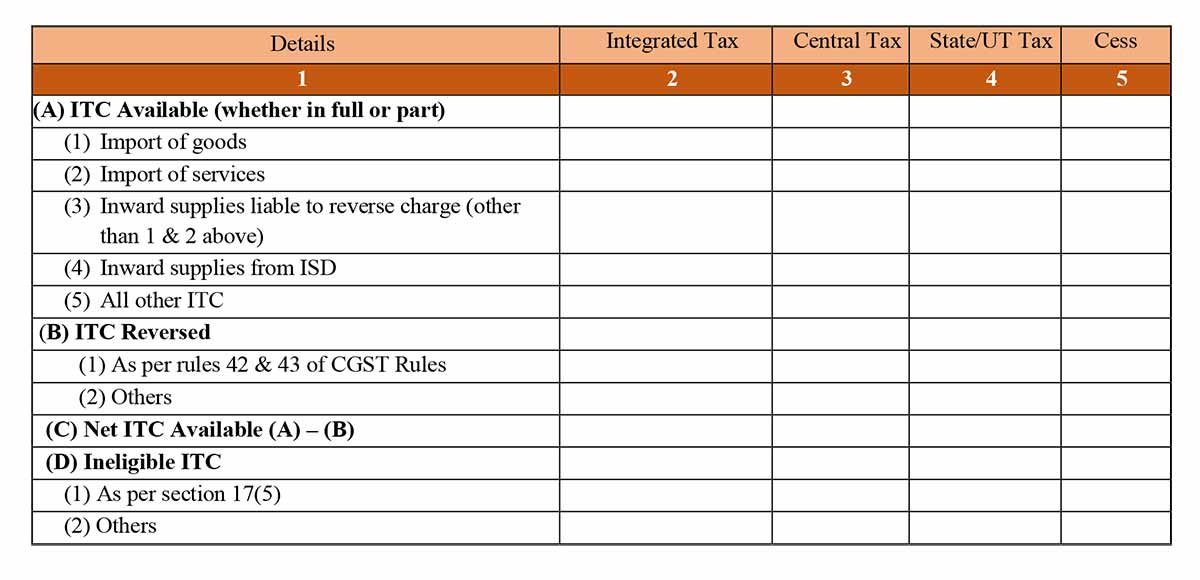

Step 4: Now, the 4th box is of Eligible ITC containing all the input tax credit demand from the taxes paid:

(A) ITC Available (whether in full or part)

Import of goods

Import of services

Inward supplies liable to reverse charge (other than 1 & 2 above)

Inward supplies from ISD

All other ITC

(B) ITC Reversed

As per rules 42 & 43 of CGST Rules

Others

(C) Net ITC Available (A) – (B)

been(D) Ineligible ITC

As per section 17(5)

Others

The required details must be filled up with Details of individual taxes to be paid accordingly, Integrated Tax, Central Tax and State/UT Tax Cess.

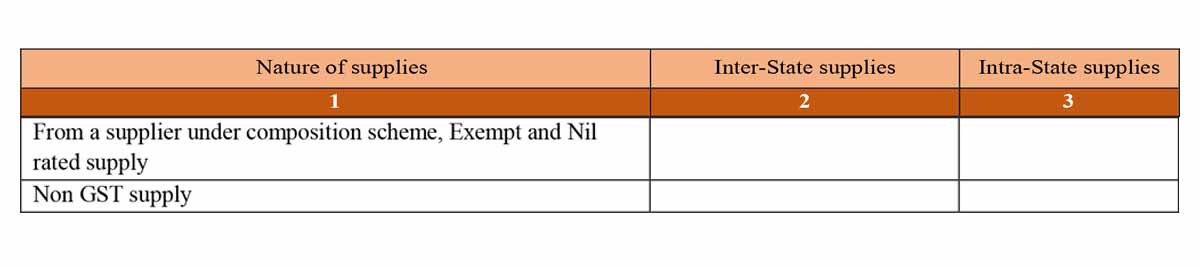

Step 5: Now coming to box 5, it includes Values of exempt, nil-rated and non-GST inward supplies:

From a supplier under composition scheme, Exempt and Nil rated supply – Include all the purchases made by unregistered dealers and composition dealers in the list.

Non-GST supply – Include all the non-GST applicable items and products of a similar category.

The taxpayer has to include all the relevant details of Nature of supplies, Inter-State supplies, Intra-State supplies, and its calculations.

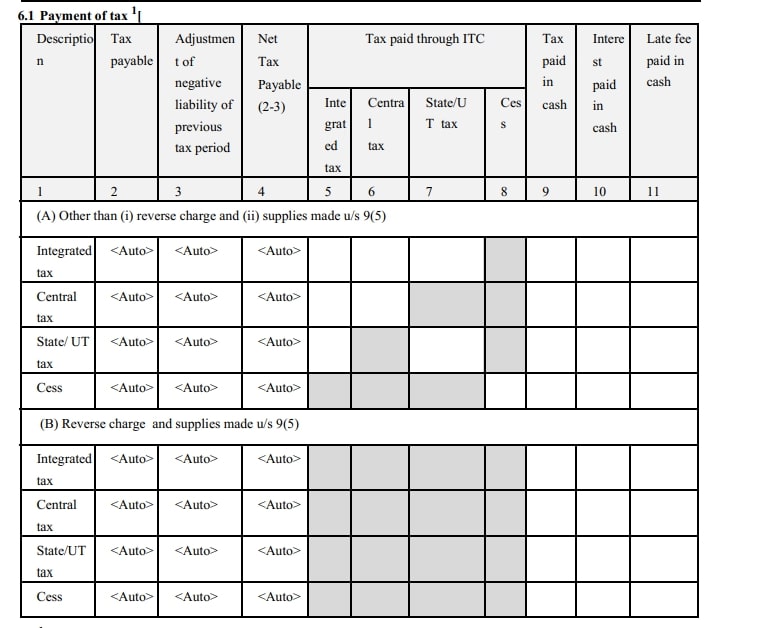

Step 6: Now comes the important box for the payment of taxes, which included a number of significant data which has to be filled up with accurate details:

Integrated Tax

Central Tax

State/UT Tax Cess

The details must be Tax payable, Tax paid- (TDS./TCS) Tax/Cess paid in cash, Interest Rate Paid through ITC – (Integrated Tax Central Tax State/UT Tax Cess)

Note: Columns which are filled in black colour must not be filled up.

Step 7: In the next box, it comes the details of TDS/TCS Credit

A proper format in which it has been mentioned all the TDS and TCS deducted for all the tax scenario including Integrated Tax, Central Tax, State/UT Tax.

Overall the Government has chosen to implement GSTR 3B form in the starting phase of GST return filing for the easy and convenient taxpaying experience for the dealers.

What is GSTR 9A (GST Composition Annual Return Form)?

The GSTR 9A is an annual GST composition return form that has to be mandatorily filed by composition scheme taxpayers. The GSTR 9A form constitutes consolidated details of SGST, CGST and IGST paid during a given financial year. In this article, SAG Infotech highlights the detailed rules and regulations as well as the step-by-step compliance procedure which composition dealers must adhere to during online filing of GSTR 9A.

In this article, you get to know about the format, eligibility, rules, and filing procedure of the annual GST composition return 9A form. Filing Procedures for each and every section as well as the subsection of the GSTR 9A composition annual return form are explained with relevant screenshots and filing guidance. The user also views and free download the GSTR 9A in PDF format.

In case of any query or doubt, readers are always welcome to seek help from our experts and professional chartered accountants. Our team of experts and CAs strives to respond and solve user doubts at the earliest. In this article, we discuss the complete GSTR 9A form which is an important composition annual return form under GST.

Meaning of GST Composition Annual Return Filing Form 9A?

GSTR 9A is a simplified annual return filed once a year by business owners and dealers who are under the composition scheme of GST. It constitutes all quarterly returns filed by the composition scheme holders (dealers/vendors) during a particular financial year. Each quarterly return must further reflect all sub-tax categories i.e CGST, SGST and IGST.

The GSTR 9A form makes composition scheme owners file detailed information of supplies made and received in a consolidated manner (monthly/quarterly returns) for a particular year.

Who is Required to File GST Return 9A?

Composition Scheme dealers under GST must file GSTR 9A before 31st December. Other prerequisites for GSTR 9A return filing include:

The business must have an annual turnover of less than Rs. 1 crore. (For North Eastern states the Annual Turnover must be less than Rs. 75 lakh)

Note – “GST Council increased the limit of annual turnover for composition scheme taxpayers to 1.50 Crores, effectively from 1 April 2019 under which the composition taxpayers allowed to file returns annually and pay tax on a quarterly basis.”

Composition dealers must keep details of all quarterly transactions (including imports and purchases) for the current Financial Year.

What are the Different Aspects of Annual GST Returns?

GSTR 9: GSTR 9 is mandatory annual return for the regular taxpayer who files GSTR 1, GSTR 2, and GSTR 3.

GSTR 9A: This annual return must be filed by a composition scheme holder under GST.

GSTR 9B: This is a mandatory return form for e-commerce operators who filed GSTR 8 during the Financial Year.

GSTR 9C: Taxpayers with an annual turnover greater than Rs 2 crores during the financial year must file GSTR 9C audit form under GST. Further, the return form mandates copies of account audits to be filed along with the form. The taxpayer must also provide a reconciliation statement of paid as well as payable tax as per audit along with GSTR 9C.

Due Date Extension for Filing GST Composition Annual Return GSTR 9A

For a given Financial Year bracket, Taxpayers under the GST CompositionScheme must submit GSTR-9A on or before 31st December of the current year. For example, if you are a composition scheme holder and you need to file GSTR-9A for FY 2017-18, then you must file the return form by 31st December 2018. In 35th GST Council meeting, the due date is revised till 31st August 2019.

GSTR 9A Penalty Norms When You Miss the Due Date

As per the penalty provisions of GSTR 9A composition annual return form, the composite taxpayer has to pay Rs. 200 per day as a penalty in which Rs. 100 consist of SGST and Rs. 100 for CGST. Also, it is to be noted that the total penalty cannot exceed 0.25% of the total turnover on which the said penalty is being levied.

31st GST Council Meeting Updates in GSTR 9A Form

Change of headings in the forms to specify that the return in FORM GSTR-9 FORM GSTR-9A would be in regard to supplies etc. ‘made during the year’ and not ‘as declared in returns filed during the year’

FORM GSTR-9A would be filed after the filing of all returns in FORM GSTR-4

Where to Download GSTR 9A Offline Utility in Excel?

The government has released GSTR 9A offline utility on its gst.gov.in portal to help taxpayers in filing the annual form.

The GSTR 9A offline utility is available on the portal when clicking on the downloads tab on the main menu

Then you have to select the returns options and click on the downloads on the GSTR 9A offline utility for downloading the zip files

The zip files have the excel sheet which will be helpful in filing the details of the return, download here

System Requirement for GSTR-9A Offline Filing

For the easy and uninterrupted functioning of the GSTR-9A Offline tool, ensure to have Operating system – Windows 7 or above and Microsoft Excel 2007 & above, installed in your system.

Process of Filing GSTR 9A Online for Composition Taxpayers

The GSTR-9 is divided into five parts and subdivided into total 17-row heads. As there is no revise facility provided by CBIC on the GST Portal so please be cautious before filing the GSTR 9A form.

Here’s a detailed closer look at each of them:

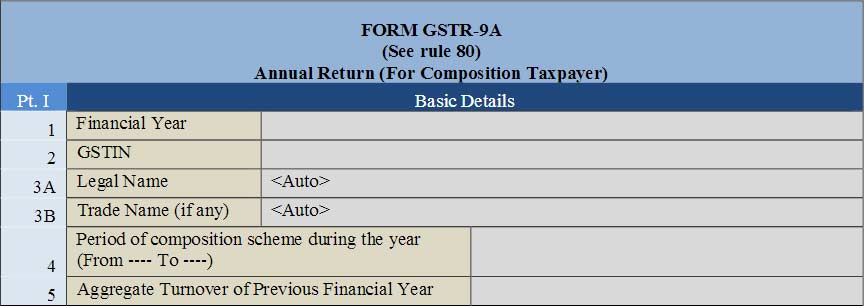

Part I Basic Details: This part is subdivided into 5 sections and 6 rows. These details are at most auto-populated.

1 Financial Year: The year for which the return has to be filed

2 GSTIN: PAN-based 15 digit GST Identification Number of the Taxpayer

3A Legal Name: Auto Populated on log-in

3B Trade Name (if any): Auto Populated on log-in

4 Period of composition scheme during the year (From —- To —-): Tax duration period

5 Aggregate Turnover of Previous Financial Year: Compounded turnover of the previous year

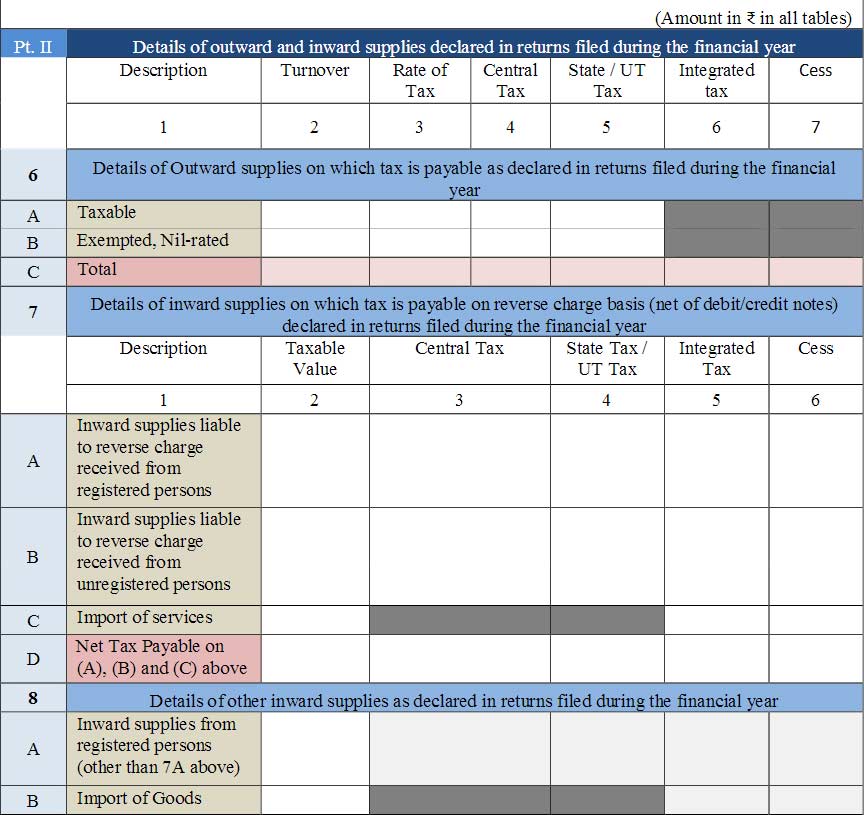

Part II Details of outward and inward supplies declared in returns filed during the financial year: This part has 3 Sections and 9 subsections. It is a consolidated summary of all returns filed during the previous Financial Year.

6A Taxable outward supplies details like Turnover, Rate of Tax Central Tax State / UT Tax

6B Exempted, Nil-rated outward supplies details like Turnover, Rate of Tax Central Tax State / UT Tax

6C Total Summation of 6A and 6B details

7A Inward supplies liable to reverse charge received from registered persons: Details include Taxable Value, Central Tax, State Tax / UT Tax, Integrated Tax Cess

7B Inward supplies liable to reverse charge received from unregistered persons: Details include Taxable Value, Central Tax, State Tax / UT Tax, Integrated Tax Cess

7C Import of services: Details of total import values, the applicable IGST and Cess

7D Net Tax Payable on (A), (B) and (C) above: Subtotal of the values in the above three sections

8A Inward supplies from registered persons (other than 7A above): Details of Inward supplies nonliable for RCM 8B Import of Goods: Taxable Value, Integrated Tax, and Cess details of imported goods

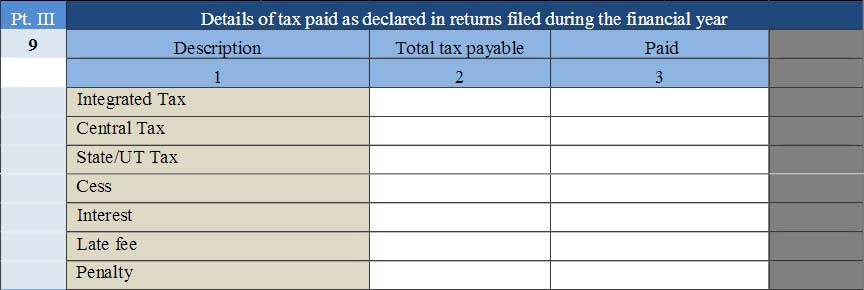

Part III

9 Details of tax paid as declared in returns filed during the financial year: This section will include the Total tax payable as well as paid under various GST tax heads during the current FY. These will include payable and already paid details of Integrated Tax, Central Tax State/UT Tax, Cess Interest, and Late fee Penalty

This section subsumes information of total tax payable and paid for all tax components in the current Financial Year. Enter payable and paid amount of GST components i.e Integrated Tax Central Tax State/UT Tax 19 Cess Interest as well as Late fee and Penalty

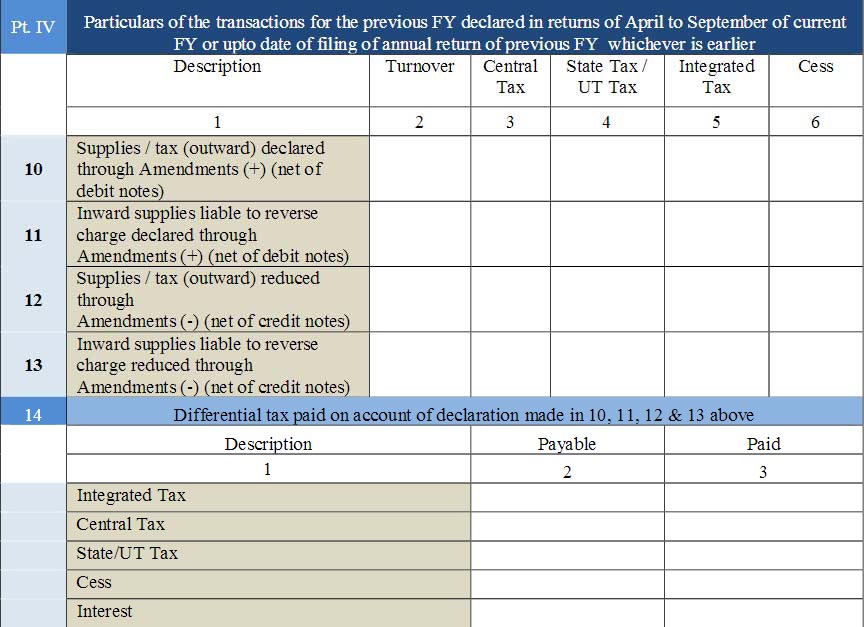

Part IV: Particulars of the transactions for the previous FY declared in returns of April to September of current FY or up to the date of filing of annual return of previous FY whichever is earlier:

10 Supplies/tax (outward) declared through Amendments (+) (net of debit notes)

11 Inward supplies liable to reverse charge declared through Amendments (+) (net of debit notes)

12 Supplies/tax (outward) reduced through Amendments (-) (net of credit notes)

13 Inward supplies liable to reverse charge reduced through Amendments (-) (net of credit notes)

14 Differential tax paid on account of declaration made in 10, 11, 12 & 13 above:

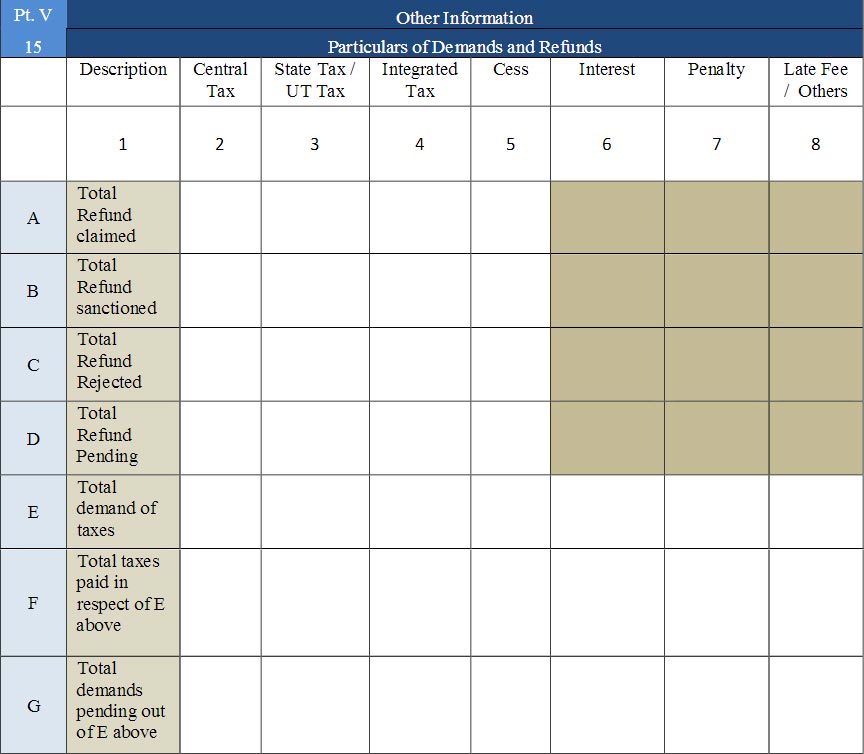

Part V Other Information:

15 Particulars of Demands and Refunds: Furnish additional information related to Demands and Refunds in this section. Detail all claims made, refunds credited, refunds pending. This part includes the following tables:

15A Total Refund claimed: Furnish bifurcated details of claims refunded including all tax components i.e Central Tax, State Tax / UT Tax, Integrated Tax and Cess

15B Total Refund sanctioned: Total tax components of refunds sanctioned i.e Central Tax, State Tax / UT Tax, Integrated Tax and Cess

15C Total Refund Rejected: Total tax components (same as above) of refunds rejected

15D Total Refund Pending: Total tax components (same as above) of refunds pending

15E Total demand of taxes: Liable tax components (same as above) at first place

15F Total taxes paid in respect of E above: Enter the detail of total tax components paid with respect to point E above

15G Total demands pending out of E above: Enter the detail of total uncleared tax components with respect to point E above

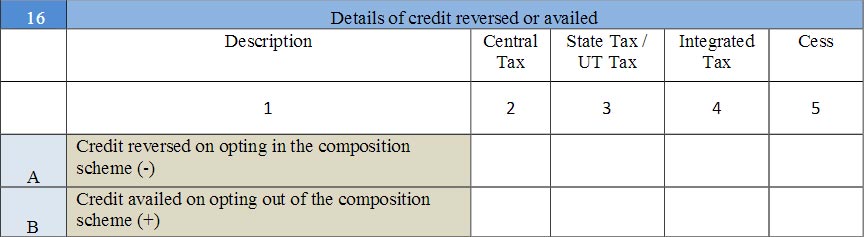

16 Details of credit reversed or availed :

16A Enter detail of Credit reversed when opting for composition scheme (-)

16B Enter the detail of Credit availed while opting out of the composition scheme (+)

17 Late fee payable and paid: Enter details of impending late fees or those which have already been paid.

17A Central Tax: Enter the payable and paid CGST

17B State Tax: Enter the payable and paid SGST

Post furnishing all appropriate details, the assessee is must digitally sign the GSTR 9A composition GST annual return form either via a digital signature certificate (DSC) or Aadhaar based signature verification to authenticate and verify the return details.

General Queries on GSTR 9A Form

Q1. Is it mandatory to file Form GSTR-9A even if someone opts out from the composition scheme in the fiscal year?

Yes, the taxpayers are compiled to file Form GSTR-9A even if he has opted out from the composition scheme for the time limit they were registered under the composition charge scheme.

Q2. Can Form GSTR-9A be filed if the registration got cancelled in the fiscal year?

Yes, The Form GSTR-9A can be filed even in the case, the taxpayer has got his registration cancelled during the mentioned fiscal year.

Q3. Can nil Form GSTR-9A be filed?

Yes, Nil Form GSTR-9A can be filed for the FY, in the following conditions when: –

any outward supply (commonly known as a sale) is not made

any goods/services (commonly known as a purchase) is not received

no liability is reported

no credit is claimed

no refund is claimed

no order creating demand is received

no late fee is there to be paid etc.

Q4. What are the prerequisites for filing Form GSTR-9A?

Pre-requisites for the filing of Form GSTR-9A are:

The taxpayer must be registered in the relevant FY and have opted for composition scheme during the financial

year even for a single day. The taxpayer must file all applicable returns i.e. Form GSTR-4, the quarterly return of the relevant FY, prior to the filing of the Annual Return.

Q5. How can a taxpayer file Form GSTR-9A?

The taxpayer can file FORM GSTR-9A through the following steps:

Navigate to Services > Returns > Annual Return

Q6. Is Form GSTR-9A return is needed to be filed at the entity level or GSTIN level?

Yes, Form GSTR-9A return is needed to be filed at GSTIN level i.e. for every single registration. In the case when the taxpayer has acquired more than one GST registrations, under the same PAN, irrespective of the same or different States, he/she is required to file annual return for each registrations individually, where the GSTIN was under composition scheme for the entire fiscal year or for a part of the year.

Q7. Is the date of filing of Form GSTR-9A extendable?

Yes, date of filing of Form GSTR-9A is extendable through notification by Government.

Q8. Does GST Portal calculate the GSTR-9A values present in different tables, based on Form GSTR-4 filed?

Values in different tables of Form GSTR-9A is auto-calculated based on Form GSTR-4. This is also downloadable in PDF format and auto-populates in different tables in Form GSTR -9A, in the format which can be edited.

Q 10. Can I file Annual return without the filing of those applicable return(s)/ statement(s) when I have not filed all my applicable return(s)/ statement(s) during the FY?

No. You are not eligible to file a return in Form GSTR-9A when you fail to file Form GSTR-4 for all applicable time durations in the relevant FY.

Q 11. Are the auto-populated details in Form GSTR-9A editable?

Yes, the edit auto-populated data in form GSTR-9A editable except the tax paid column of Table no. 9. The outward supplies details can be modified to register the actual supplies made and not just the outward supplies reported in the Returns.

Q 12. Is the consolidated summary of Form GSTR-4 made for the returns filed during the F.Y. , available for download?

Yes. A consolidated summary of all filed Form GSTR-4 statement for the relevant F.Y. is available for download in PDF format. Navigate to Services > Returns > Annual Return > Form GSTR-9A (PREPARE ONLINE) > DOWNLOAD GSTR-4 SUMMARY (PDF) option.

Q 13. Is the taxpayer allowed to download system computed values of Form GSTR-9A?

Yes, the taxpayer is allowed to download the system computed values for Form GSTR-9A in PDF format. And the same can be used as a reference by the taxpayer while filling Form GSTR-9A.

Q 14. What is the due date to file Form GSTR-9A?

The due date for filing Form GSTR-9A for an F.Y. is 31st December of the subsequent the financial year or as postponed by Government through notification from time to time.

Q 15. What happens once the COMPUTE LIABILITIES button is clicked?

When the COMPUTE LIABILITIES button is clicked, operations are initiated on details of various tables on the GST Portal at the back end and Late fee liabilities are also calculated when the computed Form GSTR-9A is filled after the due date.

Q 16. Is it mandatory to add information related to all supplies made during the F.Y.?

Yes, it is mandatory to add information related to all supplies made during the F.Y. and not only the supplies reported in the return.

Q17. Is the late fee charged in case of late filing of Form GSTR-9A?

Yes, the late fee is charged in case of a filing of Form GSTR-9A after the due date.

Q 18. Is it mandatory to pay the late fee (if applicable) for filling the Form GSTR-9A?

Yes, it is mandatory because the Form GSTR-9A cannot be filed without payment of the late fee for filing the Form GSTR-9A after a specified date.

Q 19. Is there any option available which substitutes the late fee (if applicable) payment in Form GSTR-9A?

Yes, any additional payment can be done through Form GST DRC-3 only and that too in cash. After filing Form GSTR-9A, the link is given to navigate to Form GST DRC-03 to pay tax, if any.

Q 20. What can be done if available cash balance in Electronic Cash Ledger is not sufficient to offset the liabilities?

If available cash balance in Electronic Cash Ledger is not sufficient to offset the liabilities, then additional cash, a taxpayer needs to pay is shown in the “Additional Cash Required” column. A challan may be generated by clicking on the CREATE CHALLAN button for the additional cash.

Q 21. What needs to be done when a warning message is displayed that records are under processing or processed with the error while filing Form GSTR-9A?

When a warning message is displayed that records are processed with the error or are under processing at the back end, then :

When the records are still under processing, wait for processing to be completed at the back end.

When the records which are processed with error, go back to Form GSTR-9A and take action on those records.

Q 22. In-form GSTR-9A, can the additional liability be declared if not reported earlier in Form GSTR-4?

Yes, additional liability not reported earlier in Form GSTR-4 can be declared in Form GSTR-9A. & this additional liability declared in Form GSTR-9A is to be paid through Form GST DRC-03.

Q 23. Is any Offline Tool available for filing Form GSTR-9A?

No offline tool is available for filling Form GSTR-9A but it will be introduced very soon.

Q 24. Can the Form GSTR-9A return be revised after filing?

No, the Form GSTR-9A return cannot be revised after filing.

Q 25. What consequences take place after Form GSTR-9A is filed?

After Form GSTR-9A is filed:

Generation of ARN on the successful filing of the return in Form GSTR-9A.

Delivery of SMS and an email on taxpayer’s registered mobile number and email id.

Electronic Cash ledger and Electronic Liability Register Part-I will get updated on successful set-off of liabilities (Late fee only).

Filed form GSTR-9A will be available for view/download in PDF and Excel format.

Q 26. Can Form GSTR-9A be previewed before filing Form GSTR-9A on the GST Portal?

Yes, by clicking on ‘PREVIEW DRAFT GSTR-9A (PDF)’ you can view/download the preview of Form GSTR-9A in PDF and by clicking on ‘PREVIEW DRAFT GSTR-9A (EXCEL)’ button you can view/download the preview of Form GSTR-9A in Excel format, before filing Form GSTR-9A on the GST Portal.

Q 27. Explain the different modes of signing Form GSTR-9A?

Form GSTR-9A can be filed using DSC or EVC.

(a) Digital Signature Certificate (DSC): A Digital Signature Certificate authenticates the identity electronically while providing a high level of security for online transactions by safeguarding the privacy of the information exchanged using a digital certificate. The GST Portal accepts only PAN-based Class II and III DSC.

(b) Electronic Verification Code (EVC): The Electronic Verification Code (EVC) authenticates the identity of the user at the GST Portal by generating an OTP (One Time Password) which is sent to the registered mobile phone of Authorized Signatory filled in part A of the Registration Application.

India’s economy is currently running towards 1 lakh crore or 1 trillion and fluctuates sometimes due to multiple reasons. The government is also on its toe to fetch as much as tax from the businesses.

Countries biggest industrial chief Mukesh Ambani recently made some of the staggering announcements at its 42nd annual general meeting held every year with its investors.

Mukesh Ambani revealed multiple facts and figures regarding the companies operational revenue in which one was that the Reliance industries paid a huge 67,000 crore of goods and services tax in the previous year.

The reliance chief also stated that his telecommunications company Jio also became the world’s second-largest mobile operator under which there are more than 34 crores of customers.

Not only GST, the reliance industries and all of its employees cumulatively paid an income tax return of around 12191 crores as per the figures self-declared by the Ambani.

All these announcements were done along with the big deal with the Saudi Aramco and the launching of Jio fibre for home broadband services. Although reliance is known to be a big taxpayer from decades, this was another feather in its cap.

Form MGT 7 is for the purpose of monitoring annual return details of a company. All the businesses need to fill this electronic form provided by the Ministry of Corporate Affairs (MCA). The form is further managed via electronic modes by Registrar of Companies working under MCA legislation.

The annual return has to be furnished in 60 days after the annual general meeting (AGM). The e-form is managed by the ROC (Registrar of companies) software by various tax solution companies.

What is the Eligibility to Furnish Form MGT 7?

MCA mandates all private and public companies registered as a business in India to furnish MGT 7 each year for the purpose of their annual returns. Now let us find the eligibility to furnish the MGT 7:

LLP Registration

Private Limited Company

Partnership

Sole Proprietorship

Public Limited Company

Individual person Company

Per Day Penalty If Miss the Filing MGT 7 Form

The penalty has increased in 2018 & now, the offence may cost Rs. 100 per day of delay in submitting the form. So to avoid the course of penalties one must ensure filing the form before deadlines.

Source of Downloading MGT 7

You can download the form MGT 7 from the official website of Ministry of Corporate Affairs (MCA) available under the category of “Annual filing of e-forms”.

What all Details Required in Form MGT-7 ?

MGT 7 is a requirement for all registered firms in India. The form needs to be filled with relevant details as they are on the closing of the financial year.

Required Details are Regarding:

The main office registered, the main business of the firm, details of its belonging firms, details of subsidiary companies associated with the firm.

Shares, debentures, securities and shareholdings of the company.

Debt liabilities of the company.

The updated list of members in the company or debenture holders during the current financial year.

The updated list of key personals of the company including the promoters, directors and other managers during the current financial year.

Details of key member meetings. Details of boards and its committees along with attendance details.

Remuneration of directors and key managerial personnel

A list of penalties and related offences and appeals on the company, managers or other key officials.

Related to certification of compliances and disclosures as asked in the form.

Other relevant details as required in the form.

Documents Needed with the Form:

The formalities are complete after attaching the following documents with the form under the headings:

A checklist including the names of shareholders and debenture holders

Letter of approval for the extension of the Annual General Meeting (an annual meeting of the company’s key shareholders).

Copy of MGT-8

Other documents (if mentioned in the form).

What is the Deadline or Due Date For Filing MGT 7:

The filing of Form MGT 7 is required within 60 days starting from the date of AGM.

The date of scheduling the AGM should be 15 months from the last AGM or before 30 September (6 months from the close of the financial year).

The last call for filing the MGT 7 during an FY is generally 29th November of every year.

Digital Signature is the mark of approval of electronic information same as we need a regular signature to approve manual documents. Income Tax filing is now an electronic procedure, therefore in order to confirm the authenticity of the information filled, one needs to affix the digital signature on the tax return document. I-T act 2000 gives a digital signature the importance equivalent to the regular signature.

The attested documents are proof that the taxpayer has filled the form securely without any traces of fraud.

Digital signatures are issued by Certification Authorities. Credentials required for digital signatures are the taxpayer’s name, public key, name of Certification Authority issuing the signature, expiration date of the public key, the digital signature and its serial number. It is impossible to tamper or claim forgery over a digitally signed document. Further modifications are forbidden post-signing.

Advantages of Digital Signature

One can avail to the following benefits of Digital Signature:

Digital Signature is issued by Certification Authority and any kind of tampering is impossible with the signature.

Eliminates the need for paper, thus proving to be an eco-friendly option.

It is easy to track a digitally signed document.

Cost-effective and time saver.

E-filing process becomes more efficient and the information has a value.

To understand the concept of digital signature, let’s take a sneak-peek on the components of Digital Signature:

Name: Signature cannot be recognised without a name. Signature holds the name of the person authorizing the document. This reduces the chances of tampering or fraud as the person gives the commitment of genuineness of the information under his name.

Personal Information: Credentials such as authorized person’s mobile number, current residential and office address, landline numbers, email address are equally important with name on the signature. For user’s privacy and information security, the credentials are stored in encrypted (code language) form which cannot be accessed by everybody.

Public Key: Another integral component of a signature. The sole purpose of the key is encrypting and securing a document at the time of authorisation. The key helps in the verification process. Every digital signature has an expiry date, a public key associated with the signature determines its expiration. Public key reveals the period of validity of the signature. Public Key allows resetting of the signature if needed.

Serial Number: Last but not least, the serial number is mandatory for identifying a signature. The serial number is useful for the certification authority who issues the signature. The number is to keep the data organized and with a unique identity attached to it. The serial number is important for the work-ability of the digital signature.

Grounds Where Digital Signatures are Used

Digital Signatures are of great importance in approving an e-document. Let’s check out the cases where Digital signatures are a must:

For approving documents in MS Excel, MS Word and PDF with a signature

Steps to Insert a Digital Signature in the Documents While Filing ITR

Step 1: The foremost task for the taxpayer is to register the signature on theIncome Tax Department (ITD) portal – www.incometaxindiaefiling.gov.in.

Step 2: Secondly, the taxpayer needs to login to the account using a valid user ID and password.

Step 3: On the dashboard select ‘My Account’ and then click on ‘Update Digital Certificate’ option.

Step 4: On the screen, you will find a file called ‘Store Certificate’ automatically downloading. A duplicate of your signature will be saved on your personal computer.

Step 5: Return to the web page and select “Upload your USB token”, you will land on the page with an icon saying “Select your USB Token Certificate” and “Browse” button. A selection window will come up on the screen where you need to select the file you recently downloaded.

Step 6: Click on “OK” after selecting the file. Enter the valid PIN code, which is the also Token Password, and then click on “Sign” button.

Authorities to Approach for Digital Signature Certificates

Digital Signatures are issued by the Certification Authorities. They are the licensed regulatory organisations monitored by the government-appointed Controllers.

Certifying Authorities recently performing in India are Safescrypt, CDAC CA, Capricorn CA, IDRBT, GNFC, e-Mudhra CA, NSDL e-Gov CA, Indian Air Force, Verasys CA.

The Way to Obtain a Digital Signature

One needs to get a digital certificate in order to legally authorize a digital signature. For obtaining a digital certificate, relevant documents must be furnished to the certifying authority. Authority may ask you to submit a duly signed application form along with a passport-sized photo and an identification proof. They may also ask you to register your mobile number, email address and residential or office address.

To be noted: Different countries have different document requirements to generate a digital signature.

Step-wise Guidance to Upload Income Tax Return Using Digital Signature.

Step 1:Fill the ITR form with relevant details, convert the file in an XML format and save it.

Step 2: Visit the Income Tax India portal www.incometaxindiaefiling.gov.in. Log in to your account using valid user ID and password.

Step 3: After logging in, click on “Submit Return” button and then choose the Assessment Year.

Step 4: Select the ITR Form Name from the drop-down menu.

Step 5: On-screen there will be an option asking “Do You Want To Digitally Sign The File?” Click on the “Yes” button.

Step 6: Choose your preferred digital signature type, options can be “Sign with PFX file” or “Sign With USB Token”.

Step 7: Upload the income tax returns with the help of digital signature certificate and authenticate it.

Goods and Services Tax (GST) report prepared by the Comptroller and Auditor General (CAG)’s has hoisted many concerns. However, according to tax professionals, many relevant facts have not been thought through by the government auditor.

CAG raised concern on GST of same nature being contingent to diversified tax rates by illustrating the applicability of distinctive GST on different room rents of hotels and lodges.

For instance, rent up to ₹1,000 per day is GST exempt, while it attracts GST at 12 per cent if it goes higher than ₹1,000 but lower than ₹2,499. And the GST rate increases to 18 per cent for rents between ₹2,500 to ₹7,499 and goes further higher to 28 per cent if per day room rent is more than ₹7,499.

However, as reported by the tax experts, the auditor is averting the fact that the same issues have already been discussed by the GST Council when it concluded that levying the same GST on the room rate for a room in a small lodge and the room in a five-star hotel would be unjust and irrational.

The CAG discovered many other concerns in its GST report. According to them, system certified Input Tax Credit (OTC) via ‘invoice matching’ is unfixed & displaced even after two years of GST regime. Further, the smooth and systematised e-tax system still seems evasive.

In this regard, the experts say that one needs to reconsider the decision and outlook of the GST Council.

GST system is designed in such a way that invoice matching is the essence of this system and so it becomes an inevitable need for taxpayers to comply with it at the beginning itself.

During the VAT regime, there was a need to comply with invoice matching for any of the central taxes. Although some of the states still practised invoice matching before GST regime also but invoice matching was elementary in possibilities of bogus ITC.

Under GST, ITC would be available only when invoices are uploaded in the system.

At present, two return forms – GSTR 1 & GSTR 3B provide invoice matching and as the new system is actualising in phases, more and more invoice matching will enter in through different return forms.

The downfall in the revenue of subsumed taxes (omitting central excise on petroleum and tobacco) by 15 per cent in 2017-18 concerning the year 2016-17, is another post-GST observation by the CAG.

On this subject, the tax experts bring attention to two significant points — rate cut down after the commencement of GST, and compensation cess consideration when comparing revenues.

The rates were brought down in the period beginning from November 2017 and this further brought immediate revenue effects. Comparing the revenues of 2016-17 with the 2017-18 (after GST implementation) without considering the implication of the cess would be puzzling, as stated by the tax experts.

Here the argument may arrive that the cess is solely for the compensation payment, it cannot be avoided when a comparison between post and pre-GST periods is done.

However, the compensation cess has been extracted out of the total indirect tax rates which were leviable in the pre-GST period.

One can not refuse the fact that an increment in returns filings should be one of the main aims of the tax authorities. So, one needs to notice the number of taxpayers pre and post GST regime i.e. about 60 lakh vs 1.18 crore, they said.

In terms of percentage, there have different graphs of return filing over different periods but overall it has witnessed substantial growth. Approx 75 lakh assesses have filed returns by July 31st for the month of June and this number is anticipated to rise further higher.

The report prepared by CAG has been studied by the Public Accounts Committee (PAC), and now PAC will take into consideration the government’s responses on various findings that have been made by CAG.

Maharashtra is ahead in the league in terms of GST collections in the country. It is estimated by the officials that, the state has managed to gather Rs. 1.70 crore as GST which is 15% of the aggregate GST collection of the nation. The contribution is titled as the highest GST collection in India. Finance minister Sudhir Mungantiwar claims Maharashtra to be India’s fastest-growing state which has also positively affected the GST revenue collection of the state. “Growth rate of Maharashtra continues to go high on the graph. There is an 8% increase in the GST collection this year as compared to the last financial year.” says finance minister.

He further added in the statement that the GST scale is heading towards progress. They have eliminated all the complexities of GST filing system, to enable timely submission of GST returns with complete accuracy. GST compliance is now easy for the taxpayers and also there is a huge coverage of eligible taxpayers under the GST regime.

Maharashtra has an established economy and there are many factors to prove the fact. The state also goes high on the graphs of per capital income, the fact is revealed in the growth of GST this year. The scenario is in favour of the businessman as well as customers. The businessman is getting a discount in the as the authority is cutting charges on GST and customer is also getting goods at reasonable rates.

The government has a vision of making India a nation with 5 trillion dollar economy and is working hard for the cause. This is the solid achievement of the tax government that the total number of taxpayers has increased to 15.34 lakh taxpayers in the current year from 7.79 lakh taxpayers in the previous year.

According to the specialists, the manufacturers and wholesalers who supply a discount to retailers to pass on to the customers, GST on which is creating confusion and pushing towards possible legal proceedings. The retailers say that GST on discount can put them into a difficult situation following the government’s recent decision.

In June 2019, the Central Board of Indirect Taxes and Customs (CBIC) had explained that the discount extended to dealers from the manufacturers and wholesalers assists in growing sales of retailers and this way tax considerable amount is passing on to retailer via the supplier. While the amount (discounts) needs to be a part of the transaction value between the retailer and consumers on which the Goods and Services Tax will be paid.

According to the experts, this leads to confusion when a purchase takes place. Consequently, there are high chances of raising any dispute between dealer and consumer because the latter often won’t understand and don’t want to pay additional amount as the tax on passed discount apart from the calculated sale price. Hence, the tax on discount passed to the consumer is an additional burden to retailers.

To understand it better, CBIC passed a GST circular on 28 June which explains if any discount is provided by the supplier to retailers without any obligations of depicting services as an advertisement campaign or special sales drive, the discount won’t be considered for GST. on the other hand, if the manufacturer or supplier put obligations to the retailer on the provided discount, that cut off will be liable for GST. For such cases, the tax authority had already urged to explain discounts separately as a transaction between the supplier and the retailer apart from the sale of goods made to end consumer.

“The clarification on discounts with an obligation of passing it to the recipient, forming a part of the value on which GST is leviable (even while the said is not commercially payable by the recipient) opens a Pandora’s box for most industry players; essentially because companies had always viewed these discounts as price reductions and not included them for payment of GST,” said an industry expert.

The disputes on tax on discounts have already been witnessed before the GST tax regime. In 2012, a dispute between the central excise commissioner, Mumbai and Fiat India (P) Ltd was produced against the supreme court. Wherein declared wholesale price by the company was lower than the production cost, can’t be considered as a normal price for levying excise duty as it results in short payment of tax. The decision was that discount given to the consumers for gaining market penetration would be considered taxable.

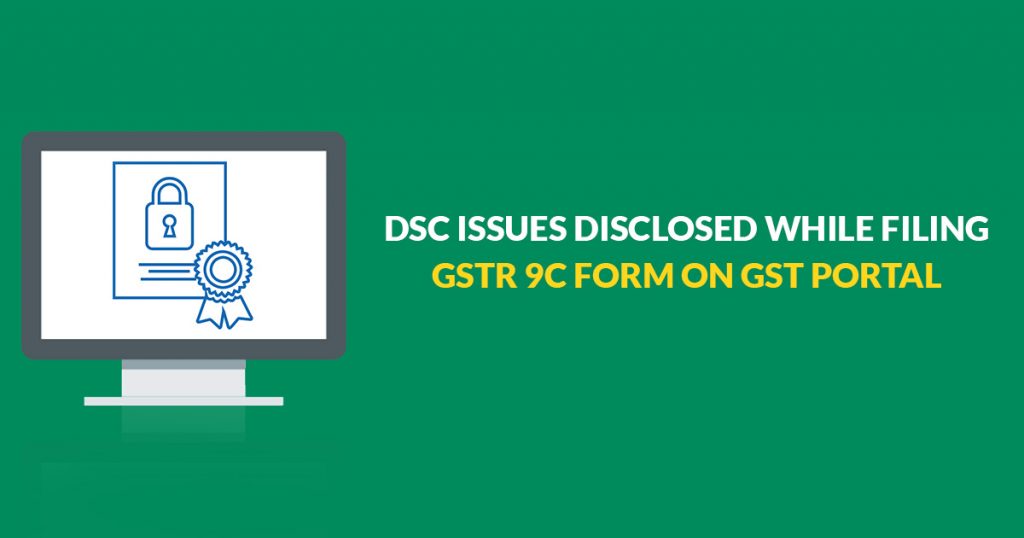

Every registered taxpayer whose turnover of an F.Y. is more than the specified limit of INR 2 crores u/s (5) 35 of the CGST Act shall get his accounts audited by a chartered accountant or a cost accountant and shall furnish its copy and a reconciliation statement in FORM GSTR-9C.

Here we will discuss the complete GSTR 9C DSC issues into 2 parts divided into Part A & Part B.

GSTR 9C Part A – Issues under DSC

Digital Signature Certificates (DSC): Digital Signature Certificate is an electronic or digital format of authorization and plays the role of evidence of an individual’s identity for the purpose of online transactions and filings.

While filing Form GSTR-9C on GST Portal, you may encounter some issues related to DSC Part-A, some of them are highlighted here along with the quick fix.

Taxpayers may use PAN-based Class 2 or Class 3 DSC on GST Portal

Make sure that PAN entered and PAN mentioned in DSC is the same, in the case of PAN verification failed error.

Make sure that DSC is installed / token is plugged in your system.

In case of issues on registration or signing DSC on the GST Portal, ensure that emSigner is started.

When emSigner server is started to → Stop the server > Restart the emSigner server as ‘Run as Administrator’.

When emSigner server is not started to → Start the emSigner server as ‘Run as Administrator’.

In case of error after clicking the PROCEED button or invisible WebSocket, restart the emSigner.

Open the GSTR-9C Offline Utility Excel Worksheet > Include the table-wise details in the Worksheet > Create Preview PDF file > Access the Draft Form GSTR-9C

Create JSON File which auditor will attest by affixing his/her DSC.

Send the attested JSON File to the taxpayer for uploading it on GST Portal.

Upload The prepared GSTR-9C Statement

Taxpayer Uploads the attested JSON File on GST Portal using his/her DSC Save Form on GST Portal.

Signature the Form and finish the filing of Form GSTR-9C on GST Portal.

Note: While signing generated JSON File, by using his/her DSC, Auditor should make sure that

HTML file name ‘WSweb’ and ‘GSTR_9C_Offline_Utility’ is in the same folder to create the JSON and emSigner is installed in your system.