On 24th July, the CBDT will conduct a taxpayer e-assistance campaign across the country to acknowledge the 159th Income Tax Day. while the Finance Minister Nirmala Sitharaman will be the chief guest of the event, as mentioned from the Officials. The Central Board of Direct Taxes (CBDT) is authorized body behind the launch of the campaign and all the regional offices of the Income Tax Department will be benefited with this movement, they further added.

The taxman that is authorized to maintain camps across the country, will help taxpayers in e-filing of their tax returns and this “hand-holding” program will make taxpayers aware with recently made changes to the forms, laws and utilities (software) of the direct taxes system, PTI reported as per a policy plan.

The CBDT, responsible to craft policy for the department, planned for the campaign post getting representations from taxpayer and stakeholders, likewise chartered accountants and bank, that they require more help in terms of filing returns electronically and performing several other IT related duties under the tax laws, they said.

On 24th July, all the regional offices of the Income Tax Department will commemorate the day by honouring the taxpayers who file their taxes diligently. As the sources revealed, the main event will be organized in Delhi and the Finance Minister Nirmala Sitharaman along with the Minister of State for Finance Anurag Thakur will mark their presence as the chief guest.

Not even this, it is being expected that the Union Minister will deliver a speech and the top officials of the department like Indian Revenue Service (IRS) and other officials are likely to be rewarded for their excellent performance in the service.

The event which is going to be held at Ambedkar International Centre on Janpath Road from 10 AM, mandates all officers from the rank of Assistant Commissioner and above posted in Delhi to attend the event, a source said. In the year 1860, the income tax was first levied on July 24, that’s why this day is celebrated as the ‘Income Tax Day’ every year.

In a recent announcement, the Finance Ministry has said that no GST invoice will be required for the goods that were taken abroad for exhibitions or other kinds of export promotion events and are brought back to India within six months.

The ministry further said that most of the exporters were having problems due to a lack of clarity about the GST procedure for the goods that are exported from India.

The applicability of GST during such goods sale was a matter of concern for most of the exporters.

Issuing clarification on GST applicability for exported goods, the ministry said that goods that were taken outside India on a consignment basis for the exhibition purpose do not qualify as supply under GST, but such products must be carried outside with a “delivery challan.”

The ministry said, “Since taking such goods out of India is not a supply, it necessarily follows that it is also not a zero-rated supply. Therefore, execution of a bond or LUT (Letter of Undertaking), as required under section 16 of the IGST Act, is not required.”

It was also mentioned in the clarification that goods that were exported from India for the exhibition purpose must be sold or brought back of India with a period of six months, starting from the date of removal or dispatch.

Although if the exported goods for exhibition purpose are not sold or brought back of India within six months than the tax authorities would consider as a supply that has taken place.

In this regard, the ministry stated, “In this case, the sender shall issue a tax invoice on the date of expiry of six months from the date of removal, in respect of the quantity of goods which have neither been sold nor brought back. The benefit of zero-rating, including refund, shall not be available in respect of such supplies.”

If the goods exported are sold abroad, full or partially, within six months, then the authorities would mark it as a valid supply under GST, in regard to the quantity so sold on the date of sale.

The sender of goods in such cases will also be required to issue a tax invoice against the sold goods. The supply would be counted as a zero-rated supply during the invoice generation.

Although, the refund for such supplies would be available only as a refund of unutilised Input Tax Credit (ITC), rather than a refund of Integrated GST.

“No tax invoice is required to be issued in respect of goods which are brought back to India within the period of six months,” the ministry mentioned.

At the point of origin of income, the taxpayers in India have to pay TDS (Tax Deducted at Source) as per the Income Tax Act, 1961. An amount from the total earnings received by a deductee or receiver is generally withheld by the deductor (person, institution, or organization). This deducted amount is equal to the tax amount, which needs to be credited to the government account within the prescribed time limit.

TDS Applicability in Multiple Forms

Most of the people in India believe that TDS is applicable to salaried individuals, but that’s completely wrong. There are multiple scenarios where TDS is applied, such as:

Income earned from the internet against securities and debentures

Interest Income received from various sources other than securities and debentures

Dividend Income

Money received from EPF (if it is availed before the prescribed withdrawal limit or if the amount withdrawn exceeds the specified limit)

Money sent to freelancers, contractors or subcontractors

Winnings from the game shows, lotteries, crossword puzzles or any other game-related winning Insurance or brokerage commission earnings

Earnings from the transfer of Movable property

Profits received from technical or professional services to clients

Income earned against royalty, etc.

Why is TDS at First Place Exists?

It is a well-known fact to everyone that earnings or income received by people in India is subject to tax at the end of the financial year. It is challenging for the central government to maintain cash reserves or national revenue if income earned by citizens are taxed only at the end of the year, Hence, to avoid such a situation, the concept of TDS has been introduced. The introduction of the TDS system helps the Indian government to:

Prevent the evasion of Tax: TDS mechanism is a masterstroke by the government to receive a portion of the total payable tax from the income at its source point directly with zero delays. This way, the government ensures that people do not hide their actual income and also minimize tax defaults.

Steady Revenue Source: the imposition of TDS on taxpayers also provide a stable revenue source to the government throughout the fiscal year.

SimplifyTax Return Filing Process: As the tax gets deducted automatically via TDS at source, the taxpayers won’t have to pay any other taxes during return filing, if they do not have any other source of income.

Maintain Timely Collection of Tax: The government ensures a timely collection of taxes by imposing the TDS system.

Provide Convenience of the Taxpayers: Individuals can plan their finances very well as the total tax payment gets spread throughout the year for them via TDS. Lump-sum payment of TDS in a single month is a bit difficult for salaried persons as it struck their financial obligations hard.

TAN stands for Tax Deduction and Collection Number; It is a ten-digit alphanumeric number that is issued to the registered organizations or individuals who are obliged to deduct or collect tax at source against payments made by them.

It is mandatory for all the individuals or organizations (bind to deduct tax) to mention the required TAN details to the Income Tax Department in all practices that are relevant to TDS (e.g. TDS returns, issuance of Form 16, TDS payments, etc.), as per the Section 203A of the Income Tax Act 1961. Those who fail to fulfil the above duties are obliged to pay a penalty of INR 10,000.

All the authorized banks in India don’t accept TDS deposits or payments when the TAN details are not mentioned by the depositor.

Point to Note:

In many instances, TAN and PAN are assumed to be the same documents by many people, thinking they can be used interchangeably, which is entirely a false assumption.

One must know that the organizations, individuals or any other entity who is responsible for tax deduction at source must have a TAN, even if they have a PAN. Immovable property buying/selling activity is the only valid exception in this case, where the buyer or deductor is not required to present TAN and can use PAN for TDS payment.

TAN Application Procedure

TAN application procedure is straightforward and can be done online by submitting the Form 49B.

TDS Deduction

As per Section 192 of the Income Tax Act, the deductor must collect TDS at the time of actual payment of salary to employee accounts rather than accrual time of salary.

If any employee gets salary/wages in advance or arrears on salary are paid in advance, then TDS must be collected at that time too.

Apart from this, for all other payments TDS must be deducted at the time of Payment or credit or income (whatever falls first).

TDS Online Payment

Online TDS payment facility is driven by the philosophy of “Anytime, Anywhere.”

Thanks to all the online TDS filing, the TDS administration has become easy and transparent for both taxpayers and government, helping minimize tax scams.

TDS website is a common platform for everyone, including deductors, taxpayers, and assessment officers to obtain or get hands-on the same TDS data.

Increasing Digitization is becoming a cornerstone of a speedy, accurate, and stabler TDS system in the country.

How to Make TDS Payment Online?

W.e.f. January 1st, 2014, the government has made it compulsory for all the public & private sector deductors, and other assesses, who are bound to audit under Section 44AB to use the electronic transfer method of making TDS Payment online. For such purpose, such personnel must have an active net-banking facility with an authorized bank; the eligible banks are listed on the NSDL-TIN website.

Here is a step by step procedure for online TDS payment:

The taxpayers, first, should visit the Income Tax Department E-Payment website. Here is the link for the same: https://onlineservices.tin.egov-nsdl.com/etaxnew/tdsnontds.jsp

Deductee falling in the category other than company must select (0021), Non-company deductee option. Others must choose (0020) Company Deductee.

Enter TAN details. Entered details must be used for online verification of TAN.

If the entered TAN details are not present in the income tax department database, then the user won’t be allowed to proceed further with the online Payment.

After submission of TAN, enter the relevant assessment year (AY), which is the immediately following year for the given financial year whose income is being evaluated. For instance, AY for the income earned between April 1st, 2015 to March 31st, 2016 would be AY 2016-17.

Afterwards, enter challan details. The details like name, address, email I.D., and contact details of the TAN holder must also be submitted.

Also, you will need to select the bank through which the TDS will be deposited.

Select the payment type

In case of a normal payment, click on the (200) TDS/TCS Payable by Taxpayer, or if it is a payment against the request raised by the income tax department (e.g., Payment of interest or late fees as per the section 234E), then you must click on the (400) TDS/TCS Regular Assessment (Raised by I.T. Department)

Select the payment nature type (e.g. Payment of insurance commissions, fees for professional services or rent), etc.

Confirm all the entered data in the challan by entering it properly and as per the best of your knowledge.

Post confirmation of data, you will be redirected on your bank’s net banking website page.

You must log in with valid user I.D. and password for processing of Payment.

Once the payment is successful, the system will display a challan counterfoil.

This particular challan contains CIN (Challan Identification Number) along with other details like bank name, customer name, Bank Branch Code, date of challan, etc.

All the entered challan details are transmitted by your collecting bank to the “Tax Information Network” (TIN) by taking the help of the Online Tax Accounting System (OLTAS).

Challan status can also be verified by you through ‘Challan Status Inquiry” on the NSDL – TIN website after seven days of making Payment via CIN.

Why TDS Certificate Required?

Once the TDS has been deposited with the income tax department, the deductor must issue a TDS certificate to the deductee on behalf of whom the tax payment has been made. The TDS return certificate required or Form 16 / Form 16A is generally issued on an annual or quarterly basis.

Advantages of Online TDS Payment

The online TDS payment facility is available 24X7 throughout the year for taxpayers.

The deductor can make TDS payment anytime, anywhere as per the convenience.

Immediate acknowledgement is received by the taxpayer in case of an online TDS payment.

The challan copies can be downloaded instantly and can be saved in the computer for future reference.

Minimal Paperwork with zero hassle.

As Paperwork is completely zero, it leads to better environmental safety.

Time Limit of TDS Payment and Schedule

The last date for making Payment of TDS collected by the deductor is the 7th of the subsequent month. For instance, for the month of July, the deductor is required to make the TDS payment on or before August 7th.

The only exception is the month of March (as it is the last month of a particular financial year) where the TDS deductor is allowed to maker TDS payment on or before April 30th for the given year.

All types of deductors (e.g., government and non-government assessee, etc.), who submit ta with Challan (treasury challan) are instructed by the government to follow this particular TDS timeline.

In the case of government deductors making TDS Payment without challan, the due date for Payment of TDS will be the same day when the tax amount has been deducted.

In some cases, the quarterly Payment of TDS might be allowed by the Assessing Officer (AO) by taking the prior approval of the Joint Commissioner. If that happens, then the last date for TDS paymentwould be the 7th of the subsequent month following the given quarter and April 30th for the last quarter of a particular financial year.

E-File TDS Returns

All the corporate deductors are mandated to furnish their TDS returns in electronic format (w,e.f. June 1st, 2003) (e-TDS returns).

W.e.f. In the fiscal year 2004-05, the government deductors have also been enforced to furnish e-TDS returns.

Apart from the government and corporate deductors, other deductors have the option to furnish TDS return in either electronic or physical format.

How TDS Return File Online?

The TDS returns need to be filed, on a quarterly basis and the due date for the same is 31st of the month after the end of the concerned quarter.

TDS return can be filed by a registered taxpayer individual, organization or institution, who operates as a deductee. Quarterly TDS returns are filed by such entities. According to section 201 (A), the interest incurred on delay in Payment of TDS should be furnished by the taxpayers before filing their TDS return.

Some Important Points About TDS Return Forms:

Form 24Q: This form needs to be filed against deductions made from salaries

Form 26Q: This form must be filed for deductions made from payments apart from salary.

Form 27Q: This is a quarterly TDS return form that needs to be filled out by deductor on behalf of all the deductions made against NRIs

Form 27EQ: This serves as TCS quarterly return that needs to be filed by the deductor

Form 27A: This form must be attached along with quarterly statements by duly signing it.

Key Points to Remember Concerning TDS Returns

NSDL e-Governance Infrastructure Limited, (NSDL e-Gov), operates as an e-TDS intermediary between the CBDT and the TDS deductors.

TIN Facilitation Centres (TIN-FCs) has been established across the country by NSDL e-Governance for assisting TDS deductors in the TDS return filing process.

Both the online and offline formats of file TDS return quarterly are the same.

The e-TDS statements should be structured as per the file format (clean ASCII File), which is similar to the details that are provided by the income tax department.

For easy preparation of TDS returns, the government also offers free downloadable software (Return Preparation Utility – RPU) that has been devised by NSDL.

The TDS deductors can also use third-party TDS tools for preparing and furnishing e-TDS.

All the approved vendor’s details can be seen by taxpayers on the NSDL-TIN website (www.tin-nsdl.com).

Penalties & Consequences for Missing the TDS Payment of Due Dates Penalty

Late In TDS Payment

It is mandatory for deductors to deduct the TDS on the 30th of each month, except for the month of February where it should be deducted on the last day of the month.

In case, TDS is not deducted on the due date (whether in whole or part), the deductor would have to pay interest at a rate of 1% p.m or part thereof, starting from the date of actual deduction.

For instance, if the due date of TDS payment was July 30th, but it was actually deducted on August 5th, in such a scenario, the TDS deductor would be bound to pay interest for two months, i.e., July and August.

Delay in TDS Payment

As per the Section 201 (1A) of the income tax act, if the TDS deductor fails to furnish the deducted TDS payment to the credit of the concerned tax authorities within the given time frame, whether in whole or in part, he/she would be liable to pay interest at a rate of 5% per month or part thereof, starting from the date when TDS was actually deducted till the date TDS was furnished to the credit of the government.

For ease of calculation, the entire calendar month is considered during interest calculation (e.g. a portion of a month will be considered as full while making TDS interest calculation).

This simply means that even a delay of one day can cause interest in two months for TDS deductors.

For instance, suppose for the TDS deducted in the month of July, the Payment has been delayed by a single day and deposited to the credit of government on August 8th. In such a case, the deductor would be forced to pay interest for two months, i,e, total 3% interest.

Apart from interest applicable on TDS late deduction and late Payment, there are some additional provisions for penalty and prosecution too:

Penalty as per Section 221

The defaulter, i.e., TDS deductor, is liable to pay the penalty, In case he fails to deduct tax, without any proper reason as judged by the Assessing Officer.

In any case, the amount of penalty should not exceed the amount of tax in arrears.

Penalty as per the Section 271C

A penalty that equals the tax amount can be imposed, if deductor fails to deduct required TDS amount

Although, the authority to levy such penalty lies within the hand of a Joint Commissioner of Income Tax dept only.

Prosecution Proceedings According to Section 276 B

The deductor is liable to receive rigorous imprisonment for 3 months to 7 years, and fine, in case, if he/she has fails to deposit the deducted TDS amount to the credit of concerned tax authorities without a valid reason.

Late TDS Return Filing

In case, an assessee or deductor fails to furnish TDS return within the given time period, he/she is liable to a penalty of INR 200 per day, until TDS return has been furnished, as per the Section 234E of the income tax act.

The total penalty amount should not surpass the total amount of TDS collected.

This penalty is also imposed, in case of purchase of immovable property or furnishing Form 26 Q.B.

Submission of incorrect data such as TAN, Challan Number, TDS Amount, etc. or delay in TDS return filing for more than a year, starting from the due date can attract a minimum penalty of INR 10,000 to 1,00,000.

Procedure to Check/Verify TDS Payment Status

TDS payment status can be checked online by TDS deductee by visiting the online portal of Centralized Processing Cell.

Here are the detailed steps for the same:

Go to the official TDS CPC website, click on the link https://www.tdscpc.gov.in/app/tapn/tdstcscredit.xhtml

Enter the given captcha code and press the submit button.

Mention details like PAN, fiscal Year, TDS Quarter, TAN, and Return type. Now, click on the “Go” button.

TDS credit details of the taxpayer are showcased on screen.

What is TDS Return Due Date?

The detailed information about TDS payment due dates and other timelines for filing and depositing TDS/TCS return is mentioned below in the table. You can also check the late payment and interest charges on late deduction and deposit of TDS.

GST composition scheme was implemented under the respective State VAT Laws with conditions applied on eligibility for the scheme accordingly. GST composition scheme assures greater compliance without the requirement of maintaining records. This system is missing in Service Tax laws.

32nd Council GST Meeting for Composition Traders

The annual turnover limit increased by GST council to 1.50 Crores, effectively from 1 April 2019

Annual filing of GSTR 4 return instead of quarterly. Also, tax paid to be deposited on a quarterly basis.

6 per cent GST rate applicable to the Composition scheme for service providers and turnover up to 50 lakh per annum

Note:

Above amendments shall be applied after the official government notification.

Every taxation system has some prescribed rules or regulations which must be followed by individuals, taxpayer or business owners. Maintaining records properly, submission or filing returns timely, simplified generation and periodic payment of taxes are some of the essential elements of the taxation system for corporate taxpayers. However, business enterprises and owners are facing difficulties to cooperate with such responsibilities of law. It happens just because of lack of knowledge and the majority of people is not aware of the taxation system.

In 28th GST council meeting, the FM has decided to extend the threshold limit of composition scheme taxpayers from 1 crore to 1.5 crores. Also, included the 10% provision of normal taxpayer annual turnover within the composition scheme if in case the given 10 percent is provided as the service.

Key Features of GST Composition Scheme

Eligibility: – Everyone is not eligible to register under the GST composition scheme. Taxpayers or people whose annual turnover up to INR 1.5 crore in a financial year. Turnover for special category States, except Jammu & Kashmir and Uttarakhand, the limit is now increased to Rs 75 Lacs. While the turnover threshold for Jammu & Kashmir and Uttarakhand will be Rs 1 crore must register under the GST composition scheme. The small traders should fill up GST CMP-01 form to accept the scheme.

Special Eligibility:- The GST council has included normal taxpayers within the composition scheme in case 10% of annual turnover is provided as a service.

Quarterly Filing Returns: – Instead of submitting returns 3 – 4 times in a month, taxable person or registered taxpayers will be required to submit or filing tax returns only one time in every quarter under the GST composition scheme.

Intra- State Supplies: – Local suppliers, who supply goods or services within a state can take advantage of the GST composition scheme. Interstate suppliers will come under the regular GST laws.

Bill of supply, not tax invoice: – Registered taxpayers under the GST composition scheme will be required to show the bill of supply instead of tax invoice to the tax authorities. A person paying taxes under the composition scheme can issue a bill of supply instead of the invoice. Exemptions up to 5 lakhs for services under composition scheme are also available.

Not Eligible for Input Tax Credit: – According to section 16, goods and services on which composition tax has already been paid (under section 8) do not apply for Input Tax Credit.

Tax Rate: – Manufacturers – 1% ( .5% central and .5% state), Restaurants services – 5% ( 2.5% central and 2.5 state ), Composition levy eligible – 1% ( 0.5% central and 0.5% state )

GST Only on Taxable supplies: – Earlier it was a provision to pay composition GST even on the exempted goods but now after 1st January 2018, the GST will be only payable on the taxable goods.

Penalty: – If the taxable person is not eligible for the GST composition scheme, then the tax authorities can charge a penalty equal to the amount of tax on such person along with his tax liability. Be careful when availing this scheme and paying taxes. The penalty will be imposed according to the provision of section 73 or 74 if an individual represents incorrect data under the composition scheme.

Voluntary Registrations: – For availing the benefits of this scheme, taxpayers need to make voluntary registration. If in case, the taxpayer annual income turnover exceeds 75 lakh then he will be transferred to the regular scheme. Taxpayers who are already a part of VAT composition need to voluntarily register under this scheme. The scheme can be availed by both migrated and new taxpayers is now extended up to 31st March 2018.

Note: The eligibility and service supply exemption is under review after the 23rd GST Council meeting

Registration Procedure Under the Composition Scheme

Registered or existing taxpayers not under the Composition Scheme may prefer to opt for it (subject to being qualified), only from the beginning of the next financial year. Tax returns to be filed on as or before 31 March of the previous year.

If in case dealers want to switch to the normal scheme, during the year, they may be allowed to do it. Although, they are not able to switch over to the Composition scheme again within the same Financial Year

Filing Returns Under the GST Composition Scheme

Individuals or registered taxpayers can pay tax under the provisions of Composition Scheme shall provide a return in official form and official manner within the eighteen days after the end of the relevant quarter.

GSTR- 4 form has been officially declared by the government for filing tax returns quarterly under the Composition Scheme. GSTR 4 form is specifically only for the dealers.

FAQs on GST Composition Scheme

Q1. Can a composition dealer purchase goods from an inter-state supplier?

Yes, of course, a person who has opted for composition scheme can procure goods from an inter-state supplier without any restrictions

Q2. What are the specified composition rates?

Composition rate is uniform for dealers & manufacturers at 1% ( 0.5% Central tax plus 0.5% State tax). Composition rate for Restaurant Services is 5% (2.5% Central tax plus 2.5% SGST) of the turnover. Composition rate for service providers is 3%

Q3. Is it mandatory for a Composition Dealer to maintain detailed records?

No, it is not mandatory for a registered Composition dealer to maintain detailed records as needed by a normal taxpayer

Q4. Is a Composition Dealers allowed to avail Input Tax Credit?

No, Composition dealer is not allowed to avail Input Tax Credit. A taxpayer who opts to pay tax under the composition scheme cannot take credit on his input supplies

Q5. Is composition dealer responsible to pay both, the Reverse charge and a fixed percentage of normal GST which he is supposed to pay?

If the reverse charge is applicable on a specific supply then the composition dealer is liable to pay GST under reverse charge as a recipient of supply at standard GST rates

Q6. Can the service provider go for the Composition Scheme?

Yes, Composition scheme for services has been introduced with an initial limit of Rs 50 Lakh, taxable at 6%, beginning from April 1, 2019

Q7. Can a person avail ITC on the stock after being denied to pay tax under composition from an authorised officer?

Yes a person can still avail ITC by filing a statement in FORM GST ITC-01 (containing details of input stocks along with the inputs contained in semi-finished or finished goods present in stock) on the date on which the option is refused as per order in FORM GST CMP07, within a period of thirty days from the order

Q8. When does an individual who opted for composition, pay tax?

An individual who opted for composition pays tax on a quarterly basis prior to the 18th* of the subsequent month of the quarter during which the supplies were made (changeable by the government notification)

Q9. Can a Composition Dealer issue Tax Invoices?

No, a Composition Dealer can not issue a tax invoice because he has to pay the tax out of his own pocket and he is not permitted to recover the same from the customers. He is bind to issue Bill of Supply

Q10. What are the different types of returns, a Composition Dealer has to file?

Q11. Can a Composition Dealer collect tax from customers?

No, a Composition Dealer has to pay taxes from his own sources and he is not eligible to recover the composition tax from the buyer

Q12. Can an interstate supplier opt for Composition Scheme?

An interstate supplier can not opt for Composition Scheme as it is available only for dealers imbibed in intra-state supplies

Q13. How is availed input credit treated when one switch on to Composition Scheme from the normal scheme?

In such a case when a person switches on to composition scheme from normal scheme, he/ she becomes accountable to pay an amount equal to the credit of input tax in terms of inputs present in stock on the day instantly after the date of the switchover. The remaining balance of input tax credit in the credit ledger after payment of such amount will be treated inconsiderable

Q14. Can I choose for Composition Scheme in one year and flip flop in the later year?

Yes, You are allowed to switch between the Composition Scheme and the normal scheme on the basis of your turnover. The same switchover can be declared on the GST Portal. However, this flip flop comes along with alterations in the way you issue invoices and file your returns

Q15. Is the alternative to pay tax under composition practicable at any time of the year?

No, the tax under composition cannot be paid at any time of the year. A registered taxpayer is supposed to provide a declaration on the GST Portal in FORM GST CMP-02 prior to the beginning of every financial year

SAG Infotech Blog is a source for all the 2019 latest GST notifications regarding Central, Integrated, Union Territory, Compensation cess and their respective taxes applicable. The following of latest GST notifications in accordance with proper laws, rules and rates is a must for every trading and business unit and will keep the tradition in a proper managerial way. Goods and services tax has been rolled out and almost every business unit must be working by the latest notifications being issued by the official government departments and according to the central board of excise and customs.

According to the notifications over the Central tax, follow and have a look at the link and be updated through the latest update over central tax issues. Also, the notifications regarding the central tax (rate) will keep you updated through the ups and downs in the rates of central taxes. Central taxes will be levied on the basis of Central GST and will be collected by the central government from every transaction of both interstate and intrastate in nature.

The exemption provided from the furnishing of Annual Return / Reconciliation Statement for suppliers of Online Information Database Access and Retrieval Services(“OIDAR services”).

Due date extended for furnishing FORM GSTR-1 for registered persons having an aggregate turnover of more than 1.5 crore rupees for the months of July 2019 to September 2019

The due date prescribed for furnishing FORM GSTR-1 for registered persons having an aggregate turnover of up to 1.5 crore rupees for the months of July 2019 to September 2019.

Date extension from which the facility of blocking and unblocking on an e-way bill facility as per the provision of Rule 138E of CGST Rules, 2017 to be applicable from 21.08.2019.

“Seeks to extend the due date for furnishing FORM GSTR-3B for the month of for the month of April 2019 for registered persons in specified districts of Odisha till 20.06.2019.”

“Seeks to extend the due date for furnishing FORM GSTR-1 for taxpayers having aggregate turnover more than Rs. 1.5 crores for the month of April 2019 for registered persons in specified districts of Odisha till 10.06.2019.”

Procedure notification for quarterly tax payment and annual filing of return for taxpayers claiming the benefit of Notification No. 02/2019– Central Tax (Rate), dated the 7th March 2019

“Seeks to extend the due date for furnishing of returns in FORM GSTR-3B for the Month of March 2019 for three days (i.e. from 20.04.2019 to 23.04.2019).”

“Seeks to extend the due date for furnishing FORM GSTR-1 for taxpayers having aggregate turnover more than Rs. 1.5 crores for the month of March 2019 from 11.04.2019 to 13.04.2019”

Notification No. 08/2017 – Central Tax dated 27.06.2017 in order to further extend the limit of the threshold of aggregate turnover for coming under Composition Scheme u/s 10 of the CGST Act, 2017 to Rs. 1.5 crores.

Prescribed due dates for the furnishing of FORM GSTR-1 for taxpayers having an aggregate turnover of more than Rs. 1.5 crores for the months of April, May and June 2019.

Prescribed due dates for furnishing FORM GSTR-1 for taxpayers having an aggregate turnover up to Rs. 1.5 crores for the months of April, May and June 2019.

Registration exemption for a business unit engaged in the exclusive supply of goods and whose aggregate turnover in the financial year does not cross Rs 40 lakhs.

Extension of due date for furnishing FORM GSTR-3B for the month of January 2019 to 28.02.2019 for registered persons having a principal place of business in the state of J&K; and 22.02.2019 for the rest of the States.

Amendment notification No. 65/2017-Central Tax dated 15.11.2017 bringing effects of amendments (to align Special Category States with the explanation in section 22 of CGST Act, 2017) in the GST Acts

“Seeks to specifies retail outlets established in the departure area of an international airport, beyond the immigrationcounters, making tax free supply of goods to an outgoing international tourist, as class of persons who shall be entitled to claim refund”

“To amend notification No. 11/ 2017- Central Tax (Rate) so as to extend the last date for exercising the option by promoters to pay tax at the old rates of 12%/ 8% with ITC”

Amendment of notification No. 02/2019- Central Tax (Rate) providing for the application of Composition rules to persons opting to pay tax under notification no. 2/2019- Central Tax (Rate).

Amendment of notification No. 13/2017- Central Tax (Rate) specifying services to be taxed under Reverse Charge Mechanism (RCM) as recommended by GST Council for real estate sector.

Rescinding the notification No. 8/2017-Central Tax (Rate) dated 28.06.2017 to bring in the effects of the amendments (regarding RCM on supplies by unregistered persons) in the GST Acts

GST Notifications on Integrated Tax and Rate in 2019

Integrated taxes will keep you informed and updated regarding the latest issues and rules and regulations of integrated taxes and the rates being decided the time to time. All the integrated taxes of state and central will be covered up in this section.

Amendment notification No. 10/2017-Integrated Tax dated 13.10.2017 bringing in the amendments (to align Special Category States with the explanation in section 22 of CGST Act, 2017) in the GST Acts

“Seeks to exempts any supply of goods by a retail outlet established in the departure area of an international airport, beyond the immigration counters, to an outgoing international tourist.”

“Seeks to specifies retail outlets established in the departure area of an international airport, beyond the immigrationcounters, making tax free supply of goods to an outgoing international tourist, as class of persons who shall be entitled to claim refund.”

“To amend notification No. 8/ 2017- Integrated Tax (Rate) so as to extend the last date for exercising the option by promoters to pay tax at the old rates of 12%/ 8% with ITC”

Amendment of notification No. 1/2017- Integrated Tax (Rate) notifying IGST rate of various goods as recommended by GST Council for the real estate sector

Amendment of notification No. 10/2017- Integrated Tax (Rate) specifying services to be taxed under Reverse Charge Mechanism (RCM) as recommended by GST Council for real estate sector.

Amendment of notification No. 8/2017- Integrated Tax (Rate) notifying IGST rates of various services as recommended by GST Council for real estate sector.

“Seeks to rescind Sl. No. 10D of Notification No. 09/2017-Integrated Tax (Rate) dated 28.06.2017 in relation to exemption of IGST on the supply of services having a place of supply in Nepal or Bhutan, against payment in Indian Rupees.”

Rescinding notification No. 32/2017-Central Tax (Rate) dated 13.10.2017 bringing in the amendments (regarding RCM on supplies by unregistered persons) in the GST Acts

2019 GST Notifications on Union Territory Tax and Rate

Union Territory section of notification is formed for the overall updates of rules and laws regarding the integrated taxes and its rates being levied across the designation union territories. All the 7 union territories along with New Delhi has been applied with UTGST and here you can catch every notification regarding the union territories updates.

The exemption from registration for the person within the exclusive supply of goods and having the aggregate turnover in the financial year does not exceed Rs 40 lakhs.

“Seeks to specifies retail outlets established in the departure area of an international airport, beyond the immigrationcounters, making tax free supply of goods to an outgoing international tourist, as class of persons who shall be entitled to claim refund.”

“Seeks to amend notification No. 11/ 2017- Union Territory Tax (Rate) so as to extend the last date for exercising the option by promoters to pay tax at the old rates of 12%/ 8% with ITC”

Amendment of notification No. 02/2019- Union Territory Tax (Rate) providing for application of Composition rules to persons opting to pay tax under notification no. 2/2019- Union Territory Tax (Rate).

Amendment of notification No. 1/2017- Union Territory Tax (Rate) notifying UTGST rate of certain goods as recommended by GST Council for real estate sector.

Amendment of notification No. 13/2017- Union Territory Tax (Rate) specifying services to be taxed under Reverse Charge Mechanism (RCM) as recommended by GST Council for real estate sector.

Amendment of notification No. 11/2017- Union Territory Tax (Rate) notifying UTGST rates of services as recommended by GST Council for real estate sector

Rescinding notification No. 8/2017-Union Territory Tax (Rate) dated 28.06.2017 bringing in the effects of amendments (regarding RCM on supplies by unregistered persons) in the GST Acts

GST Notifications on Compensation Cess & Rate in 2019

“Exempts any supply of goods by a retail outlet established in the departure area of an international airport, beyond the immigration counters, to an outgoing international tourist.”

Association of Chartered Accountants is voicing out against the confluent changes in the tax return filing software and forms seeking excess information about long-term capital gains tax.

In this regard the Bombay Chartered Accountant Society (BCAS) – India’s oldest voluntary body of Chartered Accountants, has written a letter to the finance minister Nirmala Sitharaman, seeking convenience in filing ITR. The letter calls attention to the chronology of form and changes introduced to the utility.

The letter of BCAS to FM asserts, “Constant tinkering with the forms necessitates changes in software on the e-filing portal; this in turn leads to delays in making the government utility available to taxpayers…The pain that is now being faced is beyond tolerance levels…,”

CA associations of Surat, Ahmedabad, Lucknow and Karnataka are also foreseeing to join the appeal made by BCAS regarding frequent updated in software which takes place during the intermediate period of ITR preparation.

Issues written by BCAS is about additional details of ISIN and Delayed introduction of Form 16s for employees.

ISIN (International Securities Identification Number) is a 12-digit alphanumeric number which is allotted to every security. This number is asked when the tax-payers furnish long-term capital gains. BCAS wrote that these additions to the utility which asks additional information about ISIN will complicate the situations as ITR forms are already notified. To this, a clarification was issued from the Central Board of Direct Taxes within a few hours which states that the tax-payers who have already filed ITR-1, before the changes in utility, will not have to file it again. So, 1.38 crore taxpayers who had filed their returns will not be required to consider the changes made to the utility.

Further, the issue regarding the lag in Form 16s for salaried professional was also called attention as chartered accountants had already filed returns for salaried class by June.

Raju Shah, former chairman of legal representation committee of CA Association of Ahmedabad said, “We couldn’t file returns in May-June as forms were notified late and salaried individuals didn’t receive their Form 16. In July, when we move over to business taxpayers, we are still getting salaried individuals returns,”.

To which CBDT made clarification saying, “Even though the utility is being updated regularly to provide ease to taxpayers, returns filed by using the previous version of the utility will continue to be valid. This means, those who have already filed the returns, will not need to re-file it as per the updated version of the software”.

Although the changes are made to bring ease for taxpayers, to combat tax evasion and to increase tax collection, the IT Dept. needs to bring in these mutations in their entire advertisements.

Chartered accountants study the changes and fare forward with them but taxpayers remain unaware about the same. It gives rise to a heavy-handed situation for the taxpayers as CA frequently visit them seeking additional information.

Taxpayers have a sole motto of filing the ITRs on time and not getting penalized with Rs 5,000, for delayed filing. So if the taxpayers will be on board with the latest notifications and changes, C.A. will find it easy to incorporate the alterations.

The government has announced a new feature into the GST system which will allow all the taxpayers to change the mobile number and email id of the particular taxpayers himself within the GST system.

The complaint earlier came in the scanner that most of the time authorized personnel who were designated for the application of registration had used their own contact details at the time of registration.

The finance ministry mentioned in the statement that, “the intermediaries who were authorized by them to apply for GST registration on their behalf had used their own email and mobile number during the process.”

This particular reason had let the government take such a technical step allowing taxpayers for modification in the contact details i.e. mobile number and email id.

Step by Step Procedure to Change Email ID & Mobile Number on Portal

The taxpayer will have to reach the applicable jurisdictional Tax Officer for the password of GSTIN allowed of his business

To check jurisdiction of the particular taxpayer one can log in to https://www.gst.gov.in where the jurisdiction allotted will be displayed in red text

The documents will be mandatorily required for the validation of its business according to its GSTIN

The tax officially will cross check the details and validate if the person is a stakeholder in the given GSTIN of business

The authentication will be done further after the tax office will upload the documents on the GST portal

Now the tax officer can modify the mobile number and email id of the taxpayers

After the documents uploading, the officer will reset the password for the GSTIN

The given email id will receive the username and temporary password

The login link can be used for the further modification of the password on GST portal login page https://www.gst.gov.in/

Finally, the taxpayer after login with a temporary password will be asked to change the username and password

The said procedure can be used for changing the old username and password by the taxpayer.

In the budget 2019, several GST related rules and regulations have changed which have been presented in the Finance Bill. Finance Minister Nirmala Sitharaman presented the budget 2019 on July 5, 2019. The budget promulgates the tax payment facilities in addition to the changes made in composition schemes. Most of the things presented in the Finance Bill are related to rules and regulations.

Changes in GST associated rules will increase taxpayers’ convenience while the introduction of the Amnesty Scheme will lead to the resolution of old cases.

GST council takes all the big decisions about GST in the presence of finance ministers of all states, wherein the President of this Council is the Finance Minister of the Central Government. All the decisions regarding the GST rate are taken in the GST council meeting.

List of All GST Changes Made in Budget 2019

Proposals regarding the cash transfer have also been made in the Finance Bill which proposes that from now on, any amount of taxes, interest, penalties and fees available in Taxpayers electronic cash ledger can be transferred as Central Tax, State Tax or Cess, subject to the condition that this amount should available in taxpayers’ electronic cash ledger.

Now taxpayers will be able to rectify the mistakes made during tax payments. New SubSection has been added to Section 49 of the CGST Act. Under this section, any tax or penalty which has been mistakenly paid in CGST by any registered person will now be able to get adjusted in IGST, SGST.

In the Finance Bill, it has been stated that interest will be charged only on the Net Tax liability. For instance, if a taxpayer’s liability is INR 1 lakh and he has an input tax credit of INR 50,000 and this taxpayer files a return after a fixed date, then interest will be charged only on INR 50,000 and not on INR 1 lakh.

If any company earns profits on speculation, then it will have to give 10 per cent of the profits as a penalty to the Anti-Profiteering Authority. The penalty must be given within 30 days of when Authority passes the order.

The option to fill the quarterly tax is also proposed in the Finance Bill. Now composition dealers will have to file the GST returns once a year and they can pay taxes on a quarterly basis. The other taxpayers who are filling monthly returns will be given the option to fill the UCO quarterly returns.

Another new proposal has been given in the Finance Bill which allows the Central Government to refund the amount of state tax to taxpayers.

The verification of the Aadhar card of all the taxpayers for GST has now become mandatory. Some taxpayers are kept out of this verification ambit.

The composition scheme has been provided for the people who supply intrastate goods or services and whose previous year turnover did not exceed Rs 50 lakh. 3 per cent GST rate is leviable it.

The budget also holds a proposal regarding the creation of a National Appellate Authority for Advance Ruling. If the appellate authority of 2 or more states gives separate rulings, then the National Appellate Authority will consider it.

Additionally, the new amnesty scheme under GST has been brought in the budget to resolve the old cases of service tax and excise. The name of this scheme is ‘Sabka Vishwas Legacy Dispute Resolution Scheme’. Under this scheme, the old cases related to these taxes will be resolved.

Apart from this, a 100 per cent discount will be allowed in late fees and a 70 per cent discount will be given in cases where there is a dispute regarding the tax figures. These benefits will be available only after the fulfilment of certain conditions.

SAG Infotech provides the best unlimited return filing, e-waybill, and billing GST software available for a free download. The Gen GST Version 2.0 software for FY 2019-20 being in-house developed by SAG Infotech which is a panacea for all the complex GST filing operations and tasks being assigned to the traders and business community by the government of India. It is available on both platforms i.e. desktop and online versions according to the users’ preference. Also to note down, Gen GST software is a product of utmost hard work and excellent skilled developers who have earlier given their services in the making of highly reputed taxation software i.e. Genius software, Gen XBRL etc. The GST software free download version works for PC/desktop smoothly.

Now one can also download the Gen GST Software free Demo is available absolutely free giving you insights on one of the most trusted and valuable GST software. Also, the company is giving a 10% discounton the paid version and lifetime free GST billing software available on SaaS version. The company has also decided to give GST software free download in full version with minimum conditions. The Gen GST software is ultra secured GST filing software which is developed with the most reliable JAVA language commonly used in the banking sector while the software is adaptable to any OS available or running in the market. The Gen GST software is capable of providing invoice format in excel, unlimited client return filing, GSTR 9 annual return filing with annual composition and audit form, credit ledger, cash ledger based upon data filled within the authorised format and also represents the availability of ITC Match/Mismatch report giving an error-less report result.

Steps to Download Free Gen GST Software (Trial Version for PC/Desktop)

First of all, open the https://saginfotech.com in the address bar of the browser

Click on the products tab and select GEN GST, Also you can click the topmost box to directly go to the product page

Now Click on the download free demo on the starting of the page for offline tool

After that fill the details in the orange enquiry box including Name, Email address and Mobile no. and Click send

You will receive the download link at the email address given by the interested user providing the chance for getting GST invoice software for free download

Outstanding Features of GEN GST Software (Desktop/PC):

Apart from e-filing and billing of tax, the GEN GST also provides numerous extraordinary features to its clients including,

Gen GST Online Desktop Features

GSTR 9 Annual Return Filing

GSTR 9A & 9C Annual Composition & Audit Forms

Unlimited Client Return Filing

Platform Independent

Java, Highly Secured Language

Generate, consolidate, update GST e waybill

Import Facility From Renowned Accounting Software

Creation of Masters

Industry Specific Billing Format

e-Filing

Summarized and rate wise sales figures report

Facility to export client data into excel via GST Software

Reconciliation of GSTR-3B with input credit register

Difference between GSTR 1 and GSTR 3B

Delete all data of GSTR-1 from the portal

Download all the return data from the GSTN portal on the single click

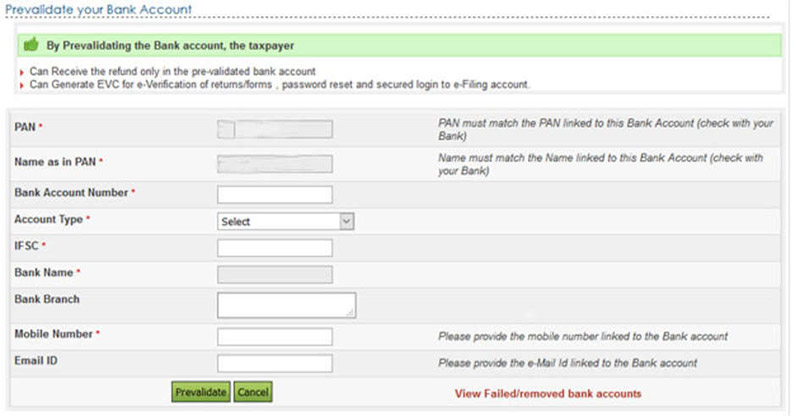

Tax system in India keeps on reforming for good. The Government and other tax-related departments are constantly working to make the tax system more rigid. One such reform is recently brought in practise by the Tax Department related to ‘Income Tax Refund’. Valid from the prevailing year onward, the one who claims Income Tax Refund has to pre-validate the bank account in which he wishes to receive the refund. Apart from that, the IT Department demands the bank accounts to be linked with the taxpayer’s PAN and if in any case the taxpayer fails to link the PAN, then the refund will not be credited in his account.

Experts say, “a taxpayer who is looking to claim the refunds must link the PAN to his bank account and also pre-validate the bank account on income tax e-filing website”. From now onward e-refund will be issued by the tax department and the refund will be credited to the bank account linked with PAN. Visit your bank branch to register your PAN with your bank account.

A Step-wise Guide to Pre-Validate your bank account:

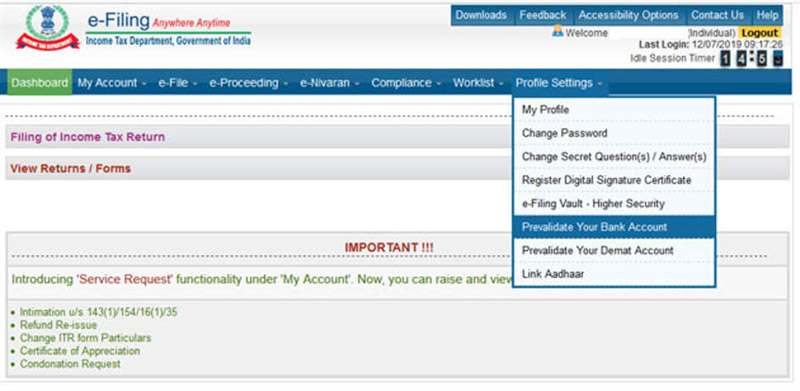

Step 1: Log in to your account on www.incometaxindiaefiling.gov.in. Your user ID is your PAN number.

Step 2: On the dashboard, select Profile Setting Tab and from the drop-down select ‘Prevalidate your bank account’ option.

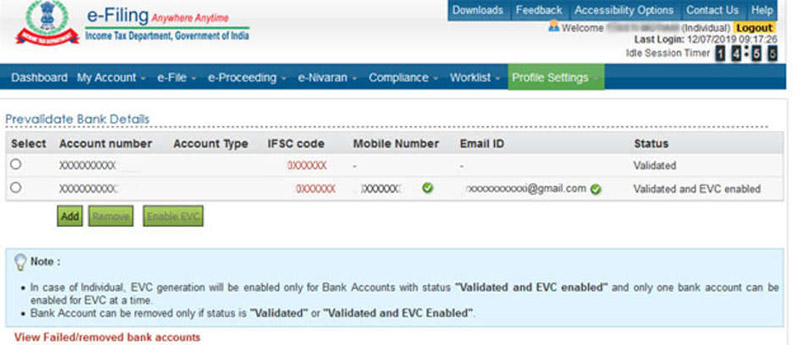

Step 3: The details of Pre-validated bank account (if any) will flash on the screen. If you don’t have a pre-validated account or if you want to pre-validate a new account, click on the ‘Add’ button.

Step 4: You will land on the application form for Pre-validating the bank account. You need to fill the relevant details such as bank account number, account type, bank name, branch name, IFSC, your mobile number and your email id. Take note on the mobile number and email id as they should match with the bank records.

Step 5: As soon as you click the pre-validate button visible in the bottom of the form you will see a message saying “Your request for pre-validating bank account is submitted. Status of your request will be sent to your registered email id and mobile number”.

Quick Tips that might help you while pre-validating your bank account:

You can even check the status of your bank account by going back to Pre Validate your bank account under Profile Settings Tab. If your account is pre-validated it will appear on the screen.

In case if you want to remove a bank account, go to the ‘Pre Validate your bank account’ under Profile Settings Tab, select the account you want to remove then click on the ‘Remove’ tab.

To see the bank accounts where pre-validation has failed, you can click on ‘View Failed/removed bank accounts’ visible at the bottom of the web page. After clicking, it will display the details of the removed or rejected bank accounts with the reason for removal or rejection.