PAN cards will now be issued online and instantly in India by the Income Tax Department. This is a good move towards digitalization of services by the Income Tax Department.

Applicants will not need to fill out an application form and submit the required documents manually as now the income tax department would procure the details from the Aadhar card of an applicant and issues a PAN card instantly. Besides the facility is free to use.

The procedure is entirely online and since it knocks off every single manual processing which consumes a time-frames of 15 days, the e-PAN facility guarantees a “near to real-time” process.

Read Also: Simple Steps for Filling New PAN Card Application Online

To apply for the instant e-PAN, the applicants would need to quote their basic details such as name & address along with Aadhaar details which are mandatory to be mentioned. The details would need to be verified by the applicants using a one-time password (OTP) which will be sent on their registered mobile phone number. Since Aadhaar card already carries details such as Date of birth, Address and Father’s name so the applicant would not need to upload any substantial document as an address proof or any other evidence. However, it should be noted that applicants must send correct Aadhaar details because any mismatch would lead to the rejection of the application.

Once the details of Aadhar get verified through OTP, a digitally signed e-PAN will be issued to the applicant. The e-PAN will feature a QR code that will carry the applicant’s photo and demographic information in an encrypted manner for security reasons and to avert the risks of fraudulence & forgery or digital photoshopping.

Read Also: Avoid Errors in Aadhaar/PAN for Income Tax Return Filing

“The move is part of greater digitization of income tax services and aimed at providing the facility without anyone having to visit any office,” an official said.

The e-PAN facility will benefit the new applicants as well as the existing PAN users. A few clicks and minutes, the existing PAN holders will get a duplicate.

In the ongoing pilot test of the instant e-PAN service, more than 62,000 e-PANs have been issued in the period of merely eight days. After the successful test, the facility will be launched throughout the country.

Goods and Services Tax ( GST ) department has received orders by the Punjab and Haryana High Court to reinitiate the facility of filing or revising Tran-1. The directions have been given to the GST department to allow the Petitioners to file TRAN-1 Form or revise their already filed erroneous TRAN-1 either electronically or manually.

Petitioners have been urging the High courts for directions under Article 226 of the Constitution of India to Respondents for allowing them to carry forward the unutilized CENVAT credit of duty discharged under Central Excise Act, 1944 and Input Tax Credit of VAT paid under PVAT Act, 2005 or HVAT Act, 2003.

These petitioners are registered under the Central/State Goods and Services Tax Act, 2017 and their credits could not be carry forwarded because they either failed to file the stipulated Form i.e. TRAN or filed it incorrectly by the prescribed due date of 27th December 2017.

Such petitioners have been behesting for permitting them to revise the incorrect TRAN or file a new TRAN in any mode and carry forward the unclaimed credits.

Justice Jaswant Singh and Justice Lalit Batra of the division bench decided and directed to allow the claimants to claim the transitional credit of the eligible CENVAT / ITC duties by filing a declaration in GST TRAN-1 and GST TRAN-2 Form.

It should be noted that only those duties are permitted to be claimed which are related to the inputs kept in stock on the appointed day as per Section 140(3) of the Act.

The Court also said that “the due date contemplated under Rule 117 of the CGST Rules for the purposes of claiming transitional credit is procedural in nature and thus should not be construed as a mandatory provision”.

Petitioners are given a time-restricted opportunity to claim or carry forward their unclaimed credit. 30th November 2019 is the due date of filing the statutory Form(s) TRAN-1 or revising an already filed erroneous TRAN.

“The Respondents are at liberty to verify the genuineness of claim of Petitioners but nobody shall be denied to carry forward the legitimate claim of CENVAT / ITC on the ground of non-filing of TRAN-I by 27.12.2017”, added by the Court.

As anticipated the GST collections for the month of October the collection took turns for the INR 95,380 crores only which is less than the normal peak stable fo 1 lakh crore of targets. The same collections for the month of October from the previous year were 1,00,710 crore.

The central GST was evaluated at 17,582 crores, state GST came at 23,674 crores, Integrated GST came at 46,517 crores while the cess collection came at 7,607 crore rupees for the month of October for the government.

Also, there was a total of 73.83 lakh of GSTR 3B returns filed in the month which have not brought any significant collections to the government.

GST collection was at a 19-month low in September

Information received by the Revenue Department had revealed a total GST collection of Rs 91,916 crore in September 2019. The figure was at a 19-month low. Even in the month of August, the GST collection figure was Rs 98,202 crore. However, the economic slowdown was said to be the reason for the decrease in GST collection in both the months.

A reduction of approx 2 lakh crore rupees in the total tax collection in the financial year 2019-20 is likely to happen. The government has informed the Finance Commission regarding the same. The central government had estimated the gross tax collection of Rs 24.6 lakh crore in the current fiscal year.

Initially, the estimate was Rs 22.5 lakh crore. The total tax collection this year was Rs 21 lakh crore. This means that the government needs to increase the total tax collection by 18 per cent to meet its target in the current financial year. Government of India needs more than Rs 1 lakh crore GST to meet its fiscal target but not to offset the state-level losses as GOI is responsible to compensate the states for its revenue losses only once in every two months for the first five years of GST onset.

Read Also: First Meeting of GST Review Committee Went Inconclusive

The government has already compensated the states with Rs 27,955 crore and Rs 17,789 crore in June-July & April-May this year, respectively.

The tax collection in the month of September came out to be the lowest in nineteen months which is another symbol of economic downturn. In such a scenario, the government’s concern regarding the GST collection and economic improvement has increased because of poor tax collection.

The state of Jammu & Kashmir has been bifurcated into two Union Territories – Union territory of Jammu and Kashmir and Union territory of Ladakh.

According to the Table II, in column (3), in serial number 51, of the concerned notification by the government of India, dated 19th July, 2019, the words “State of Jammu and Kashmir” shall be replaced by the words “Union territory of Jammu and Kashmir and Union territory of Ladakh”.

The Jammu and Kashmir Reorganisation Act, 2019 of Indian Parliament contains provisions regarding the reformation of the state of Jammu and Kashmir into two union territories on 31 October 2019.

According to this Act, the state GST Act will continue because without this the issues related to enforcement of the indirect tax on the two union territories will spawn out and also J&K has the assembly of its own. GST Act for union territories will have to be made for Ladakh for which law will have to be passed.

Read Also: What is Union Territory GST (UTGST) and Why It Is Implemented

The government shall exercise the powers specified under section 5 of the Central Goods and Services Tax Act, 2017 (12 of 2017) along with section 3 of the Integrated Goods and Services Tax Act, 2017 (13 of 2017).

Besides, the government will simultaneously have to hammer away other issues for the smooth execution of the GST regime. Both the Union Territories, as well, will need to acquire separate registration under GST and carry out other procedural formalities. GST will be levied on any kind of supply between these two Union Territories.

As the deadline for filing GST returns under the new, revised mechanism is approaching, many taxpayers are still confused regarding the new rules for claiming a refund of input tax under GST. So, they are now waiting for some kind of clarification from the government’s side over the revised mechanism, which limits the maximum amount of input tax credit to 20% of the total eligible amount.

The GST returns under the new rules will begin starting from next week.

Earlier this month, the GST Council had announced updates in its GST refund policy, which restricts the ITC amount to a maximum of 20% of the claim amount in case of suppliers have not uploaded documents or details in the form GSTR 1.

Since it is still a new rule, there is a lot of confusion around it, as to where and how the rule is applicable. Moreover, businesses are also likely to face cash-flow challenges if their input credit refunds are restricted on the grounds of unavailability of supplier documents.

The decision to limit input credit refund was taken to reduce the instances where businesses were acquiring input tax credit by uploading fake returns. However, the lack of clarity over the new rules may do more harm than good. “GST returns of October 2019, which will be filed on or before 20th November are going to be the first return after introduction the newly introduced restrictions of 20 per cent,” says a Mumbai based Chartered Accountant.

One of the confusions among the taxpayers is how exactly the government will decide how much is the input tax credit eligible for a particular time. The input credit mechanism was introduced by the government to avoid tax cascading and refund the input tax amount back to the taxpayer while paying output tax. “Online credit is a dynamic amount so how to determine 20 per cent of it will be another issue to be addressed.”

Moreover, taxpayers also need clarity over the time or date for matching of invoices, since the process of return filing and invoice matching happens online only through the GSTN portal.

It was not until this month, two years after GST implementation, that the GST Council chose to activate the provision to match invoices, which was already mentioned under section 43A since the very beginning. This was because the government had come across several cases where some companies were reportedly misusing the input tax credit mechanism by claiming ITC on fraud invoices.

Another thing that troubles taxpayers is that only a part of the section 43A has been introduced, as of now. Since the remaining section is yet to be made effective, there is big uncertainty regarding the applicability of the rule in specific cases.

The 37th GST council took the decision to not to levy GST on the intermediary deals applicable on the various international transactions. However, the decision has not come through the notification.

As per the decisions, it is cleared that the intermediaries giving services to the person receiving supply and the recipient of the goods are from outside India will not come under the GST tax ambit.

Currently, there is an 18% GST applicable to the intermediaries who are giving services to the outsider of India. There is a defined definition of the intermediary in the GST act.

It states that “a broker, an agent or any other person who arranges or facilitates the supply of goods or securities or services between two or more persons.”

While it does exclude the person who is supplying the goods and services and even both of them on his own account. The rule is applicable to the export of the services of the intermediary to the outside of India.

But both the giving and receiving of goods and services and the intermediary location are all different under which the latter is inside the India which makes him out of the ambit of GST as per the decision of GST council.

If the outward supply is made there has to be input tax credit reversed making the transaction tedious for both the taxpayer as well as the government.

It is to be seen how the decision will affect the intermediary service providers to outside of India which an impact on their cash flow due to the no input tax credit claim.

There is no notification in this regard, therefore, the decision is still not affixed.

The government releases the GST return forms details which are mandated to be filed according to the due dates under GST mentioned in the attached notification. The submission and uploading of the returns are totally online. We have mentioned all the GST return filing due dates along with their respective associated GST forms such as GSTR 1, GSTR 3B, GSTR 4, GSTR 5, GSTR 6, GSTR 7, GSTR 8, GSTR 9, GSTR 9A, GSTR 9C in FY 2019-20 etc.

Find GST Forms’ Current Due Dates Below:

GSTR 1 Due Date (Turnover up to 1.5 Crore) | GSTR 1 (Turnover more than 1.5 Crore)

GSTR 3B Due Date

GSTR 4 Due Date

GSTR 5 Due Date | GSTR 5A Due Date

GSTR 6 Due Date

GSTR 7 Due Date

GSTR 8 Due Date

GSTR 9 Due Date | GSTR 9A Due Date | GSTR 9C Due Date

GST Calendar of Return Filing Due Dates in October 2019

Government announce GST return filing due dates from time to time in order to maintain taxation in line with respective clearance. Also, the main effort is to alert the taxpayers regarding the GST return filing due dates is to make them neglect any penalty or interest. Here we are offering GST due dates calendar for October 2019 for all the registered taxpayer under indirect tax regime to make them aware of the time period as of when to get their GST return filing done on time.

As GSTR 1 & GSTR 3B is to be filed every month, there is a greater need of getting regular updates/notification based on GST due dates calendar for avoiding any interest and penalty. Also, there is GST CMP 08 for the composition scheme dealers but it has to be filed every quarter lowering down the need for regular updates on GST due date filing calendar.

GST Return Form Name

Filing Period

Due Dates in October 2019

GSTR 7

Monthly

10th October

GSTR 8

Monthly

10th October

GSTR 1

Monthly

11th October

GSTR 6

Monthly

13th October

GSTR 3B

Monthly

20th October

Note: The revised due dates and above announcements have been implemented under official CBEC GST notification & latest GST circulars/orders by Govt. CBIC department

GST Return Filing Due Dates Chart 2019

All these changes are described below:

GSTR 1 Due Dates (T.O. up to INR 1.5 Crore)

Period (Quarterly)

Last Dates

October – December 2019

31st January 2020

July – September 2019

31st October 2019

April – June 2019

31st July 2019

How to File GSTR 1 with Complete Online Return Filing Procedure

GST Return 1 Due Date (T.O. More Than INR 1.5 Crore)

Period (Monthly)

Last Dates

October 2019

11th November 2019

September 2019

11th October 2019

August 2019

11th September 2019

July 2019

11th August 2019 | Note: “The due date extended till 20th September 2019 for notified districts of Bihar, Gujarat, Karnataka, Kerala, Maharashtra, Odisha, Uttarakhand and also for registered persons whose principal place of business is in J&K.” Notification Here

June 2019

11th July 2019

May 2019

11th June 2019

April 2019

10th June 2019 for Odisha, Read Notification

March 2019

Revised – 13th April 2019 | Read Notification

February 2019

11th March 2019

January 2019

11th February 2019

Note:

“The late fee shall be completely waived in case of GSTR-1 for the time period of months/quarters July 2017 to September 2018, which are furnished after 22nd December 2018 but on or before 31st March 2019”

“All the newly migrated taxpayers, a due date extended for furnishing GSTR-1 for the time period of quarterly July 2017 to December 2018 respectively till 31st March 2019”

The filing of GSTR-2 and GSTR-3 has been suspended by the Committee of Officers, which will resume after 30th June 2018. The detailed schedule shall be updated accordingly. The further months of filing for GSTR-1 and GSTR 3B are also decided to be filed till for 6 more months as announced by GST council meeting.

GSTR 3B Form Filing Due Dates

Period (Monthly)

Due Dates

September 2019

20th October 2019

August 2019

20th September 2019

July 2019

22nd August 2019 | Note: “The due date extended till 20th September 2019 for notified districts of Bihar, Gujarat, Karnataka, Kerala, Maharashtra, Odisha, Uttarakhand and also for registered persons whose principal place of business is in J&K.” Notification Here

June 2019

20th July 2019

May 2019

20th June 2019

April 2019

20th June 2019 (Odisha) | Read Notification

April 2019

20th May 2019

March 2019

23rd April 2019 (Revised)

February 2019

20th March 2019

January 2019

22nd February 2019 (Due Date Revised) | 28th Feb 2019 for J&K Read Notification

December 2018

20th January 2019

November 2018

20th December 2018

October 2018

20th November 2018

Guide to File GSTR 3B with Online Return Filing Procedure

Note:

“The late fee shall be completely waived in case of GSTR-3B for the time period of months/quarters July 2017 to September 2018, which are furnished after 22nd December 2018 but on or before 31st March 2019”

“All the newly migrated taxpayers, a due date extended for furnishing GSTR-3B for the time period of July 2017 to February 2019 respectively till 31st March 2019”

GST Return 4 (CMP 08) Quarterly Payment Filing Due Dates for FY 2019-20

Period (Quarterly)

Due Dates

1st Quarter – April to June 2019

31st August 2019 | Due Date Extended in 36th GST Council Meeting

2nd Quarter – July to September 2019

18th October 2019

3rd Quarter – October to December 2019

18th January 2020

4th Quarter – January to March 2020

18th April 2020

GSTR 4 Guide with Step by Step Filing Procedure

Note:

GSTR 4 return revisions under 32nd GST council meeting: File annually return instead of quarterly along with tax paid to be the quarterly basis.

GST Return 5 (Non-Resident Foreign Taxpayers) Monthly Filing Due Date

Period (Monthly)

Due Dates

September 2019

20th October

August 2019

20th September

July 2019

20th August 2019

June 2019

20th July 2019

May 2019

20th June 2019

April 2019

20th May 2019

March 2019

20th April 2019

February 2019

20th March 2019

January 2019

20th February 2019

December 2018

20th January 2019

November 2018

20th December 2018

GSTR 5 Onlne Filing Procedure

GST Return 5A (Non-Resident OIDAR Service Provider) Filing Due Date

Period (Monthly)

Due Dates

September 2019

20th October 2019

August 2019

20th September 2019

July 2019

20th August 2019

June 2019

20th July 2019

May 2019

20th June 2019

April 2019

20th May 2019

March 2019

20th April 2019

February 2019

20th March 2019

January 2019

20th February 2019

December 2018

20th January 2019

November 2018

20th December 2018

GSTR 5A Online Filing Procedure

Due Dates for GSTR 6

Return Monthly

Due Date

October 2019

13th November 2019

September 2019

13th October 2019

August 2019

13th September 2019

July 2019

13th August 2019 | Note: “The due date extended till 20th September 2019 for notified districts of Bihar, Gujarat, Karnataka, Kerala, Maharashtra, Odisha, Uttarakhand and also for registered persons whose principal place of business is in J&K.” Notification Here

June 2019

13th July 2019

May 2019

13th June 2019

April 2019

13th May 2019

March 2019

13th April 2019

February 2019

13th March 2019

January 2019

13th February 2019

December 2018

13th January 2019

Note:- TRAN-2 July to December 2017 has been announced to be filed until 30th June 2018.

GSTR 7 Due Date for TDS Deductor

Return Monthly

Due Dates

October 2019

10th November 2019

September 2019

10th October 2019

August 2019

10th September 2019

October 2018 to July 2019

31st August 2019 | Read CBIC Notification Note: “The due date extended till 20th September 2019 for notified districts of Bihar, Gujarat, Karnataka, Kerala, Maharashtra, Odisha, Uttarakhand and also for registered persons whose principal place of business is in J&K.” Read Notification

GSTR 7 Online Filing Guide

GSTR 8 Due Date for TCS Collector

Return Monthly

Due Date

October 2019

10th November 2019

September 2019

10th October 2019

August 2019

10th September 2019

July 2019

10th August 2019

June 2019

10th July 2019

May 2019

10th June 2019

April 2019

10th May 2019

March 2019

10th April 2019

February 2019

10th March 2019

January 2019

10th February 2019

October, November & December 2018

7th February 2019 | Read Official ROD Here

GSTR 8 Online Filing Guide

Due Date for GST Return 9 Annual Form

Return Annually

Revised Due Date

GSTR 9 (Annual Return) FY 2017-18

30th November 2019 (Check Order No. 7/2019-Central Tax)

GSTR 9 (Annual Return) FY 2018-19

31st December 2019

GSTR 9 Online Filing Guide

Note: Filing of form GSTR-9 for those taxpayers who (are required to file the said return but) have aggregate turnover up to Rs. 2 crores made optional for the said tax periods for FY 2017-18 and FY 2018-19 by GST Council 37th meeting. Read Official Press Release

Due Date for GST Audit Form 9C

Return Annually

Revised Due Date

GSTR 9C (GST Audit Form) FY 2017-18

30th November 2019 (Check Order No. 7/2019-Central Tax)

GSTR 9C (GST Audit Form) FY 2018-19

31st December 2019

GSTR 9C Online Filing Guide

Due Date for GST Return 9A Composition Annual Form

Return Annually

Revised Due Date

GSTR 9A (Composition Annual Return) FY 2017-18

30th November 2019 (Check Order No. 7/2019-Central Tax)

FY 2018-19

31st December 2019

GSTR 9A Online Filing Guide

Note: Waiver of the requirement of filing GSTR-9A form for the said tax periods (FY 2017-18 and FY 2018-19) by GST Council 37th meeting. Read Official Press Release

Due Date for GSTR 10

Return

Due Date

GSTR 10

3 months of the registration cancellation date or order cancellation date, whichever comes late

Regular Last Dates of GST Return for Indian Tax Payers

GST Forms

GST Due Dates

Associated Tax Payers

GSTR 1

Divided into 2 categories, Up to 1.5 Crores (Last Day of the Succeeding Month Quarterly) and More than 1.5 Crores (11th Day of the Succeeding Month Monthly)

Regular Dealers Outward Supplies (Sales)

GSTR 1A

–

Outward supply details of Business unit Corrected or Deleted

GSTR 2

To be updated

Regular Dealers Inward Supplies (Purchase)

GSTR 2A

–

Inward supply reconciliation in Form GSTR-1 by the supplier to business

GSTR 3

To be updated

Regular Dealers Monthly Return

GSTR 3A

–

Notice of failure of returns furnishing to the registered taxpayer

GSTR 3B

20th of Next Month (Only from July 2018 to March 2019)

All Dealers

GSTR 4

Annually

Composite Dealers

GSTR 4A

–

Inward supplies reconciliation under composition scheme in form GSTR-1 as supplier furnished

GSTR 5

20th of Next Month

Non-Resident

GSTR 6

13th of Next Month

Input Service Distributors

GSTR 6A

–

Inward Supplier reconciliation by ISD in form GSTR-1 as supplier furnished

GSTR 7

10th of Next Month

TDS Returns

GSTR 7A

–

Certificate of TDS

GSTR 8

10th of Next Month

E-Commerce Operators

GSTR 9

31st December of Next F.Y.

Registered Taxable Person

GSTR 9A

31st December of Next F.Y.

Taxpaying compounding of Annual return

GSTR 9C

31st December of Next F.Y.

GST Audit Form

GSTR 10

Within three months of the date of cancellation or date of cancellation order, whichever is later

Final Return for the taxpayer after surrendering or cancellation of the registration

GSTR 11

28th of Next Month

Inward supplies statement for the person having UIN

Interest on Late GST Payment and Penalty on Missing GST Return Due Dates

The GST Council has decided to levy interest of 18 percent on the late payment of taxes under the GST regime. The interest would be levied for the days for which tax was not paid after the due date. You can read more details of the GST penalty provision in chapter 10, part 50 at this link https://cbec-gst.gov.in/CGST-bill-e.html

Let’s understand this by an example: If the total tax liability of a person is Rs. 1,000 and doesn’t pay tax continuously for a few days after the due date, then the interest amount will be calculated as 1000*18/100*1/365= Rs. 0.49 per day approx. So, the person will have to pay this much interest each day after the due date.

In case if a taxpayer does not file his/her return within the due dates mentioned above, he shall have to pay a late fee of Rs. 50/day i.e. Rs. 25 per day in each CGST and SGST (in case of any tax liability) and Rs. 20/day i.e. Rs. 10/- day in each CGST and SGST (in case of Nil tax liability) subject to a maximum of Rs. 5000/-, from the due date to the date wheGST Due Dates: GSTR 1 GSTR 3B GSTR 4 GSTR 5 GSTR 6 GSTR 9n the returns are actually filed.

Recommended – Due Dates of GST Payment Along with Penalty Charges on Late Payment

GST Return Forms in Brief with Due Dates

GSTR 1 – The form is associated with every registered dealer who is under the regular scheme will have to file their outward supplies (sales) within 40 days from the end of the month.

GSTR 2 (Only for Regular Dealers Inward Supplies – Temporarily Closed) – The GST due date for the form is to be decided by the committee and the data can be uploaded on a daily basis whenever required.

GSTR 3 (Only for regular dealers Monthly return -Temporarily Closed) – The due date for the form is to be decided by the committee.

GSTR 3B (Summary Return Filing Form for Regular Dealers) – 20th of Next Month (Only from July 2018 to March 2019)

GSTR 4 (For composite dealers Quarterly Return) – The GST due date for the form is on or before 18th of next month after the end of the quarter in which the return is filed and it must be of previous three months.

GSTR 5 (Return for Non-Resident) – The due date for the submission of the form is 20th of next month and at the time of closure of the business within 7 days.

GSTR 6 (Input Service Distributor) – The GST due date for return filing for GSTR 6 form is 13th of next month in which the return filed.

GSTR 7 (TDS Return) – The due date for return filing for the form GSTR 7 is 10th of next month in which return is filed.

GSTR 8 (E-Commerce operator) – The GST due date for return filing for the form GSTR 8 is 10th of every next month in which the return is filed.

GSTR 9 (Annual Return of the normal dealer) – The GSTR 9 form is a mandatory form which must be filed on or before 31st December.

GSTR 9A (Annual Return for the composition dealer) – The GSTR 9A form is a mandatory form which must be filed on or before 31st December.

GSTR 9C (GST Audit Form) – The GSTR 9C audit form is a mandatory form which must be filed for companies that turnover exceeds 2 crores in a particular financial year on or before 31st December.

GSTR 10 – Final Return for the taxpayer after surrendering or cancellation of the registration. View the GSTR 1 form

GSTR 11 (INWARD SUPPLIES STATEMENT FOR UIN) – (INWARD SUPPLIES STATEMENT FOR UIN HOLDERS) – The due date for the GSTR 11 form is 28th of the month following the month for which statement is filed.

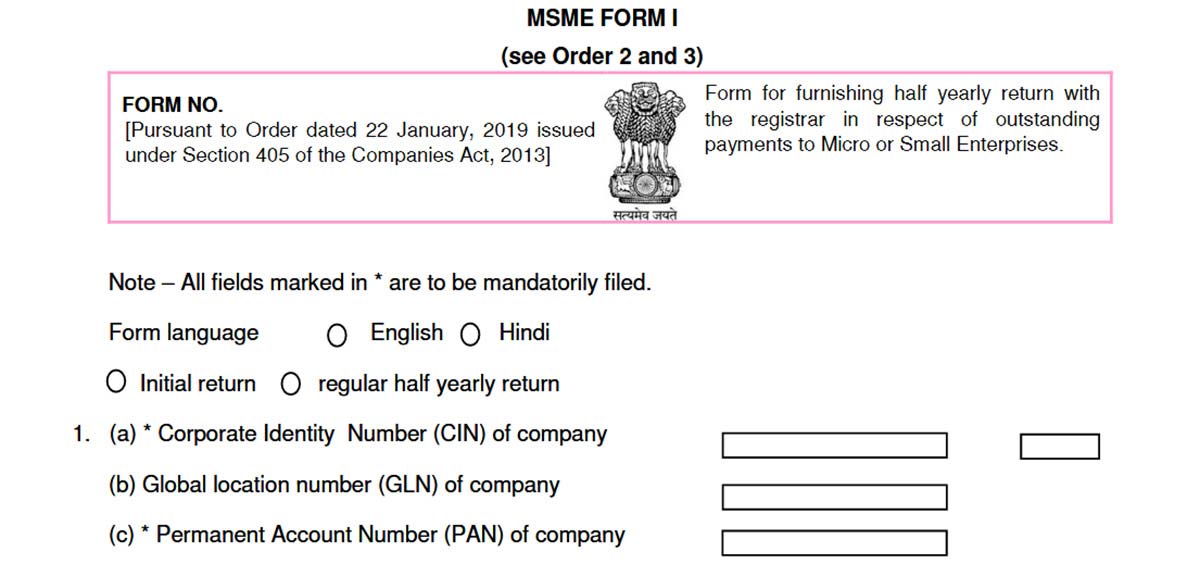

The Criterion for filing MSME I form (MCA) by those specified companies whose outstanding payment to MSMEs suppliers is exceeding 45 days, is being discussed below:

Order Named: Specified Companies (Detailed information regarding payment to micro and small enterprise suppliers) Order, 2019

Date of Notification: In context to Order dated January 22, 2019, issued under Section 405 of the Companies Act, 2013

Effective Date: From the Date of Publication in the Official Gazette

Note: File MSME Form 1 As Per the Applicability of the Provisions by Complaw Software

What is MSME Form 1 (MCA)?

The MSME I Form is for the payment of half yearly return with the Registrar of Companies (ROC) in context of the outstanding payments to Micro or Small Enterprises.

Major changes have been made by the Ministry of Corporate Affairs in the context of protecting the interest of the small group of companies or business. He laid emphasis on following compliance by all Specified Companies Whether Public or a Private Company, Micro or Small.

Recommended: Due Dates of Filing ROC Annual Return by Companies

A half-yearly return is required to be submitted to the Ministry of Corporate Affairs on a mandatory basis, by all those companies who receive supply of goods or services from Micro or small enterprises and the payment done to these micro and small enterprise suppliers exceeds forty-five days from the date of acceptance (or deemed acceptance) of the relevant good or services.

The following points should be stated in it:

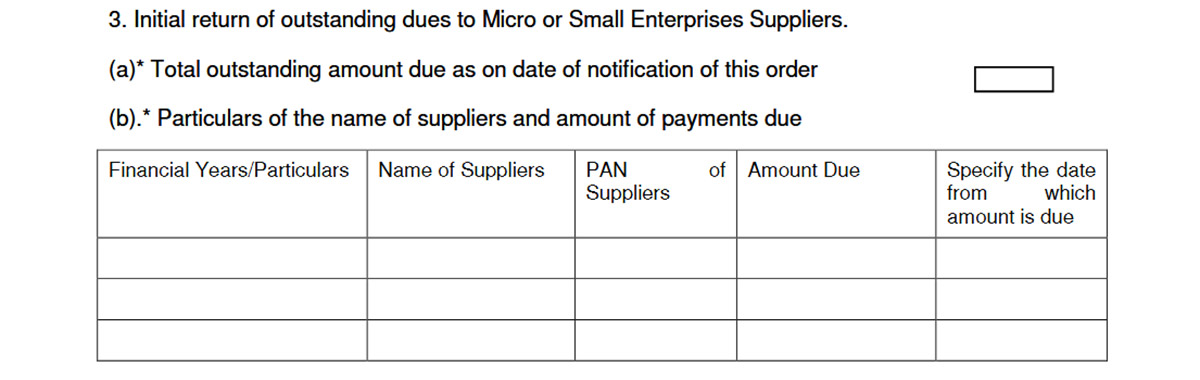

the amount of payment due and

the reasons for the delay

Following the provision of section 405 of the Companies Act, 2013, (18 of 2013) the Central Government made it necessary for all the “Specified Companies” to furnish the above-notified information about the payment to micro and small enterprise suppliers.

MSME Form 1 Due Date (Initial Return)

The government has declared the MSME form 1 due date till 30th May 2019 for all eligible companies. The department earlier said that the due date for companies to file the form will be 30 days from when it is uploaded on the official website. Read the notification here.

MSME Form 1 Due Date (Half Yearly Return)

Form MSME I (half yearly return) has to be filed within 30 days from the end of each half year in respect of outstanding payments to Micro or Small Enterprise i.e. 31st October 2019 (April 2019 to September 2019) 30th April 2020 (for October 2019 to March 2020). Read the notification here.

Important Definitions:

Specified Companies: As per the provisions of section 9 of the MSME Development Act, 2006, Specified companies are those companies who receive the supply of goods or services from MSMEs and the payment against these supplies to the suppliers of these MSMEs exceed 45 days from the date of acceptance (deemed acceptance) of the goods or services

Micro and Small Enterprise: The Micro and Small Enterprise mentioned above mean any class or classes of enterprises (including proprietorship, Hindu undivided family, partnership firm, company, undertaking, an association of persons or co-operative society), in which conditions applied are as per below:

Manufacturing Sector

Conditions applied

Enterprises

Investment in plant & machinery

Micro Enterprises

Does not exceed twenty-five lakh rupees

Small Enterprises

More than twenty-five lakh rupees but does not exceed five crore rupees

Service Sector

Conditions applied

Enterprises

Investment in equipment

Micro Enterprises

Does not exceed ten lakh rupees:

Small Enterprises

More than ten lakh rupees but does not exceed two crore rupees

Note: The Criteria specified above are specified bases Micro, Small and Medium Enterprises Development Act, 2006 and the bill to change the criteria of classification and to withdraw the MSMED (Amendment), 2015 is pending in the Lok Sabha.

The MSME Act, 2006 defines the Micro Small and Medium Enterprises.

Read Also: All About of MCA E-Form INC-22A with Step by Step Filing Process

MSME Act, 2006, MSME Broadly Classified Into 2 Categories

1) In the First category comes to those Enterprises which are engaged in the manufacturing and production of goods for any industry.

Manufacturing Enterprises – As per the first schedule to the industries (Development and Regulation) Act, 1951, the Manufacturing enterprises defined in terms of investment in Plant & Machinery, are those enterprises that are engaged in the manufacture or production of goods for any specific industry

2) In the second category comes to those enterprises which are engaged in providing or rendering services

Service Enterprises – Defined in terms of investment in equipment, service enterprises are those enterprises which are engaged in providing or rendering services

Under the MSMED Act 2006, the Micro Small & Medium Enterprises (MSMEs) in India are categorized and defined on the basis of capital investment done in plant and machinery but excluding the investments made in land and building.

Micro & Small Enterprise Category

In the Micro and Small Enterprise category there are entities which include Proprietorship, Hindu Undivided Family, Partnership Firm, Company, Undertaking, an Association of Persons or Co-Operative Society.

Applicability on Companies:

As per a notification issued by the MCA it has been mandated to file disclosures through Form MSME I for every type of the Company – Public or Private Company, Micro or Small Companies; the Company that satisfies the following two conditions:

Condition 1: Company must have received Goods and/or Services from Micro or Small Enterprise

Condition 2: Payment must have been due/not paid, to such Micro and Small Enterprise for 46 days from the date of acceptance

Note: Date of deemed delivery refers to the acceptance of goods and services by the buyer in written with no objection with the product or services received within the 15 days time period.

Late Filing Penalty for MSME Form 1

The section 405(4) which includes non-furnishing/incomplete/incorrect information penalty states a fine up to Rs.25000 (Co.,), Rs.25000/- (Min) & Rs.3 lacs (max) and imprisonment of 6 months for directors or both. Therefore it is mandatory for directors to file the MSME form 1.

Procedure for Filing MSME Form 1 (MCA)

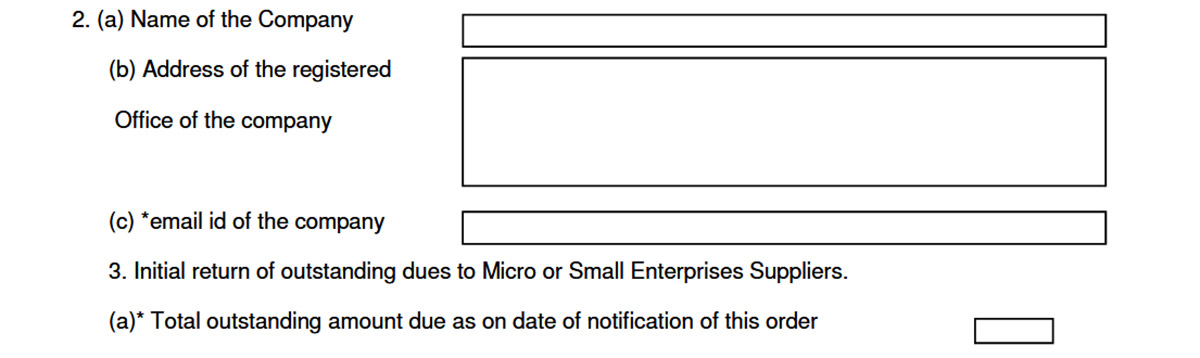

The Initial one-time Return: The companies should file, the MSME Form I detailing all the outstanding/ dues against the Micro or small enterprises suppliers that are existing on the date of notification of the related order within 30 days from the date of deployment of E-form MSME-1 on the MCA Portal.

Last date for filing Initial Return (One time return) in form MSME 1: Within 30 days from the date when E-form MSME-1 shall be deployed on the MCA Portal. Note: (as per the extended notification of MCA dated 21.02.2019). Read Notification

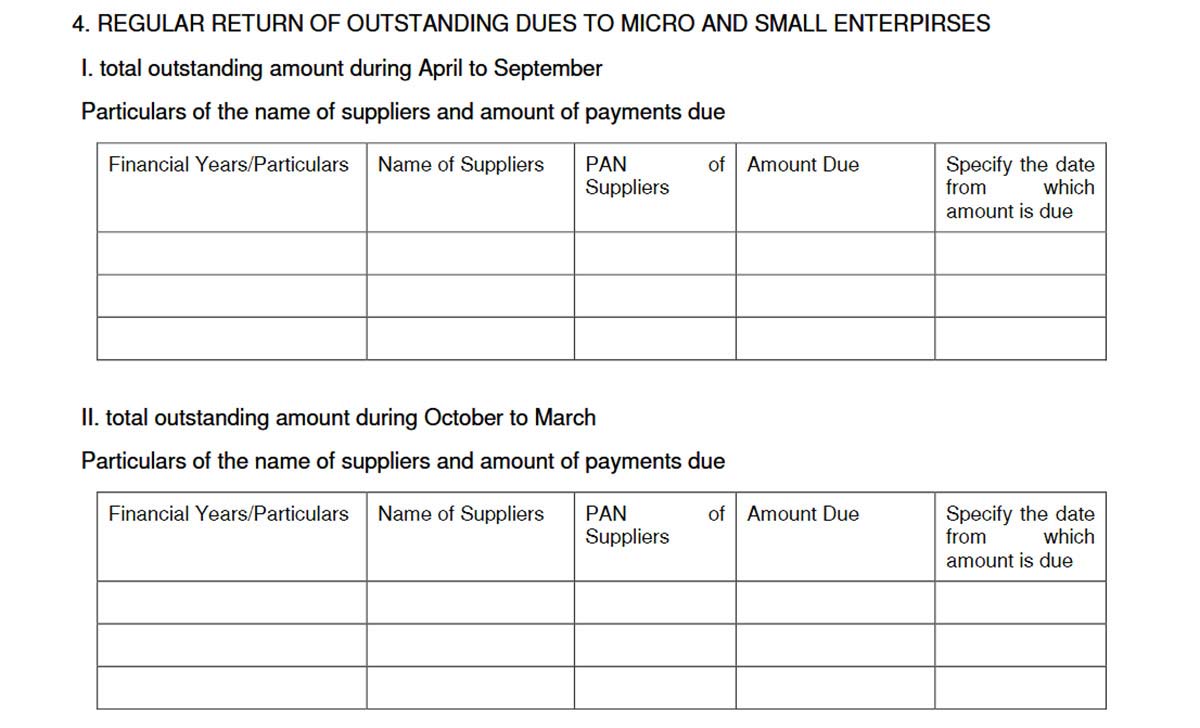

All the Companies falling under the above-mentioned category, would require to file MSME Form I as a half-yearly return by October 31st, for the period from April to September and later by 30th April for the period from October to March and must furnish the below details in it:

1) the amount of payment due and 2) reasons for the delay

Thus Concludingly, each Specified Company, public or private, that obtains goods and services from the small and micro-enterprise and whose payment is due with such micro and small enterprise suppliers for 45 days from the date of acceptance, shall be required to file MSME Form as a half yearly return every year.

Read Also: Free Download ROC Return Filing Software for Companies

Step by Step Procedure to File MCA MSME Form 1

Below are the details of the form:

Step 1: Company details such as Corporate identity number, global location number, and the PAN

Step 2: Basic details of the company such as name, address, email id

Step 3: Details like initial returns of outstanding dues to the MSE suppliers

Step 4: Details of regular returns of outstanding dues to the MSE suppliers

Step 5: Details based on the reason for the delay in the payment amount

Step 6: Any particular attachment for the validation

Then there is a declaration by the company director along with a digital signature

Due Date for Filing MSME Form 1 (MCA):

1. Initially (One time)

Every company is required to file MSME Form I within 30 days from the date of deployment of said E-form on the MCA portal (as extended by the MCA) furnishing the details of all the outstanding dues, to Micro or Small enterprises suppliers, existing on the date of notification of this order.

2. Thereafter The Half-yearly return

Every company is required to file the MSME Form I as half yearly return by 31st October, effective for the period from April to September and once again by 30th April for the period October to March every year, relating to the outstanding payments to MSMEs.

Who should not file the form? (Exemption to this rule)

This Rule applicable not for all the Companies but only for those Specified Companies whose payment to MSMEs suppliers exceed 45 days from the date of acceptance or deemed acceptance of the goods or services as per the provisions under section 9 of the MSME Development Act, 2006.

If the payment against supplier exceeds 45 days but the supplier/Creditors gives a declaration that they do not fell under the category of Micro or small Enterprises.

The government of India and GST Council has introduced the GST 2.0- A New Filing System in order to simplify the GST return filing process. The main reasons for the introduction of this new return filing mechanism, i.e., Goods and Service Tax 2.0, by the government include simplification of tax procedures, evade & control tax evasion, and increase compliance.

The full-scale launch of this new GST filing system is scheduled to be rolled out in a phased manner starting from April 2020. The trial run of the new GST filing system has already been started on July 2019.

The major highlights of this newly proposed GST system include the introduction of three new forms, i.e., GST RET-1 (Normal), GST RET-2 (Sahaj), and GST RET-3 (Sugam) for suppliers, and two annexure forms, i.e., GST ANX-1 and GST ANX-2. Under GST 2.0, the government has also proposed some changes related to uploading of the invoice, provisional credit, and amendment returns for the taxpayers.

To get regular updates, news and other key information about GST 2.0: New GST Return Mechanism, keep following SAG GST Portal.

MGT 7 is an electronic form that is allocated to all the companies by the Ministry of Corporate Affairs for filing details of their annual return. The Registrar of Companies uses to maintain this e-form via electronic mode and on the basis of the statement of correctness given by the company. It is a popular form among the companies which are required to file the form as per the norms and regulations of the ministry of corporate affairs.

Who Need to File the MGT 7 Form?

All the registered companies in India must file this e-form every year doesn’t matter if the company is private or public. The requirement of filing the Form MGT 7 by the company is for its annual return.

What if the Company does not File MCA Form MGT 7?

If any company does not file Form MGT 7 on time, it would attract a penalty of INR 100 per day as default. The levied penalty was remarkably increased in 2018. So, it should be a good approach to file an annual return in this form before the last date.

Download MGT 7 Form Format from MCA Portal

One can easily download the MGT 7 form from MCA portal under “Annual filing e-forms” category.

MGT 7 (MCA) Form Filing Fees

The fee for the filing of company annual return via MGT 7 is determined by the nominal share capital of a company. The MGT 7 form filing fee starts at Rs 200 for the company with Share Capital of less than 1,00,000. The fee amount increases with increase in the share capital of the company. You can find the complete list here. The company must pay this fee when filing the annual return MGT 7 with ROC. For the companies not having a share capital, the MGT 7 Filing Fee is Rs 200.

Nominal Share Capital

Normal Fee Applicable in Rupees

Less than 1,00,000

INR 200

1,00,000 to 4,99,999

INR 300

5,00,000 to 24,99,999

INR 400

25,00,000 to 99,99,999

INR 500

1,00,00,000 or more

INR 600

MGT 7 Form Late Filing Fees (MCA)

In case of delay in the filing of MGT 7 annual company return, a company is required to pay an additional fee as penalty along with the normal fee. For a delay of up to 30 days, the MGT 7 late filing fee is twice the normal fee. Its gets increased depending on the period of delay.

Period of delays

Fee applicable

Up to 30 days

2 times of normal fees

More than 30 days and up to 60 days

4 times of normal fees

More than 60 days and up to 90 days

6 times of normal fees

More than 90 days and up to 180 days

10 times of normal fees

More than 180 days

12 times of normal fees

What’s an Objective Behind Filing the e-Form MGT 7?

The Form MGT 7 is filed for annual return however it contains all the particulars as similar to appear in the closing of the financial year. These particulars hold details of :

Read Also: ADT-1 Form Due Date and E-Filing Documents for First Auditor

The registered office, primary business activities, details of its holding, subsidiary and associate companies

The shares, bonds and other securities and shareholding pattern of the company financial obligations of the company

The members and debenture-keepers along with changes associated with them since the end of the last financial year

The promoters, directors, key managerial personnel along with changes associated with them since the end of the last financial year;

Meetings of members or a class thereof, Board and its various committees along with attendance details

Payment of directors and principal managerial personnel;

Details of penalty or punishment imposed on the company, its directors or officers and facts of the composition of offences and appeals made against such penalty or punishment

The issues related to certification of compliances and disclosures as may be specified

It’s a Shareholding format Such different issues as needed in the form

Which are the Needed Attachments to File MGT 7 Form?

One can file this e-form by attaching the scanned copy of documents under the attachment head. This attachment section is provided at the end of the form which requires given below attachments including:

List of investors, debenture holders

Approval letter for augmentation of AGM

MGT-8 copy

Optional Attachment(s), if any

What is the Last Date for Filing MGT 7 MCA Form?

The company required to file the form MGT 7 within 60 days from the Annual General Meeting date.

The last date for conducting annual general meeting is on or before the 30th day of September after closing of every financial year.

Hence, the last date for filing of form MGT 7 is usually 28th of November every year.

Mentioned in the provisions of Section 92(1) of Companies Act 2013, every business operating in India (including One Person Company and small company) is obliged to prepare the annual report of the company’s business and present it to the authorities in Form MGT 7. MGT 7 is required by every business on the closing of every Financial Year i.e., 31 March.

The contents of annual return form MGT 7 include details of the company’s registered office, principal business activities, information about the company’s holdings and subsidiary firms, shareholding patterns, company’s members, debenture holders, indebtedness, etc.

Mentioned in Rule 11 of the Companies (Management and Administration) Rules, 2014, the annual return of the company in Form MGT 7 authorised by the company’s director is required to be submitted to ROC (Registrar of Companies) within the prescribed time period.

Mentioned Below Some FAQs Related to MGT 7 E-forms:

Q.1 – About the MGT 7 e-form?

The Company’s Annual Return form or MGT 7 form is required to be filed by every company. The form comprises of the company’s financial and non-financial details which are needed by the authorities.

Q.2 – Who needs to file an MGT e-form?

Every registered firm operating in Indian premises including One Person Company and small company are required to file Form MGT 7.

Q.3 – When does the form need to be filed?

Depending upon the situations of various companies there are different due dates of filing Form MGT 7:

Case 1 – In the case of One Person Company, e-form MGT 7 needs to be submitted to legal authorities within 60 days starting from the expiry of 6 months from the closing date of FY. For Example, if FY ends on 31 March 2019, then 6 months from the end of FY will complete on 30 September 2019. So the prescribed due date of filing MGT 7 is 28 November 2019 (i.e. 60 days from 30 Sept 2019).

Case 2 – In the case of company’s except OPC, MGT 7 needs to be filed within 60 days starting from the date of concluding the Annual General Meeting (AGM). If in case the company fails to conduct the AGM then also it needs to furnish MGT 7 Form along with the valid reason for not conducting the AGM.

Q.4 – How much fee is to be deposited along with Form MGT 7?

Mentioned below is the table presenting the amount which is to be paid to legal authorities along with form MGT 7:

Nominal Share Capital

Normal Fee Applicable in Rupees

Less than 1,00,000

INR 200

1,00,000 to 4,99,999

INR 300

5,00,000 to 24,99,999

INR 400

25,00,000 to 99,99,999

INR 500

1,00,00,000 or more

INR 600

To be noted: For the companies not falling under any of the above-mentioned criteria, the fees along with MGT form is Rs. 20.

Q.5 – What is the penalty for the late filing of MGT 7?

As declared by Companies (Registration Offices and Fees) Second Amendment Rules 2018, the late filing of form MGT 7 will invite penalty of Rs. 100 per day of delay counted from the expiry of the due date of filing MGT 7.

Q.6 – What is the aftermath of not filing MGT 7 within the prescribed time period?

If the company is found guilty of not filing MGT 7 within the designated time limit then the company along with its key officials will be liable for paying Rs. 50,000 as a penalty. However, if the delay continues then the penalty of Rs. 100 per day will be payable until the amount reaches the maximum of Rs. 5,00,000.

Q.7 – What documents are required along with form MGT 7?

List of documents needed adjacent to form MGT 7:

A list containing details of shareholders & Debenture holders – Applicable in the case when the company is having share capital and where the complete list of shareholders and debenture holders has been enclosed as an attachment.

Approval letter for extension of AGM, if applicable.

MGT-8 (if applicable)

Optional: MGT-8 is a certificate given by Company Secretary in practice where the company is listed or its paid-up share capital is INR 10 Crores or more or Turnover is INR 50 crores or more.

Q.8 – Whose signatures are required to authenticate MGT 7?

When OPC is concerned – the signature by the company secretary on Form MGT 7 is required and if there is no company secretary for the firm then the signature is required by the director of the company.

When companies other than OPC are concerned – Form MGT 7 needs signatures from the director and the company secretary of the firm, if there is no all-time company secretary then signature is required by the company secretary in practice.

To be noted: If any company found alleged of filing Annual Return which is contradicting the provisions of the ‘Companies Act’ then the company has to pay the fine of min Rs. 50,000 but not exceeding Rs. 5,00,000.

Q.9 – Link to download form MGT 7?

E-form MGT 7 is available to download from MCA’s official website.

Concussion

For all your filing related compliance for the MGT 07 for MCA, the SAG Infotech is readily available to cater you with the best of ROC/MCA filing software i.e. Gen CompLaw which is used by thousands of tax professionals across India. The Gen CompLaw is capable of minutes register and all the relevant ROC filing as per the due date and regulations

File MGT 7 Annual Return Form by Gen CompLaw XBRL Software