A glance on the latest scrutiny reveals that 15% of Indore dwellers are filing annual GST return while rest in the city are still struggling to understand new tax compliance legislature. Taxpayers in the city are worried about the fast-approaching due date as well as other complexities of the new tax regime are requesting the authorities for exemptions from filing annual returns of 2017-18.

Small traders are incapable of filing Form 9, 9A and 9C. Looking at their situation Ahilya Chamber of Commerce and Industry goaded to exempt taxpayers from filing the very first year’s returns. Revealed by one of the key professionals in Ahilya Chambers, “Excluding some giant corporates, the fulfilment of the requisites asked in annual returns is near to impossible for small businessmen due to which they are unable to file GST returns. As we are e-filing the monthly returns, the software should automatically assemble the annual return data for taxpayer’s convenience.”

4 lakh registered taxpayers in Madhya Pradesh are capable of compiling annual GST returns which is nearly 15% of the total registered taxpayers in the state, figures revealed by the officials working in state GST department. Complexities in the nature of return filing forms and lack of error rectifying measures are held responsible by the officials for such a situation in the state.

Read Also: Free Download Gen GST Software for GSTR 9, 9A & 9C Filing

Some industries want the due date of return filing to extend from current 31st August. They are urging the government to do the needful so that they can get enough time for modifying their returns.

State GST department does not consider it to be a good sign, that only 15% of the registered taxpayers have accurately filed their annual returns on time. Looking at the current scenario, it is estimated that the last date of filing the annual returns may extend.

CAJobs is the leading online job search portal in India for the Chartered Accountants (CAs), Chartered Secretaries (CS) and other qualified accounting and finance professionals in India. This premier online CA job search site has been established by The Institute of Chartered Accountants of India (ICAI ) in 2018. ICAI is leading and a well-renowned statuary accounting body in India that has been established 70 years ago by an Act of Parliament. It undertakes the role of forging all the key rules, regulations and provisions related to the accountancy profession in India.

Since its launch is 2018, this unique CA job search portal has helped companies in the selection & recruitment process of talented CA, CS, and other accounting professionals. This one-stop job search portal has also assisted CAs to find suitable job vacancies in differnet accounting & finance firms based on multiple filters like salary compensation, experience, etc.

Frequently asked questions (FAQs) by CA job seekers related to CAJobs Portal:

Q.1 – How can an ICAI/ CMI&B member register on the CAJOBS Portal?

The members should visit https://cajobs.icai.org/ After landing on the page→ enter Members Tab → Login/Register

Point to note:

The user name for the members would be their ICAI membership number, and the password would be the date of birth (D.O.B) in DD/MM/YYYY format. In case a particular candidate has already registered https://cmib.icai.org/ in the ongoing placement drive, they should use those credentials while logging in.

Q.2 – How to apply for a job on the CAJOBS Portal as an ICAI member?

After Login and profile update on the portal, the relevant jobs matching member profile will be shown on the user dashboard for directly apply process.

Q.3 – What benefits can a member receive while applying for jobs through CAJOBS Portal?

Here are some of the member benefits when they apply for a job through CAJOBS portal

Find accounting and finance vacancies from primary to top-level easily

One-stop job portal to find all CA and finance field-based vacancies in India

Search and sort CA jobs based on numerous filters like featured jobs, premium jobs, most viewed jobs hot jobs, etc

RecieveTimely job alerts

Track Job application on the go

See relevant job recommendations and receive customized system-based SMS or Emails

Filing Form

Frequently asked questions (FAQs) by CA employers regarding CAJOBS Portal:

Q.4 – How does a company register itself on the CAJOBS Portal?

Here are the detailed steps for employer registration:

Visit https://cajobs.icai.org and click on the corporate tab

2 Fill up details in the new employer registration form

Update company profile and subscribe to a subscription package

Click submit and start posting CA jobs through employer dashboard.

Q.5 – How to get access to various services offered by the CAJOBS Portal to employers or companies?

Once the CMI&B office approves the employer registration request & other details, the company account gets activated. The company should also subscribe to an annual package for availing CAJOBS Portal services.

Q.6 – What type of jobs can be posted by companies on CAJOBS portal?

Employers can post Regular Jobs, Part Time Jobs, Contractual Jobs, Flexi hours Job, Classified, Featured Jobs etc.

Q.7 – What benefits companies may avail by posting jobs on CA JOBS Portal?

Here are some of the employer benefits when posting a job through CAJOBS portal:

Opportunity to hire talented and skilled Chartered Accountants available at one place.

Automate interview scheduling

Arrange interviews through video conferencing

Easy payment procedure through integrated payment gateway on the portal.

Find relevant candidate profile based on your entered preferences.

Easily and quick candidate-job screening process with an advanced search option.

Latest Update as per 20th August “Effective date to not allow e-way bill generation for not filing returns for >2 months, extended till Nov 21.”

Recently, some vital provisions & rules related to the E-way bill system has been added by the government that will come in effect from Nov 21st 2019. An important rule-138E has been recently added by the government via notification no. 36/2019-Central Tax, dt. 20-08-2019, which contain the following features:

If the GST returns have not been furnished for the last two months by the regular dealers OR

If the GST returns are not submitted for the previous two quarters by the composition dealers

Then,

Such dealers would simply be prohibited from generating E-way Bill on the official GST E-way bill Portal.

For such cases, only the Jurisdictional Commissioner would be given the authority to generate bills that too with permission or order.

What should the Dealers do to avoid such a scenario?

Two things must be taken care of by dealers:

Fill the GST Returns up to April 2019 before or on Nov 20th 2019 to continue the facility to generate E-way bill.

E-way bill would not be generated, in case, you fail to file your GST returns correctly.

Therefore, every registered taxpayer must strictly adhere to the government guidelines and file all their pending returns until September 2019 to avoid the 11th-hour rush.

Provisions Recently added by the government pertaining to E-way Bill System

138E (Restriction on furnishing of information in PART A of FORM GST EWB-01)

As per this new rule, no person (including a consignor, an e-commerce operator, consignee, transporter, or a courier agency) would be allowed to submit details in PART A of FORM GST EWB-01 on behalf of a registered person/taxpayer (whether as a supplier or recipient), who

(a) has not furnished the GST returns for two consecutive tax periods tax under section 10; or

(b) has not filed his/her returns for the last two months, as a person who differs from the one mentioned in clause (a).

Although, the Commissioner can allow such person or taxpayer to fill such information in PART A of FORM GST EWB-01 depending upon the validity of reasons that are given by him in writing.

Read Also: Why Worry? Download Free, Gen GST Software for Easy GST Return Filing

It further added that the affected person will be given a reasonable opportunity to explain his/her case before passing any order to reject their request to fill information in PART A of FORM GST EWB-01 under the first provision.

Also, the permission granted or rejected by the Commissioner of UT tax or Commissioner of State tax must be treated as the permission granted or rejected by the Commissioner himself/herself.

The GSTR 3B form is a return form declared by the Indian government for the return filing only of GST implementation. The GSTR 3B form will continue till June 2019 according to the notification No. 13/2019 – Central Tax. You can read entire help guide for filing the 3B form on Indian government portal here: GSTR 3B Creation-Submission PDF, downloadGSTR 3B offline utility or download the 3B form in PDF format here.

A Registered dealer is mandated to file average three Returns in every month and 1 return annually under the GST. So, that total comes 37 Returns every year for the registered taxpayer. Initially, the GSTR 1, 2 and 3 were extended for the filing by the taxpayers till the next council meeting.

GSTR 3B Return Due Date

Interest and Penalty Charges

GST Council Meeting Updates

General Queries on GSTR 3B Form

Step to Filing GSTR 3B Form Online

GSTR 3B Filing By Gen GST Software

Some of the Features of Return Form GSTR 3B

Form 3B to be filed mandatorily by all normally registered taxpayers

Nil returns to be filed in case of no business. Recently, GSTN portal offers a simple and fast procedure to file GSTR 3B return. In the latest offering, the taxpayers who are filing nil returns are free from extensive filing details and will be forwarded to simple return form with minimum details. No extra tiles and details are required for this new functionality.

Summary of information about sale and purchase, available input taxcredit, tax payable, tax paid is to be furnished

All input tax credit availed and utilized will be posted in the ITC ledger

Unutilized ITC can be used in subsequent months

While filing up form 3B, don’t forget to Save partially filled form by clicking save GSTR 3B button

After pressing submit, no modification is possible therefore check the details carefully before pressing submit

If form GST TRAN-1 is submitted Click Check balance button to view the balance available for credit under the integrated tax, Central tax, State tax and Cess (including transitional credit also)

The finance ministry rolled out special provision for the form 3B return taxpayers by giving them accessibility to adjust and change the tax liability along with rectification in monthly return of form 3B. The decision has been taken in order to help the taxpayers to claim the input tax credit on the correct basis while the penalty will be exempted in the procedure. In the latest CBEC statement, it is cleared that, “as the return in Form GSTR-3B does not contain provisions for reporting of differential figures for the past month(s), the said figures may be reported on net basis along with the values for the current month itself in appropriate tables.”

The Process of GSTR 3B Filing Simplified

GSTN-3B application has been finally simplified by the GSTN of the last Wednesday. It is now user-friendly, but there are several signs that it may be used after the 31s march. Keeping in mind the problems faced by the public before, there are several changes done to modify the filing for the easy use. This is a very important step as it makes the system less rigid and reduces the chances of inadvertent errors.

GSTN has made following key changes in GSTR-3B return filing form, said by the PWC partner:

Tax Payment: In the revised version of the form, the public can see whether the tax liability is being paid by cash or credit in tax liability, before submitting the form. But in the earlier filing, a taxpayer was required to Submit the return to ascertain the tax liability amount. After submission, no changes were allowed.

Challan Generation: Now the challan gets prepared with cash amount required to be paid after taking into account the balance available in cash ledger and suggested the utilization of ITC (Income Tax Credit) in the table, with a click of a button. Earlier, the challan had to be manually filled with the amount to be paid in cash. However, the taxpayers can make the edition in the credit amount to be utilized and not to use the credit amount filled by the system.

Download Facility of Draft Return: Earlier, there was not any downloading option to save details for offline re-checking. But now there is a new option available for public convenience where drafts return can be downloaded at any stage to verify the saved details offline.

Auto-fill of Tax Amount: This step is taken to save the time and reduces the error as taxpayers now either have to fill CGST or SGCT/UTGCT, other tax amounts will be auto-filled manually.

All don’t have to Submit GSTR 3B Return Form?

(ISD) input service distributor

Composition supplier

TDS deductor

TCS collector

OIDAR (online information data access and retrieval)

Due Dates for GSTR 3B Filing

November 2018

20th December 2018

December 2018

20th January 2019

January 2019

22nd February 2019 (Due Date Revised) | 28th Feb 2019 for J&K Read Notification

February 2019

20th March 2019

March 2019

23rd April 2019 (Revised)

April 2019

20th May 2019 (Others)20th June 2019 (Odisha) Read Notification

May 2019

20th June 2019

June 2019

20th July 2019

July 2019

22nd August 2019 | (Revised)

August 2019

20th September 2019

September 2019

20th October 2019

Note:

The due date for return filing of GSTR 3B form for all the taxpayers is 20th of every succeeding month of filing for the month of July 2019 to September 2019. Read Notification

“The late fee shall be completely waived in case of GSTR-3B for the time period of months/quarters July 2017 to September 2018, which are furnished after 22nd December 2018 but on or before 31st March 2019”

“All the newly migrated taxpayers, a due date extended for furnishing GSTR-3B for the time period of July 2017 to February 2019 respectively till 31st March 2019”

“Press Release – Extension of due dates for filing GST returns for districts affected by Cyclone Titli and Cyclone Gaza.”

Interest on Late GST Payment & Missing GST Return Due Date Penalty

Those taxpayers, who do not pay their taxes on time as per the date scheduled by the GST Council, will have to pay an additional late fee amount at 18 percent per annum, depending on the number of days they delay the payment.

For example, If you fail to pay your tax liability on the due date, you will have to pay additional 1000*18/100*1/365 = Rs. 0.49 per day as of late fee Where Rs. 1000 is the tax liability amount, 1 is the number of delayed days and 18 is the rate of interest (annual). See the official doc attached below for complete details of GST interest late fee and penalties https://cbec-gst.gov.in/CGST-bill-e.html

In case if a taxpayer does not file his/her return within the due dates mentioned above, he shall have to pay a late fee of Rs. 50/day i.e. Rs. 25 per day in each CGST and SGST (in case of any tax liability) and Rs. 20/day i.e. Rs. 10/- day in each CGST and SGST (in case of Nil tax liability) subject to a maximum of Rs. 5000/-, from the due date to the date when the returns are actually filed.

The GST council and government again worked for the betterment of the taxpayers and gave relief by waiving off the late fees on the filing of GSTR 3B for the month of August and September. It was also learned that if in case any taxpayers paid the late fees, it would be credited back to the taxpayers’ ledger.

General Queries on GSTR 3B Form

Q. What is the difference between GSTR 3 and GSTR 3B?

GSTR 3 which was previously issued by the GST council was further replaced by the GSTR 3B which is a consolidated monthly return filing form for the payment of the net liabilities (output tax – input tax) i.e. GSTR 3B is a consolidated return form whereas GSTR 3 is a detailed form including sale/purchase details of the month

Q. How to show credit note in GSTR 3B?

For showing the credit note in the GSTR 3B, one can deduct or net-off the amount of credit note from total outward taxable supplies. GSTR 3B is only showing an aggregate total amount

Q. ITC reversal in GSTR 3B?

ITC reversal can be shown in the GSTR 3B on tab 4 B (1) “As per rule 42 & 43 of CGST/SGST rules” and 4 B (2) “Other”.

Q. How to rectify GSTR 3B?

Previously there was a reset tab in GSTR 3B and now it has been removed by the GSTN portal, hence once the GSTR 3B gets filed, it cannot be rectified now

Q. What is ITC in GSTR 3B?

The input tax credit is that amount of the tax which you have already paid on input and now will be deducted from the total amount of tax you need to pay on output. For instance When you purchase a product or service then you pay taxes on every purchase to a registered dealer and the same way you collect taxes when you sell , then the tax you paid initially on purchases will be adjusted against the taxes you collected i.e output tax (tax on sales) and balance liability of tax (tax on sales minus tax on purchase)will have to be paid to the government. This process refers to the utilization of input tax credit. So, in short, you can say Input Tax Credit is the initially paid tax on purchases or inputs.

Q. How to pay taxes while filing GSTR 3B?

One can pay taxes while filing GSTR 3B by Logging in and Navigating to GSTR-3B – Monthly Return page. Then fill up the details in Section – 3.1 i.e. Tax on outward and reverse charge inward supplies and Section – 3.2 i.e. Inter-state supplies. After that Enter ITC Details in Section – 4 i.e. Eligible ITC.

Q. How do I check my GSTR 3B status?

The steps to check GSTR 3B status are as follows:

Step 1: Access GST Portal via https://gst.gov.in.

Step 2: In the main menu, click on Track Application Status under Services.

Step 3: Enter the ARN Number. Enter the ARN number in the field provided and complete the CAPTCHA.

Step 4: Now view Status.

Q. What is the difference between GSTR 3B and GSTR 2A?

Form GSTR – 3B is a month-based summary return filed by the taxpayer by the 20th of the next month to declare their summary GST liabilities for the tax period and the completion of these liabilities in time.

Form GSTR – 2A is an auto-populated form generated in the recipient’s login, carrying all the outward supplies (Form GSTR – 1) declared by his suppliers, from whom goods and/or services have been procured by the receiver taxpayer, in a respective tax period.

A normal taxpayer needs to file GSTR-1, 2, & 3 returns for every tax period. When the due dates for filing of GSTR-1 and GSTR-2 get postponed then GSTR-3B has to be filed. And there is any mismatch between the system generated 3B and initially filed 3B then the taxpayer is compelled to pay additional tax, liability and other dues.

Form GSTR -2A is auto-populated from the Form GSTR-1/5, Form GSTR-6 (ISD), Form GSTR-7 (TDS), and Form GSTR-8 (TCS).It is generated for a recipient when the Form GSTR-1/5, 6, 7 (Tax Deductor) & 8 (Tax Collector) is filed by the supplier taxpayer. The details can be viewed by the recipient and can be updated as and when supplier taxpayer add or alter any details in their respective Form GSTR, for the given tax period. Form GSTR-2A of a tax period is available for view only.

Q. Can I file a GSTR 3B without paying the tax?

As per section 27 (3) of GST Law, GST return will be valid only if the full tax is paid by the registered taxpayer and only the valid return would certify the taxpayer to claim an input tax credit (ITC). In other words, the supplier has to pay the entire self-assessed tax and file his return to be eligible for ITC.GST returns are treated as void if filed without making GST tax payment against such GST returns. Section 28 does not allow ITC on invalid return and defines such taxable person as unqualified for utilizing such credits before clearing his self-assessed tax liability.

Q. Is there any provision for the rectification of errors in GSTR 3B?

However, there is no concept of revised return available in GST, whether for Form GSTR-3B or your regular return which means one can not modify the data after the submission of return in the GST Portal. Yet some errors can be rectified:

The Form GSTR-3B is just an interim return and the actual return for July is to be filed in Form GSTR-1, Form GSTR-2 and Form GSTR-3 by 10 October; 31 October; and by 10 November 2017 (revised dates) respectively. Hence, any correction in GSTR-3B can be duly reported via Form GSTR-1 and Form GSTR-2.

Any alterations regarding outward supplies are to report in Form GSTR-1 when the supplies are incorrectly filled FORM GSTR-3B.

While any corrections regarding inward supplies need to be reported in Form GSTR-2 like when the ITC, tax liability of inward supplies liable for the reverse charge; or any other details of inward supplies are submitted erroneous in the Form GSTR-3B.

Based on the correct details reported in the Form GSTR-1 and Form GSTR-2, the revised tax liability and eligible ITC will be displayed in your e-ledger and these details will get auto-populated in Form GSTR-3 of July 2017.

Because of the absence of the revised return concept the data can only be rectified as long as the GST form is in save status before the submission, but cannot be modified after the final submission of return.

GSTR 3B Form Revisions Under 31st GST Council Meeting

FORM GSTR-1 & FORM GSTR-3B returns are required to be filed before the filing of FORM GSTR-9 & FORM GSTR-9C

The recipient is required to avail invoice issued by the suppliers within the time period of FY 2017-18 in context to ITC till the due date for the purpose of furnishing Form GSTR 3B for the month of March 2019 pertaining to particular conditions

An additional time-window for completion of the migration process has been opened. The due date shall be extended till 31.01.2019 for the taxpayers who had not filed the complete FORM GST REG-26 but have received the Provisional ID (PID) only till 31.12.2017 for furnishing the requisite details to the jurisdictional nodal officer. Also, the due date shall be extended till 31.03.2019 for furnishing FORM GSTR-3B and FORM GSTR-1 for the period July 2017 to February, 2019/quarters July 2017 to December 2018 by such taxpayers

All taxpayers who furnish FORM GSTR-1, FORM GSTR-3B & FORM GSTR-4 for the months/quarters July 2017 to September 2018 after 22.12.2018 but on or before 31.03.2019 will not have to pay any Late Fee

Step by Step Procedure of Filing GSTR 3B Form Online

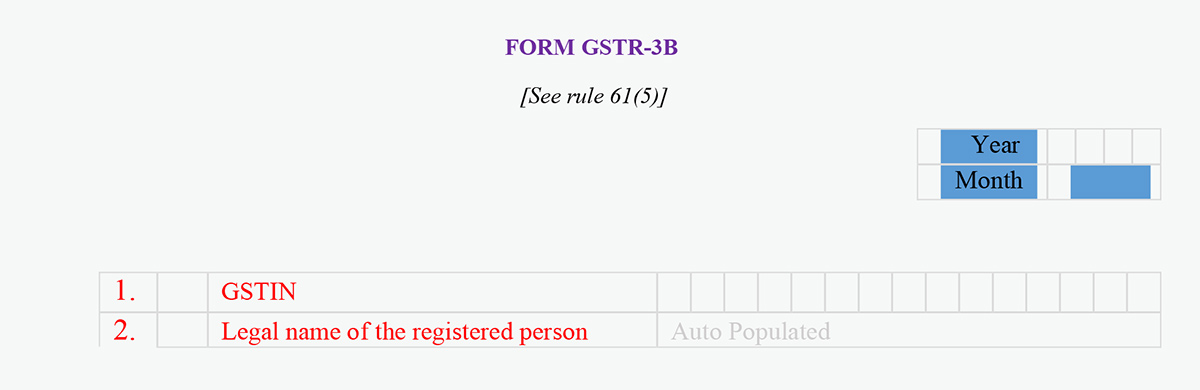

Step:1 First of all the taxpayer will have to enter his GSTIN ID very precisely with no errors. And in the second point, the legal of registered individual.

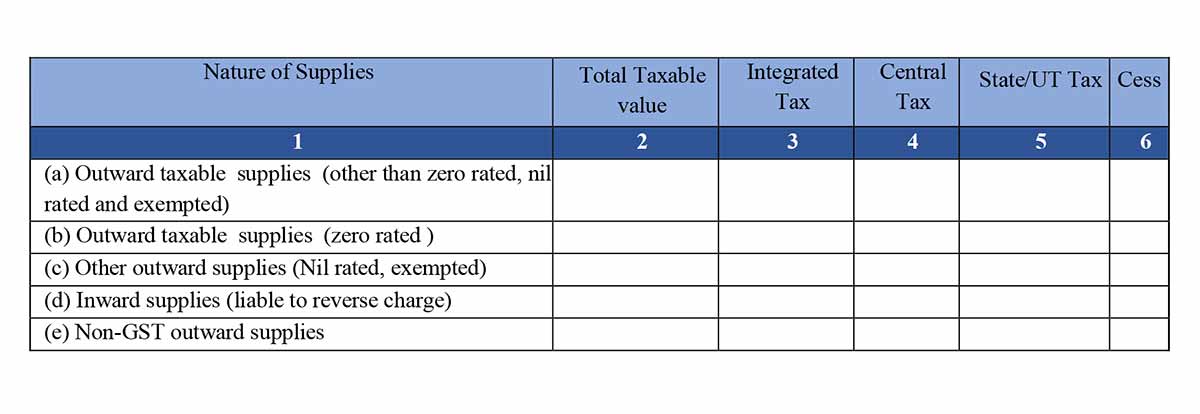

Step 2: Coming to the second box, including Details of Outward Supplies and inward supplies liable to reverse charge:

In the name of supplies column, it is given-

Outward taxable supplies (other than zero-rated, nil rated and exempted) – In this column, fill out all the general and non-taxable items which are sold by the business on a regular basis.

Outward taxable supplies (zero-rated ) – In the column, only zero rate tax items will be included, if any.

Other outward supplies (Nil rated, exempted) – In the column, only exempted tax items will be included, if any.

Inward supplies (liable to reverse charge) – All the supplies of inward supplies must be mentioned here which are liable for the reverse charge.

Non-GST outward supplies – Include all the Non-GST outward supplies which are not covered by the GST tax scheme.

All the details must be filled along with Nature of Supplies, Total Taxable value, Integrated Tax Central Tax, State/UT Tax, and Cess.

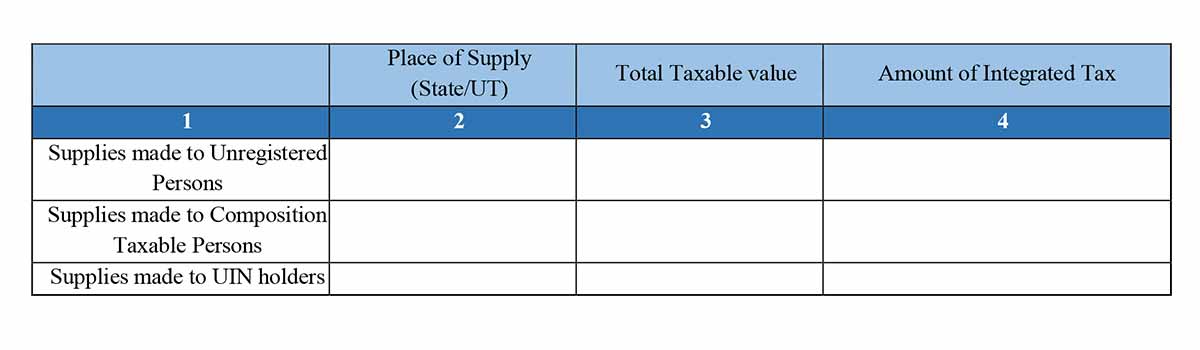

Step 3: Now the box, Of the supplies shown in above, details of inter-State supplies made to unregistered persons, composition taxable persons, and UIN holders.

Supplies made to Unregistered Persons – All the supplies details with the item name and HSN codes in the column which has been done to an unregistered dealer or individual.

Supplies made to Composition Taxable Persons – All the supplies details with the item name and HSN codes in the column which has been done to a composition scheme dealer or individual.

Supplies made to UIN holders – All the supplies details with the item name and HSN codes in the column which has been done to a UIN holder.

All the supplies must be entered with details of Place of Supply (State/UT), Total Taxable value, Amount of Integrated Tax.

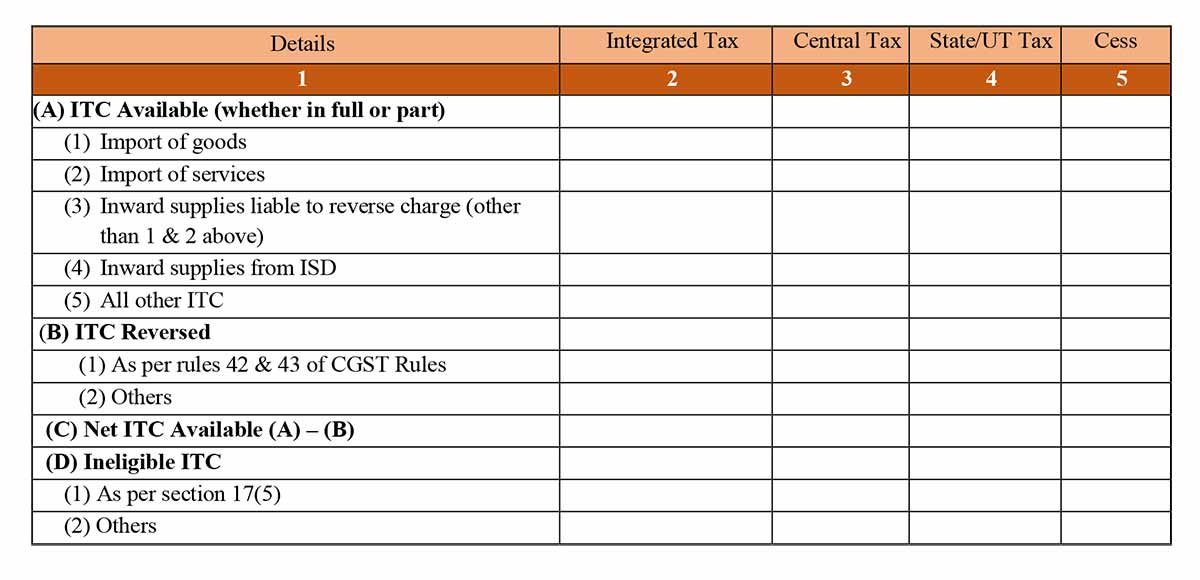

Step 4: Now, the 4th box is of Eligible ITC containing all the input tax credit demand from the taxes paid:

(A) ITC Available (whether in full or part)

Import of goods

Import of services

Inward supplies liable to reverse charge (other than 1 & 2 above)

Inward supplies from ISD

All other ITC

(B) ITC Reversed

As per rules 42 & 43 of CGST Rules

Others

(C) Net ITC Available (A) – (B)

been(D) Ineligible ITC

As per section 17(5)

Others

The required details must be filled up with Details of individual taxes to be paid accordingly, Integrated Tax, Central Tax and State/UT Tax Cess.

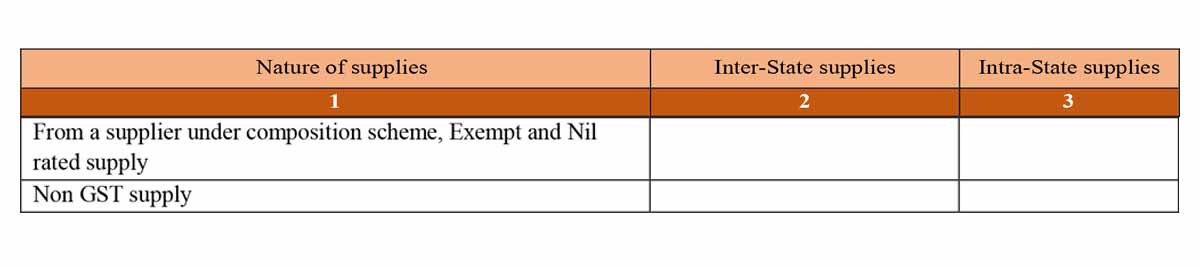

Step 5: Now coming to box 5, it includes Values of exempt, nil-rated and non-GST inward supplies:

From a supplier under composition scheme, Exempt and Nil rated supply – Include all the purchases made by unregistered dealers and composition dealers in the list.

Non-GST supply – Include all the non-GST applicable items and products of a similar category.

The taxpayer has to include all the relevant details of Nature of supplies, Inter-State supplies, Intra-State supplies, and its calculations.

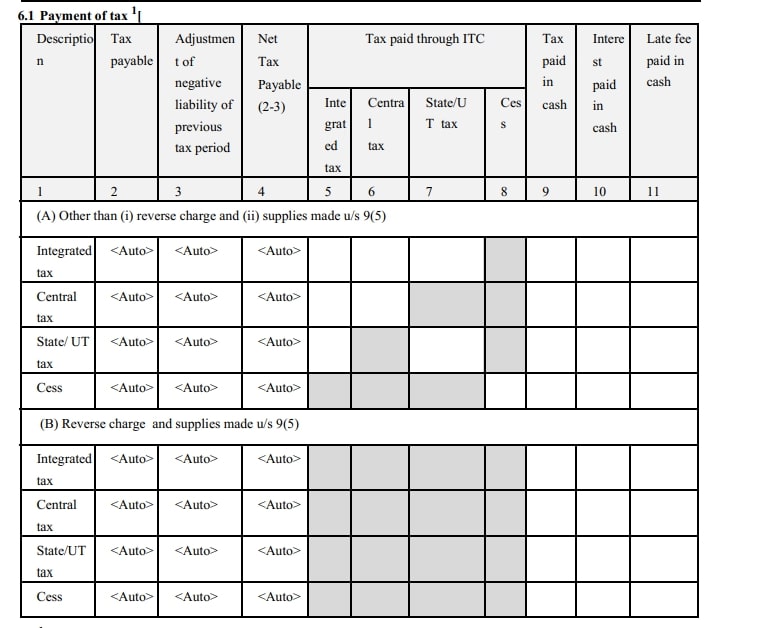

Step 6: Now comes the important box for the payment of taxes, which included a number of significant data which has to be filled up with accurate details:

Integrated Tax

Central Tax

State/UT Tax Cess

The details must be Tax payable, Tax paid- (TDS./TCS) Tax/Cess paid in cash, Interest Rate Paid through ITC – (Integrated Tax Central Tax State/UT Tax Cess)

Note: Columns which are filled in black colour must not be filled up.

Step 7: In the next box, it comes the details of TDS/TCS Credit

A proper format in which it has been mentioned all the TDS and TCS deducted for all the tax scenario including Integrated Tax, Central Tax, State/UT Tax.

Overall the Government has chosen to implement GSTR 3B form in the starting phase of GST return filing for the easy and convenient taxpaying experience for the dealers.

The panel headed by CBDT member Akhilesh Ranjan proposed amendments in the Income Tax Act on Monday. This was the act of relief for the taxpayers. Reforms included a 25% tax rate for domestic as well as foreign companies and reforms in other income tax slabs to benefit the middle class and upper-middle-class Indian residents.

Motivation to startup companies, the proposal also recommended incentives for startups and the all-new curriculum for settling disputes between taxpayers and administration through negotiations, extracted from the panel reports delivered to Nirmala Sitharaman. The government will disperse reports of the council in the public domain for further discussion after personally investigating the recommendations.

Tax Algorithms for Corporate Sector

Proposed by the panel, tax relief will apply to both, in-house, as well as foreign companies that are currently working within the premises without any subsidiary and are liable for 40% tax. Foreign firms are charged with higher tax as compared to the domestic firms but are deprived of “dividend distribution tax” which is needful for a domestic company.

Read Also: How to File a Complaint Against Income Tax Officer?

Presently, domestic small scale companies with certain threshold limits are liable for a 25% tax rate while giant businesses pay 30% income tax including surcharge and cess to the nation. Certain tax relief measures could prove to be a boon for corporate sectors which are sliding with the economic slump. The introduction of new direct tax laws will lead to new taxation concepts and plans to reduce corporate disputes.

To interest foreign companies, the proposal has ‘branch profit tax’ for businesses who dispatch the earnings to their centres overseas. However, the effects of branch profit tax and reduced corporate tax remain unseen. US government in 2017 executed “The Tax Cuts” and “Jobs Act” with the intention to encourage overseas extensions of American companies to dispatch their profits to their origin firms.

The panel proposed for plain assessment proceedings along with the opportunity for the public to ask for clarifications on tax issues from CBDT.

Significant reforms are awaited by the government on corporate tax laws. Immunity schemes such as Sabka Vishwas (legacy dispute resolution) Scheme earlier introduced to restrict litigations under indirect tax enactments is a good amendment to be included in the direct tax design as well.

The proposal is kept on the desk on Finance Minister Nirmala Sitharaman with the vision of bringing an absolute taxation structure for reviving personal and corporate income tax. The reforms are favourable to enhancements in business and reducing the compliance load as well as tax disputes.

The nation is heading towards the path of tax reductions in favour of the businesses in the country to boost the sector with immense production and sales. The current economic slowdown has urged the jurisdiction to call for reforms in the interest of the blooming businesses.

The businessman from the city of Jammu asked for the due date deadline extension for the income tax filing as well as for the goods and services tax return filing.

The reason behind the extension given by the Chamber of Traders Federation(CTF) was the suspension of internet services across the state which made the return filing delayed.

The Chamber of Traders Federation (CTF) sent a letter to the Union Finance Minister Nirmala Sitharaman in which it said, We demand an extension of dates for filing of income tax and GST returns in view of the peculiar ongoing situation in Jammu and Kashmir following the abrogation of Article 370.”

The association also added that there is some impact after the abrogation of 370 on both income tax and goods and services return, which needs to be further analyzed and studied.

There was a lot of hue and cry when the article 370 was abolished recently but the association praised the trader’s community to perfectly balancing the situations.

It also added, “We hope that the government would provide necessary relief to augment trade once the situation becomes congenial.” In the meantime, the state government is preparing itself as per the news laws.

Only 20% of Visakhapatnam Traders have filed central goods and services tax (CGST) returns till the date and 80% of them need to urgently file the returns before the due date of 31st August 2019.

The due dates for filing GST returns have been extended many times due to the complexities and cumbersome process involved in it and finally, 31st August 2019 was concluded to be the deadline which will stand its ground.

The eyelids of CGST officials have turned towards the total GSTR filings in the largest city and the financial capital of Andhra Pradesh i.e. Visakhapatnam. And the conclusion came out to be quite awful when it was encountered that only 20% of traders have filed the GST returns and 80% are yet left to file when only a fortnight is remaining to touch the time limit.

The target of Rs 58,222 crore which was fixed for Andhra Pradesh for 2018-19 is going skimpy with the total collection of just Rs 16,037 till July 2019.

As the taxpayers were delaying the filing process and involving in the process of illegitimately claiming bogus ITC & not passing on the benefits to the consumers, the stringent rules for curbing such unlawful practices were already framed.

Now the heavy penalty is imposable on late filing of GSTRs and illegitimate acts such as ITC scams, use of ITC as working capital & holding GST amassed from consumers may get the defaulters behind bars.

“All taxpayers should file their GST returns for 2017-18 by August 31, else they would face severe consequences, including a hefty penalty,” said chief commissioner of Customs and CGST, Visakhapatnam Zone, Naresh Penumaka.

He also added, “Traders should also issue a bill collecting GST as per the reduction affected by the GST Council from time to time”.

The chief commissioner turned down that the burdensome & baffling filing process is the reason behind deficiency and delay in GSTRs return filing. He called attention to the fact that at the national level, the compliance rate is 90% whereas, at the state level, it is just 70%. According to him, some of the traders deliberately delay in making payment.

The commissioner also notified that the due dates for GSTR filing will not be postponed further so the traders who are yet left to file the returns, must approach the closest central excise official for filing GSTRs ASAP.

It is high time when the taxpayers should start approaching the close at hand office for Central Exercise because this time the due date of 31st August is inevitable, so if the taxpayers get a delay in filing returns before that, they will end up paying heavy penalties for late GSTRs filings. The rules this time are quite strict so the taxpayers should take a simple path & comply with the government rules & regulations if they do not want to be imprisoned.

Taxpayers can now file their annual GST Returns 9, 9A and 9C with advanced GST filing software Gen GST. The software is available in both desktop and web/online versions. It offers unlimited client return e-filing with features like auto error detection, error summary, e-way bill generation, invoicing, import data, and more. Download the free demo of Gen GST Software now!

Central Board of Direct Taxes (CBDT) is marching forward towards “Digital India” and it has framed its mind to utterly knock off the manual processing with the taxpayers. The orders of the same have been given to income tax officials. As per this major policy conclusion, the tax officials will be able to have only digital communication with taxpayers which implies a big “NO” for paper-based exchange of information.

The order will become operative from October 2019, after which any information associated with assessment, investigation, penalty, appeals or rectification, will be allowed to be transmitted digitally only and the communication which will not comply with the guidelines defined by CBDT shall be treated invalid.

Read Also: All About Digital Signature & How to Use in ITR Filing

CBDT chairman Sudhir Chandra expressed appreciation for this step saying that, “It’s a good step that the department is owning up the responsibility,”.

“All the assessment, appeals, orders, statutory or otherwise, exemptions, inquiry, investigation, verification of information, penalty, prosecution, rectification, approval, etc issued on or after October 1, 2019, shall carry a computer generated Document Identification Number (DIN) duly quoted in the body of such communication,” said the CBDT of India.

All these documents which are related to appeals, investigation, penalty etc will have a unique Document Identification Number (DIN) i.e. a computer-generated identification number (DIN) embedded in it. According to CBDT, this DIN will upkeep an appropriate paper-based trail.

DIN guarantees to the taxpayers that the documents have been issued by the Income Tax Department and a taxpayer can easily & promptly ignore any such document which does not have any DIN.

“Now you can be sure that a particular communication has indeed been issued by the department. If it doesn’t carry the unique Document Identification Number (DIN) then you can simply ignore it, Sudhir Chandra told Financial Express Online”.

CBDT told that the Income Tax department had already started communicating electronically on the Income Tax Business Application (ITBA) platform to nail down the transparency. But the board observed that some of the information is still transmitted in a paper-based manner to the taxpayers which lead to improper maintenance of audit trail. So, the Board decided to exercise this stringent rule that bans manual communication completely and will invalidate all such communications post-September, this year.

Recommended: Incomplete ITR Details May Face up to 200% Penalty, See How!

“Any communication which is not in conformity with the prescribed guidelines shall be treated as invalid and shall be deemed to have never been issued,” CBDT clarified in a statement. However, now also in some exceptional cases, the way of communication will still be manual and these extraordinary cases have been differentiated and stated by the CBDT.

Such cases would need to be approved by the respected chief commissioner or director general of income tax and the consent should be in written form. In addition to this, the deadlines and course of action in this regard have also been specified by the CBDT. These manual conversations will be regulated and suggested to the Principal Director General of Income-tax.

The motive of the tax government is to make your ITR filing convenient and less time-consuming. In case if you have filed your Income Tax return completing all the formalities still you are bothered by the tax officers regarding the compliance, you can file a report stating your issue or instead file an online complaint against the officer bothering you.

Grievance Redressal in Principal CCIT Region

Especially for your complaints, Grievance Redressal in Principal CCIT Region or Unified Grievance Handling System is on duty to online launch a report with the help of e-redress. You can file a complaint in case if there is any trace of harassment, misbehave or delay in forwarding your file from the officer’s side.

How to File a Complaint Against IT Officer?

Let’s have a look at quick steps to file an online complaint against any inconvenience from the department or from the tax officers:

Visit www.incometaxindia.gov.in and click on ‘Contact Us’ visible on the dashboard

Inside you will find guidelines related to various tax issues faced by the filer

Select Grievance Redressal in Principal CCIT Region option visible on-screen → Select from the list, the name of your state

After selecting the state, you will land on the list of ‘zones’ → Select your Zone from the list

You will now come across the list of all the Income Tax officers operating in your area with the details of their phone numbers and email id. You can now compliant

An assessee is responsible to file an Income Tax Return (ITR). Different ITRs have to be filed by different kinds of taxpayers before the due dates. ITR-7 is one of those ITR which is filed by the individuals & companies which fall under section 139(4A) or 139 (4B) or 139 (4C) or 139 4(D).

There are different sections which governs the compliances to adhere towhile filing ITR-7. The sections are as follows:

Section 11

Section 10 (23C)(iv)/10(2 3C)(v)/10(23C) (vi)/10(23C)(vi a)

Here, we will briefly discuss the compliance requirements to file ITR-7 as per these sections. Compliance requirements Under Section 11 and Section 10 (23C)(iv)/10(2 3C)(v)/10(23C) (vi)/10(23C)(vi a) ask for the registration/ approval under section 12/12AA and Section 10 (23C)(iv)/10(2 3C)(v)/10(23C) (vi)/10(23C)(vi a), respectively along with details furnishment under “Details of registration under the Income Tax Act” in Part A General.

Section 139(4A) and Section 139(4C) is the Return filing section for the former and the latter one, respectively. Schedule VC and AI are for offering the contribution and income under section 11 while under section 10 (23C)(iv)/10(2 3C)(v)/10(23C) (vi)/10(23C)(vi a), the contribution and income are offered in schedule VC and AI.

Other compliances under Section 11 And Section 10 (23C)(iv)/10(2 3C)(v)/10(23C) (vi)/10(23C)(vi a) are as follows:

Amount spent for the charitable purpose has to fill schedule ER, EC.

Assessee claiming exemption via deemed application has to furnish details in point 4 of schedule part BTI and Form 9A before the deadlines.

Assessee claiming exemption via Accumulation has to furnish the details in Point 4 of schedule Part BTI and Form 10 before the deadlines.

Other taxable income has to be offered in schedule HP, BP, CG and OS.

Non-adherence to Section 11 & 12 or unqualified to claim exemption has to fill Sl.No. 5 of schedule Part-BTI.

Form 10B and Form 10BB, respectively under section 11 and the other, has to be furnished for Audit report along with the return of income before the due date.

All other sections comply the Registration/Approval under any law which is applicable besides the Income Tax Act. Return filing section is 139(4C) under Section 10(23C) (iiiab)/(iiiac), Section 10(23C) (iiiad)/(iiiae), Section 10(21), 10(22B), 10(23AAA), 10(23B), 10(23D), 10(23DA), 10(23EC), 10(23ED), 10(23EE), 10(29A), 10(46), 10(47), Section 10(23AAA) and Section 10(23A), 10(24), whereas under section Section 13A and Section 13B, 139(4B) is the Return filing section.

Other Compliance requirements Under Section 10(23C) (iiiab)/(iiiac) includes offering the contribution or income in schedule VC and IE-3. Exemptions claimed u/s 10(23C) and u/s 10(23C) (iiiac) should be filed in point 9a of schedule part BTI and 9b of schedule part BTI, respectively. Other taxable income has to be offered in schedule HP, BP, CG and OS, while the gross receipts and Grants received from Government, have to be furnished in Schedule IE-3 in addition to Schedule VC for the grants received from the government.

139(4D) is the return filing section under Section 10(21) read with section 35(1) clause ii and iii. Under Section 10(20), 10(23AA), 10(23AAB), 10(23BB), 10(23BBA), 10(23BBC), 10(23BBE), 10(23BBG), 10(23BBH), 10(23C)(i), 10(23C)(ii), 10(23C)(iii), 10(23C)(iiia), 10(23C)(iiiaa), 10(23C)(iiiaaa), 10(25)(i), 10(25)(ii), 10(25)(iii), 10(25)(iv), 10(25)(v), 10(25A), 10(26AAB), 10(26B), 10(26BB), 10(26BBB), 10(44)) where income is exempt unconditionally, the return filing sections is “Others”. For all these sections, other taxable income has to be offered in schedule HP, BP, CG and OS and the contribution or income is offered in schedule VC and IE-1.

For a complete version of the checklist to avoid mistakes in filing ITR 7 for AY 2019-20, here:

Also, there are some changes in the utilities of ITR 6 and ITR 7 to avoid any bugs in due course of filing the schedule of TDS and FSI. Note that the changes do not impact any schema of XML. The taxpayer must download the latest utility of excel before proceeding.