Tax officials propagated that the Income Tax Department has introduced a modification in the process of issuing refunds to the taxpayer. The department used to issue refunds to taxpayers either in their bank accounts or through account payee cheques, depending on the category of taxpayers. But from this assessment year, tax refunds will be issued only through e-mode, directly in the bank accounts of taxpayers which must be linked with their PAN.

Tax department comes up with this change with the motive of ensuring direct, abrupt and secure tax refund. Bank account linked with PAN is a pre-requisite for this. The bank account can be either savings, current, cash or overdraft.

Tax official while communicating with the public also added that taxpayers can make sure if their bank account is linked with their PAN by logging on to the e-filing website of the department: https://www.incometaxindiaefiling.gov.in

In case the PAN is not coupled with the bank account then taxpayers are required to link it by visiting their home bank branch followed by its validation over the income tax return e-filing website of the I-T Department.

If your bank is unified with the e-filing portal, pre-validation can be done easily & directly via EVC (Electronic Verification Code) and net-banking route. On the other hand, if your bank account is not integrated with the e-filing portal, then the income tax department will certify the bank account itself from the details filled up by you.

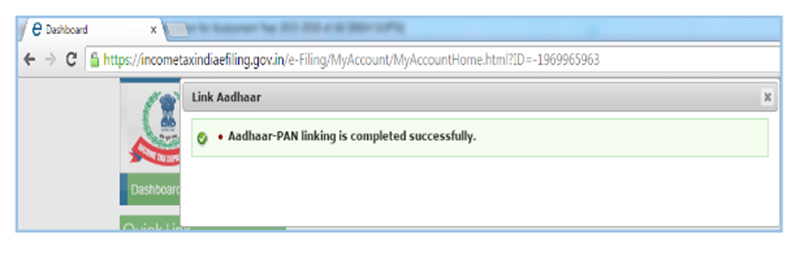

It has also become mandatory to link PAN with the Aadhar-PAN in order to file an ITR (Income Tax Return) and deadline for the same is 31st March 2019.

PAN is a 10-digit alphanumeric number allotted by the IT Department to a person, firm or entity. Aadhaar is assigned by the Unique Identification Authority of India (UIDAI) to an Indian resident, containing a 12-digit number generated on the basis of some factors like demographics and biometric data specific to each individual.

Aadhaar card is as significant as a PAN card for an Indian citizen

While updating the data at the beginning of this month, the I-T Department witnessed that only 23 crores PAN were linked with Aadhaar and the remaining 19 crores PAN are still needed to be linked.

An onset of Tax Audit spell is buzzing alarm for CAs to update their knowledge about different clauses of the Form 3CD and form a check list to move in tune with Tax officials.

C.A.s may prepare and follow a step-by-step procedure which is in compliant with the I.T. rules and regulations to stay in good books of Tax authorities and avert the circumstances to be penalised.

The main purpose behind the implementation of Tax Audit was to ease the troublesome and baffling assessment process for the tax authorities. A tax auditor is responsible for the verification of the details and responding to different clauses of 3CD in the most efficient way he can while ensuring accuracy and fairness.

It doesn’t matter whether an auditor or client or both get the data ready which is needed to accomplish the tax audit, the responsibility of the accuracy of the information presented in 3CD or annexures exists with the auditor inescapably, until & unless he doesn’t prove himself innocent or evidence that he has done the allotted assignment with ultra care and efficiency.

Here, we are not going to confer upon how tax audit is done but we shall know the consequences of furnishing incorrect details in tax audit/ Statutory reports or certificates. We shall know whether C.A. gets penalised or he bears no responsibility for that. So let’s move on with a simple question- Does C.A. hold any liability for furnishing wrong details in a tax audit by the assessing officer?

Section 271 J added in the act from April 1st. 2017 has the answer. Here, we have presented a brief study of the section:

Section 271J is about the penalty imposition on professionals for furnishing inaccurate or wrong information in a certificate or statutory report.

Without prejudice to the provisions of this Act, when the Assessing Officer or the Commissioner (Appeals), during any prosecution or proceedings under this Act, discovers that an accountant/ a registered valuer/ merchant banker has furnished incorrect or false information in any certificate or report issued under any provision of this Act or the rules formed under that, the Assessing Officer or the Commissioner (Appeals) may levy a penalty of INR 10,000 on such accountant/ registered valuer/ merchant banker for each such certificate or report.

Explanation with the Reference of Section 271J

“accountant” signifies an accountant referred to in the Explanation below sub-section (2) of section 288;

“merchant banker” refers to Category I merchant banker registered with the Securities and Exchange Board (SEBI) of India formed u/s 3 of the SEBI Act, 1992 (15 of 1992);

“registered valuer” refers to a person stated in clause (oaa) of Section 2, Wealth-tax Act, 1957 (27 of 1957).

The noteworthy points elicited from the definition of the act

The Chartered Accountant who has attested a certificate or report under the Income Tax Act must present before the assessing authorities to substantiate the rational reason behind the disappointing delivery of the results wherever it’s client assessment is under process. This may also involve travelling of C.A. from one city to another to get him/herself present before the assessing officer.

This section has been added from April 1st, 2017 but also takes into consideration the certificates and reports signed before this date.

This section begins with “without prejudice to the provisions of this Act”.

Key Considerations:

The penalty can be imposed on Chartered Accountant only by Assessing Officer or CIT(Appeal). No other authority has the right to levy this penalty.

As the section 271J is “without prejudice to the provisions of the Act”, if the C.A. is accountable to any other penalty or prosecution pursuits under the Act, he will continue to be responsible under those provisions.

The penalty can be imposed on if the proceedings conclude that information furnished was inaccurate or false.

Recommendations:

The Judicial elucidation of “without prejudice to the provisions of this Act” has been illustrated in the below-mentioned cases:

A.P. State Financial Corporation V. Gar Re-Rolling Mills, AIR 1994 SC 215

CIT v. Punjab National Bank [2001] 116 Taxman 310 (Delhi).

Wrapping up:

The ligature does not hold any intention to delay the processing of any request or submission made before any forum or department or court.

There is, without prejudice to the provisions of this Act, right to – try to resolve any issue by taking up parallel or alternative mechanism without any disruption or delay in the proceedings taking place at the same time regarding the same matter.

The importance of “without prejudice to the provisions of this section” is that the authority of the assessing officer to proceed u/s 143(2), even after the intimation u/s 143(1) (a), was perpetuated and wasn’t abducted. The process has not been shortened but preserved.

Implications Under the Rules of the Institute of Chartered Accountants:

A Chartered Accountant in practice who has been penalized by I.T. Department under section 271 J, can be castigated by the Institute of Chartered Accountants of India (ICAI) also on the ground of professional violation under the Chartered Accountants Act, 1949.

Penalty u/s 271J is leviable irrespective of the fact that penalty can/cannot be imposed on the associated assessee who also used the same false information.

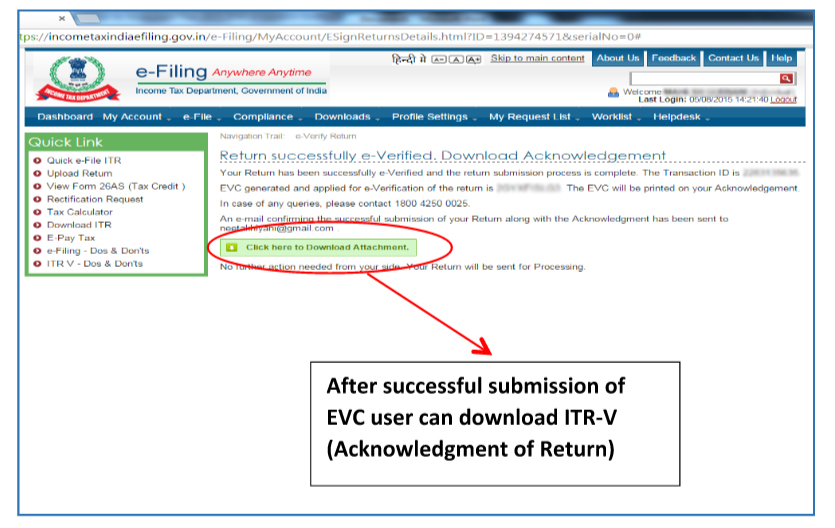

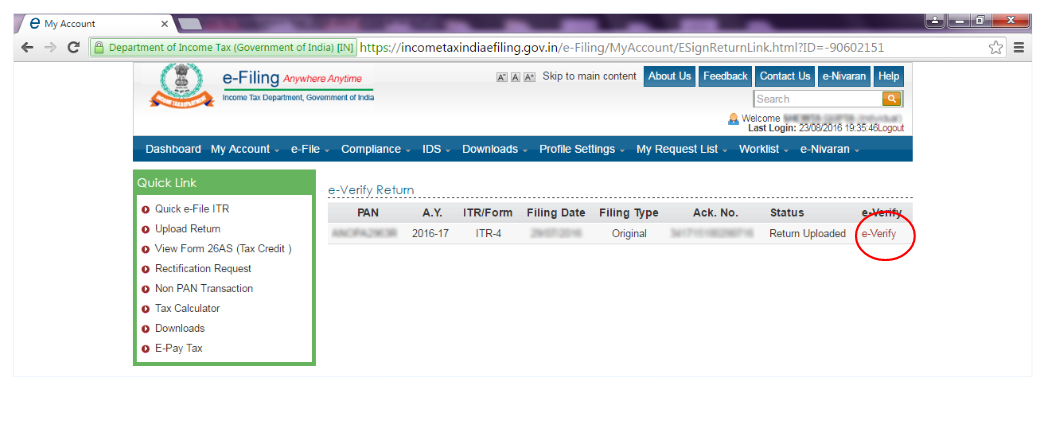

After uploading of return in electronic mode, a New functionality of electronic verification code (EVC) of the Income Tax return has been introduced vide Notification No. 2/2015, dated 13/07/2015. This facility can be used as an alternative for submission of ITR-V to CPC- Bangalore.

Mode and Process of Generating and Validating IT Returns through EVC

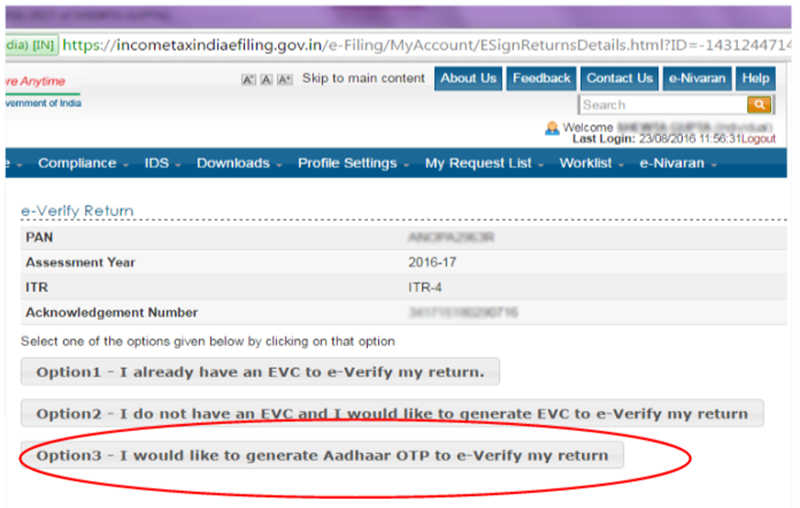

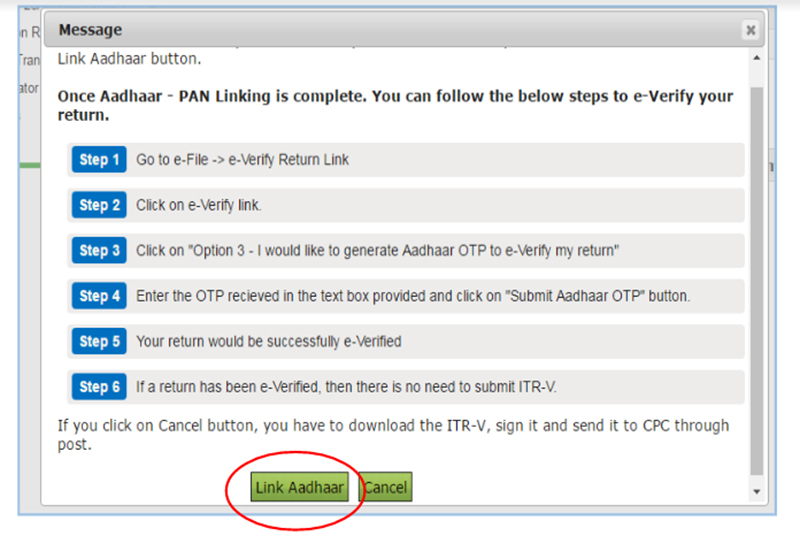

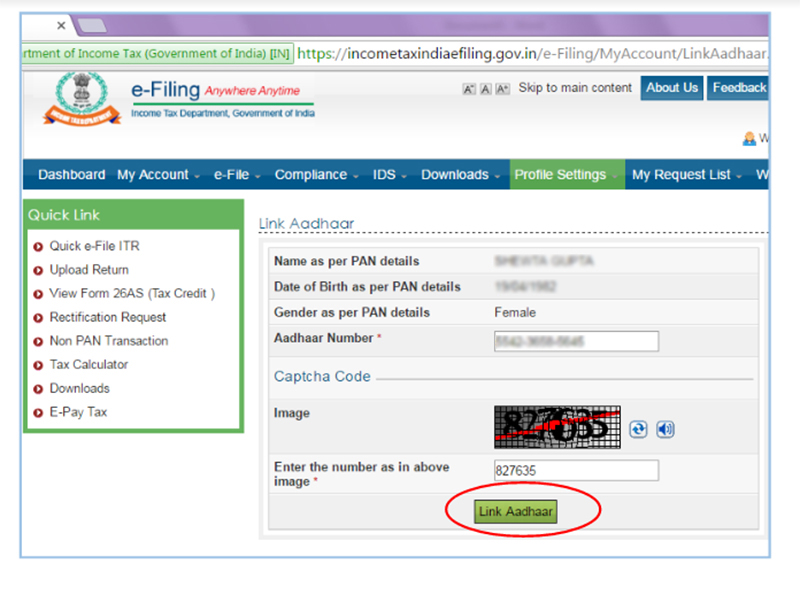

If the assessee has Aadhar Number then he has to link Aadhar No. by Clicking on “Profile Setting” on ITD portal and then click on Link Aadhar Card.

Step 1

Step 2

Step 3

Step 4

Step 5

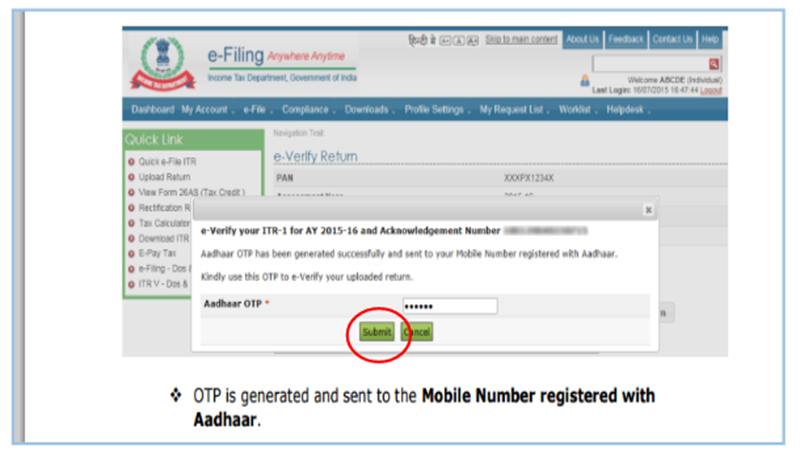

After successful linking of Aadhaar Number, you can e-verify your return through Aadhaar OTP

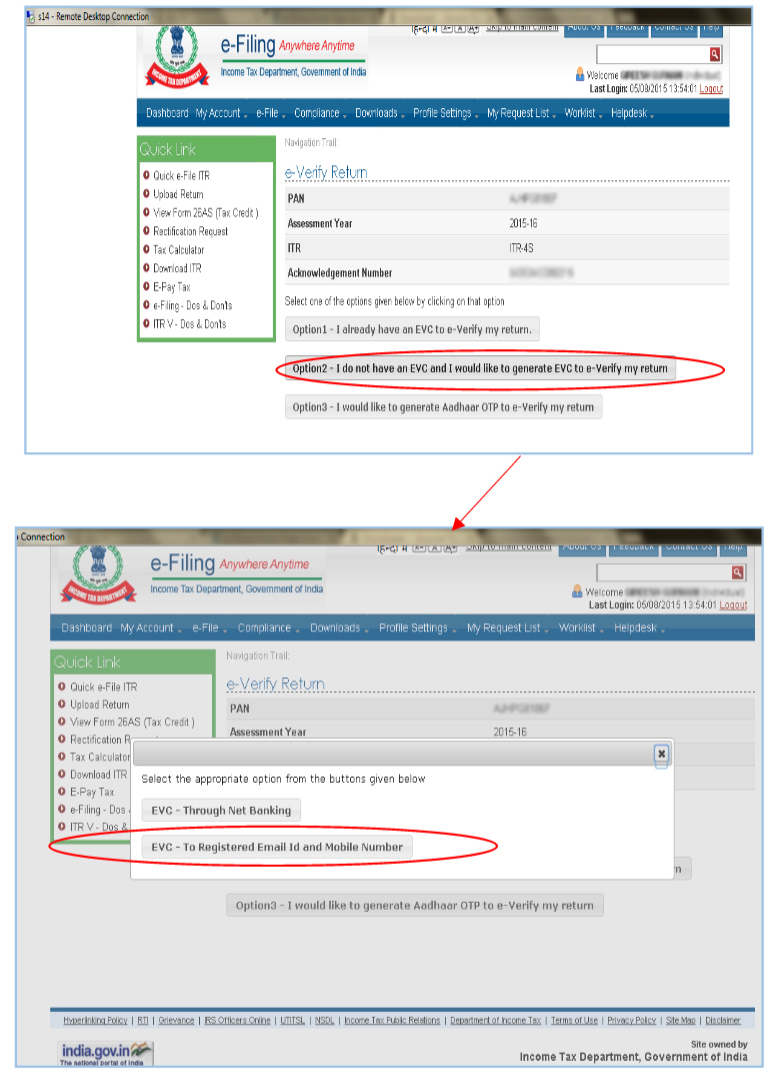

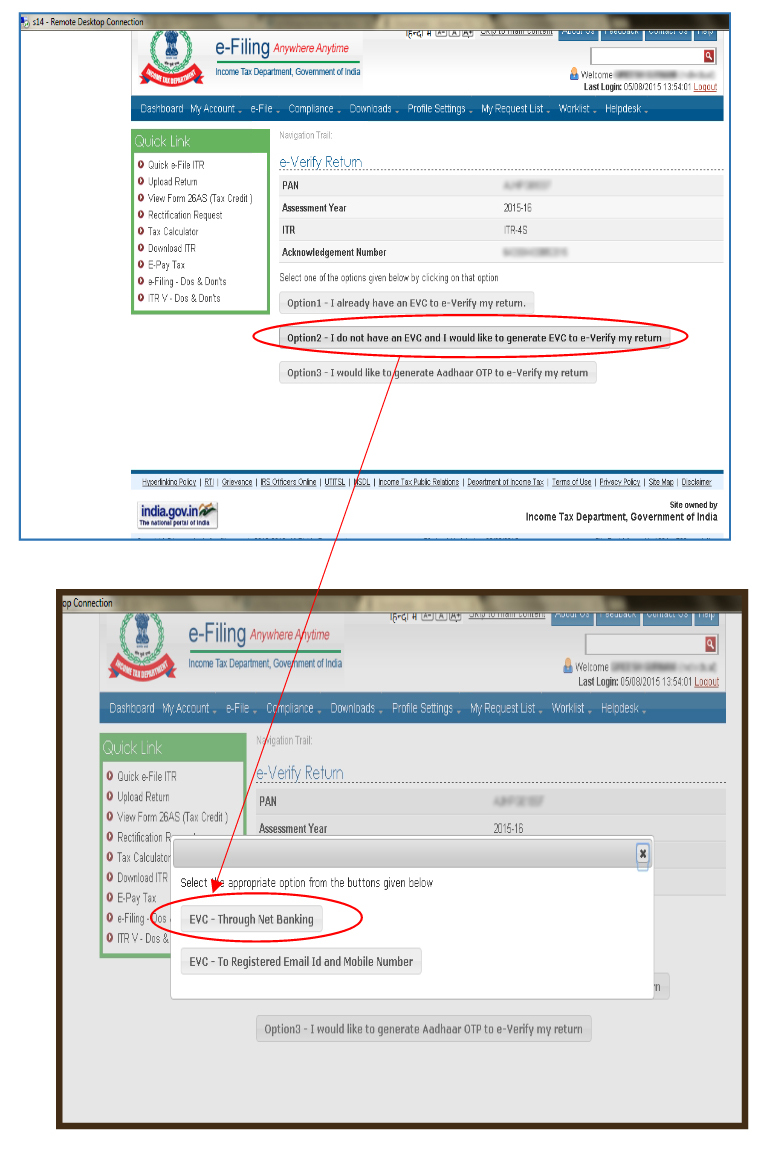

2. I do not have EVC and I would like to Generate EVC to e-Verify My Return

After uploading of return in electronic mode assessee has to choose an option from e-Verify drop-down option.

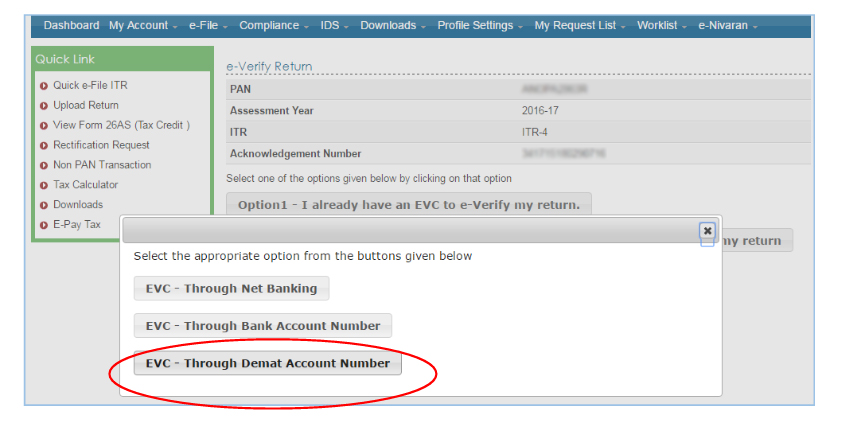

“I do not have an EVC and I would like to generate EVC to e-verify my return” by clicking on this option four modes will be available:

EVC —> Through Net banking

EVC —> To registered Email id and Mobile Number

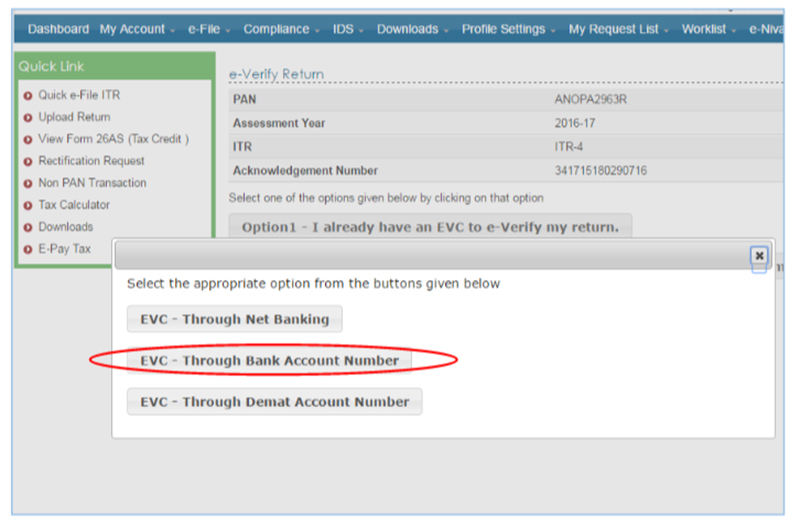

EVC —> Through Bank Account Number

EVC —> Through Demat Account Number

Note:

A) In case of refund claimed in uploaded return, the user can generate EVC through Internet banking not on registered Email Id and mobile No.

In Case Assessee’s Total Income is more than five lakhs Rs he will not be eligible to e-Verify his return through registered Email Id and mobile No

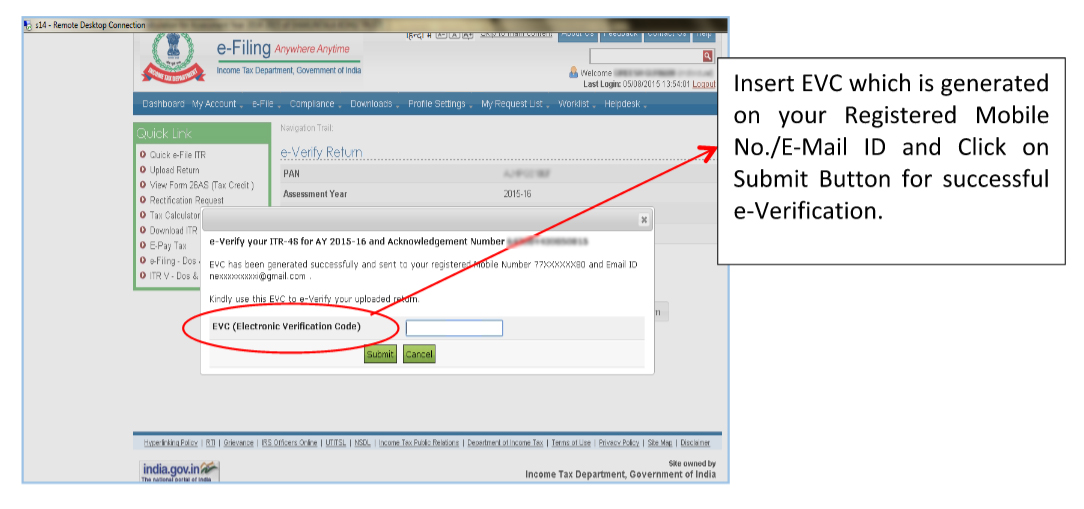

EVC —> To registered Email id and Mobile Number

After selecting this option a code will be sent by ITD to registered mail id and Mobile No. The assessee has to submit this code for e-verification.

After Submitting EVC, the user can download ITR Acknowledgment

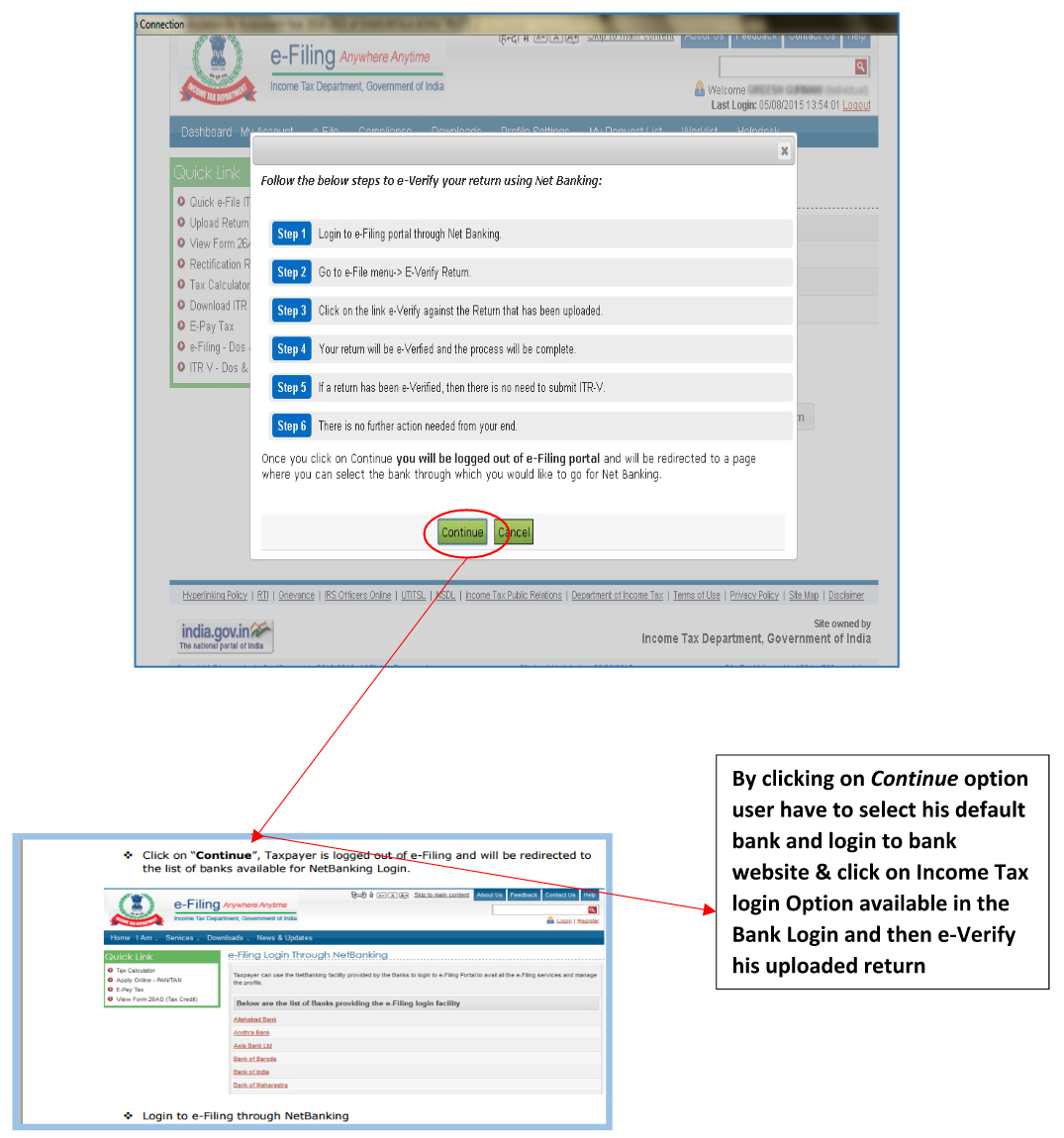

EVC —> Through Net banking

Step 1 —> Go to ITD Login —> View Return Form —> Click on e-Verify option

Step 2 —> By clicking on that option following screen will be appeared

Earlier there were only two options, EVC through Net Banking or EVC through Email Id and Mobile Number

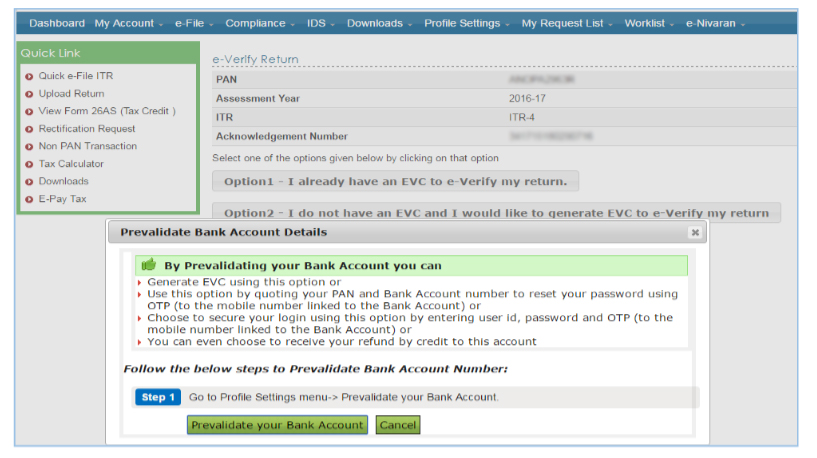

The Assessee who don’t have Internet banking facility can verify their return through Prevalidating Bank Account Number.

But for this function assessee must have the bank account in Punjab National Bank, State Bank of India, ICICI Bank or United Bank of India, then the only assessee can e-Verify return.

Generation of EVC through Bank Account Number

Step-1

Step-2

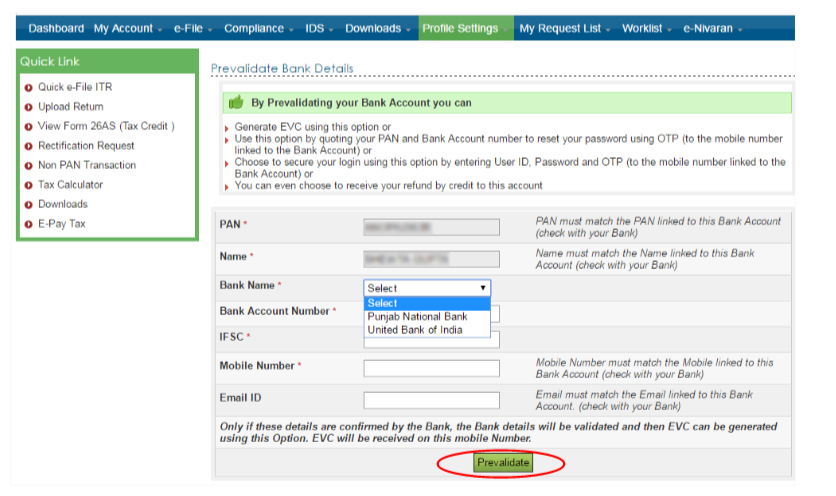

Step-3 —> Assessee have to fill all the required Details like Select Bank from the drop down box Fill account Number with IFSC code and Mobile Number and Email Id and click on Pre-validated Button

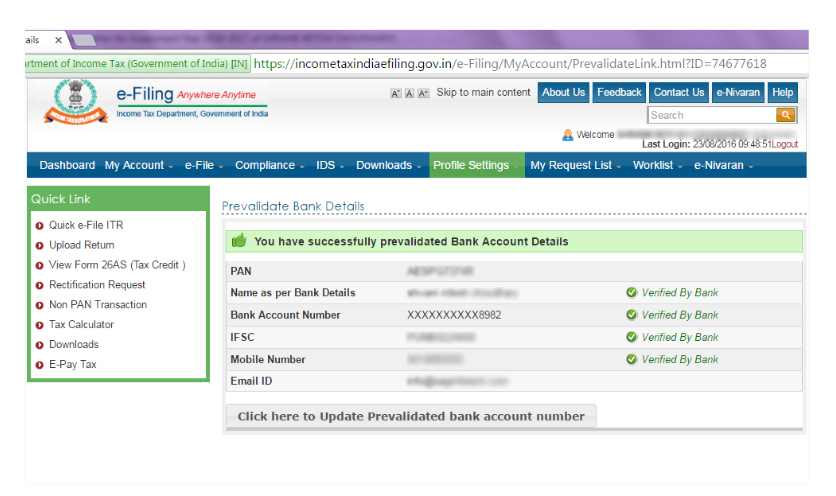

Step-4 —> Successful Pre-validation of Bank Account Number

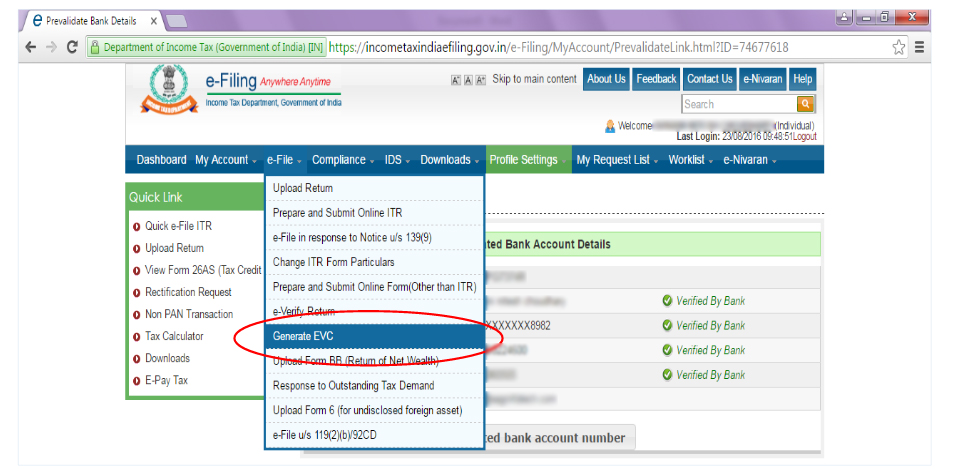

Step 5 —> Generation of EVC to e-verify ITR

After successful Validation of Bank Account Number, assessee have to click on Generate EVC option in e-file Menu of ITD login and he will get a code on his registered mobile Number. After furnishing code return will be e-verified by ITD.

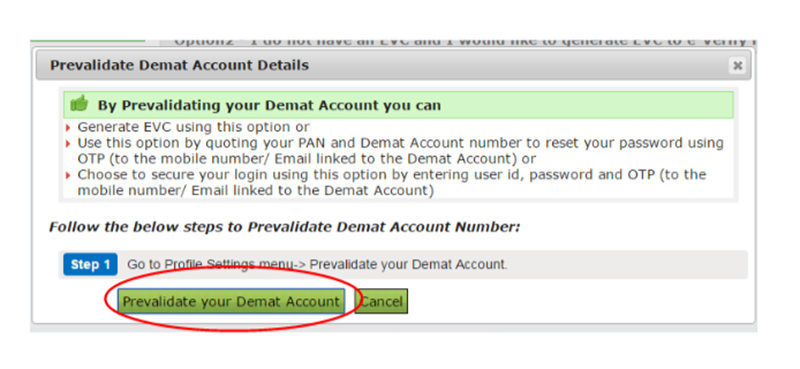

EVC generation Through Demat Account Number:

If you have Demat Account Number then you can use this facility to e-Verify your return.

For this function you have to follow such simple steps:

Step 1 —> Login to e-filling website –> Click on View Return Form and select e-verification option.

Step 2 —> Choose Generate EVC through Demat Account Number from available options.

The following screen will be available.

Step 3 —> After selecting Demat Account option user have to pre-validate his Demat Account Number

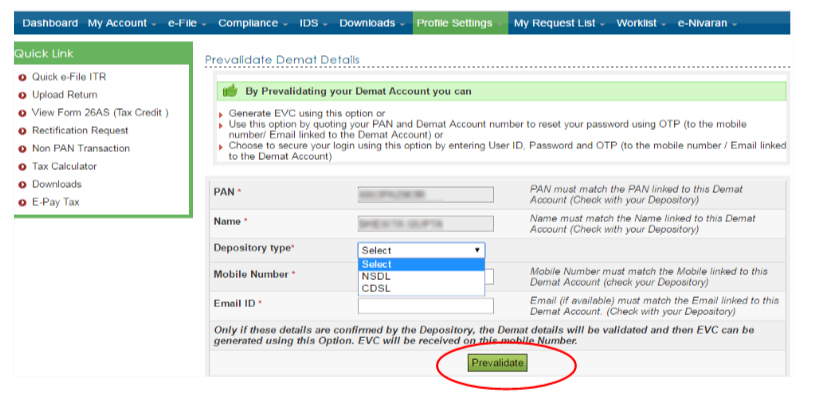

Step 4 —> Fill following particulars to verify your Demat Account Credentials and click on Pre-Validate option after submitting details user have to select Generate EVC like assessee has done in step-5 then return will be E-verified.

The Income Tax Department allows individuals to claim the refund for depositing extra tax. An individual can claim the same online using the Income Tax Department’s e-filing portal, www.incometaxindiaefiling.gov.in. Income Tax regulations mandate the Filing of income tax for individuals earning an annual income of Rs.2.5 lakh or more. For Senior citizens (individuals with age between 60-80 years) and very senior citizens (individual with age above 80 years), the limits are Rs.3 lakh and 5 lakh respectively.

Simple Steps to Claim the Income Tax Refund Online:

Step 2: Go to ‘My Account’ tab on the top left side of the screen near the ‘Dashboard’ tab and choose the ‘Service Request’ option. Select “New Request” under request type field and choose “Refund Reissue” as Request category

Step 3: All the refund failures for each AY will be displayed. Click on submit to request refund issue for a particular year.

Step 4: Fill in the details like Bank Account No., Account Type, IFSC Code, Bank Name and Address.

The refund will be credited to your bank account after successful processing.

Step 1: Log in to the Income Tax e-filing portal www.incometaxindiaefiling.gov.in with your user id, password and captcha.

Step 2: Go to ‘My Account’ tab and and click on “View e-filed Returns/forms”. You can check the refund status by clicking on acknowledgment number of relevant A.Y.

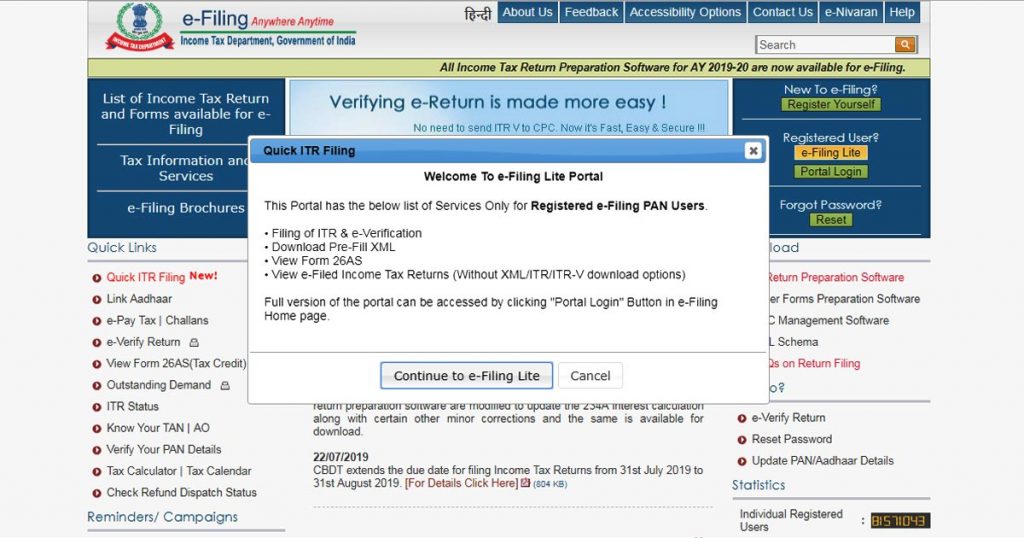

Taking a step towards the ease of the taxpayers, the Income Tax Department has launched E-filing lite services. This favourable approach by the tax government will prove to be of great help for taxpayers in e-filing of returns. The feature is initiated on the link www.incometaxindiaefiling.gov.in. Tax Authority says, “the department is glad to inaugurate e-lite filing which is the easy version of online ITR filing and will attract more taxpayers on the portal”.

To access the e-lite feature one may click on the ‘e-lite button‘ flashing on the homepage of the website. E-filing portal has a login button on the homepage to facilitate all the services. The tax official says “the new tab for lite is provided on the e-filing website which will direct the registered taxpayer to only the valid links of ITR and Form 26AS after login. The taxpayer can also file his/her previous returns and easily download XML format files.”

He further stated that e-lite edition is exclusive to make ITR Filing easy and is immune from other settings such as e-proceedings, e-exemptions, compliance, schedule and profile settings. However, these options are available in the standard edition.

The last date of filing ITR for FY 2018-19 has been extended by the government from earlier 23rd July 2019 to current 31st August 2019. Taxpayers who have not filed the ITR yet can still file the return by 31st August from the respective e-filing portal or by using lite services.

To be noted: The lite version of e-filing has fewer features than the standard version.

In July 2019, the central and state governments managed to collect the revenue of INR 1,02,083 crore as Goods and Service Tax (GST). Comparatively, it is 5.8% more over the similar month last year, as described from an official.

In the current fiscal, it is the third chance when the combined central and state GST collection crosses INR 1 trillion milestones. There is an agreement between the central and state government if the GST collection of states accounts below a fixed 14% annual growth every year, the union government has the responsibility of compensating shortfall in revenue, within the first five years of GST regime. Collected revenue in July is the result of transactions made in June. In April 2019, the government recorded an annual growth of 10 per cent in GST collection, post which it remains low at 6.6 and 5.8% in subsequent months.

The GST collection of INR 1.02 trillion in July 2019 is the contribution of INR 17,912 crore from the union government, INR 25,008 crore from states, INR 50,612 crore from Integrated GST (IGST) on inter-state sales and INR 8,551 crore from the GST cess. For the revenue shortfall in FY19 and the growth rate remained below 14% till now in FY20, kept the central government busy in compensating states and a question arises how would be the state revenue position will be handled if the trend continues. The average collection of combined central and states was INR 93,114 crore monthly in last fiscal against an INR 1 trillion target of monthly.

In case if this shortfall remained to continue, the union government has to find new resources for compensating states revenue shortfall. Likewise collection from cesses and surcharges on several other taxes.

The Controller General of Accounts (CGA), the governments internal auditor, revealed the total tax revenue of central government in the June quarter registered a growth of 2.7% to collect INR 1.86 trillion as against to similar time duration last year.

The due date for filing ITR for AY 2019-20 is down the pike. Taxpayers are compiling various documents to file an ITR with correct figures. Most of the businessmen have hired professionals and purchased taxation & accounting software for e-file ITRs effortlessly and errorlessly. Salaried individuals are also under an obligation to file ITRs by using Form 16. Form 16 is not only a basic document but an ad hoc for the salaried individuals for filing the income tax returns (ITR). Filing an ITR without Form 16 is beyond the bounds of possibility for salaried individuals.

In a few cases, salaried individuals do not get Form 16 for a specific year. The reason for the same can be shut down of the business by the employer, termination from a job before the time mentioned in the bond, or job change without completing the exit formalities. In such cases when the salaried individual so not have Form 16, he/she needs to give many other documents as reference or endorsement to e-filing Income tax return.

Here we are presenting a step-by-step guide for salaried people to e-file an ITR in without Form 16.

Step 1: Computation of Income From Salary

Salary slips are the major source of information for the calculation of income from salary. Make sure to acquire monthly pay-slips from all the HR managers or employers of the organization you have worked for in the year. For this year as well, you will need to present the entire break-up of your income from salary.

Income from salary includes Gross salary (Salary in accordance with Section 17(1), Value of Perquisites, Profit in lieu of Salary, Allowances exempt u/s 10, Standard Deductions – Deductions u/s 16, Entertainment allowance (only for government employees) and Professional tax.

Salary slips are the major source of information for the calculation of income from salary. Make sure to acquire monthly pay-slips from all the HR managers or employers of the organization you have worked for in the year. For this year as well, you will need to present the entire break-up of your income from salary.

Income from salary includes Gross salary (Salary in accordance with Section 17(1), Value of Perquisites, Profit in lieu of Salary, Allowances exempt u/s 10, Standard Deductions – Deductions u/s 16, Entertainment allowance (only for government employees) and Professional tax.

Generally, salary slips have all the figures except the amount of profit in lieu of salary and the value of perquisites as in many instances, the company does not furnish these figures in salary slips. So in such cases, one may request the HR or finance department to issue Form 12BA – The form which constitutes the details of the value of perquisites and amount of profit in lieu of salary given to the employee by the employer.

In addition to the information stated above, the salary slips contain the amount of all the allowances paid to the employee, tax deducted at source (TDS), the amount deducted towards provident fund (PF), etc.

Some Beneficial Points in this Regard:

Ensure to use the allowances that reduce your tax liabilities such as LTA, HRA, etc.

Compute the allowances, well-considering the partially exempt and fully exempt allowance.

Mention the tax-exempted allowances in ITR.

Avail the standard deduction of Rs 40,000 u/s 16 (ia) for the present year.

Step 2: Reconcilement of the deducted TDS with Form 26AS

Form 26AS encompasses the complete information of the TDS which is deducted on the salary income as well as on other incomes. So, the TDS amount present in the Form 26AS should not be matched with the individual sources such as salary slips for the TDS deducted on salary, TDS/interest certificate for TDS on fixed deposits (FDs), etc. However, the number of TDS deducted should be cross-checked with the TDS figures shown in Form 26AS. In case of any mismatch, the salaried individual should get in touch with the specific deductor.

Step 3: Computation of Income From House Property

The income generated from letting the house property on rent comes under this head. When you give a house owned by you on rent, the income which comes as rent is termed as rental income. And if you have availed any house loan on the property which you have given on rent or self-occupied property and you are paying interest on that house loan, then the deduction of the same can be availed and comes under this head.

Further, when an individual is an owner of two or more houses, he/she first needs to review the deemed let-out factor. If the individual is the one who is generating the rental income, then he/she is eligible to avail a flat deduction of 30 percent along with deduction of municipal tax from his/her rental income (if paid any).

Step 4: Computation of Income From Capital Gains

For computing the capital gains, an individual should get a summary statement from his/her broker for the gains from the sale of equities or equity-oriented mutual funds and should get the purchase and sale deed ready for the gains from the sale of land or building. The capital gain is exempt up to the limit of Rs. 1 lakh if it is held for a period exceeding a year and was sold out in FY 2018-19.

Note: One Can Not File a Tax Return Using ITR-1 When:

A) He/she has sold equity mutual funds and/or equity shares in FY 2018-19;

B) He/she is the owner of more than one house property.

C) He/she is holding investments in unlisted shares;

In the above-mentioned cases, an individual must e-file online ITR-2 or ITR-3.

Step 5: Computation of Income From Other Sources

Income from other sources constitutes the income earned as interest on various bank deposits such as FDs, savings, recurring or term deposits and interest on income tax refund, etc.

For this, one can consider his/her bank passbook which showcases the interest income and Form 26AS which displays interest on an income tax refund.

Note: This year an individual needs to state the source of interest income also from the drop-down menu which is present in the ITR form.

Step 6: Claim All The Deductions

Section 80C and 80D of the Income Tax Act provides various deductions for the individuals. Deduction for the PF, Life insurance, Equity-linked savings schemes, principal repayment of home loan etc can be claimed along with appropriate evidence u/s 80C, while deductions like medical insurance premium can be claimed u/s 80D.

The stated limit up to which a deduction under section 80C can be claimed is up to Rs 1.5 lakh. Similarly, other deductions also have prescribed limit up to which it can be availed.

Step 7: Calculation of Total Taxable Income

This is near to the final step in which the deductions are subtracted from the total income generated from various sources to get the final figure which is the total taxable income.

Step 8: Calculation of Income Tax Liability

Now the income tax liability applicable to the total taxable income is ascertained. It can be calculated with the use of an income tax calculator.

Step 9: Pay Additional Tax (if any)

When the total tax liability comes out to be more than the amount of tax already paid following the Form 26AS, then the remaining tax liability which is the additional obligation should be paid to the IT department.

Step 10: e-File Your Income Tax Return

This is the final destination to e-file an income tax return in the absence of Form 16. Make sure to e-verify it within the time-frame of 120 days of filing.

Wrapping Up: Although Form 16 is a prerequisite for a salaried individual to file an ITR, there is another way to file ITR when Form 16 for the year is not available with you. For that, you just to have the above-mentioned documents and follow the above mentioned step-by-step process. Keep in mind the due dates for filing ITR online and defend paying late filing fees u/s 234F for ITRs.

This ‘One Nation One Tax’ regime was initiated for the first time in the nation on 1 July 2017 and has completed 2 years of existence. Even after two years, GST governance lacks a definite blueprint of input tax credit system (ITC) says CAG reports. Not only this, the digitized e-tax filing system is still a tedious task for the fillers, said reports on the desks of the Parliament. No doubt, GST was introduced in the nation with good intentions but now the system has become exposed to ITC frauds.

The current GST compliance arrangement cannot work without proper invoice matching procedures, auto-generation of refunds and tax assessments, etc. the initiative has to be taken by the concerned authority to alter the prevailing scenario of tax compliance in the country. The key players of the tax system such as Department of Revenue (DoR), Central Board of Indirect Taxes and Customs (CBIC) and GSTN must co-ordinate and bring GST tax compliance to proper functionality.

In a written statement, Minister of State for Finance Anurag Thakur replied to the parliament saying, tax authorities have unveiled tax frauds worth Rs 45,682.83 crore under GST in last 2 years.

As per the data extracted from the government’s desk, Rs 6520.40 crore fraud was identified in the April to June period of the financial year 2019-20. In the last two years, the total number of 9,385 cases of GST frauds were brought to the limelight. GST rising under BJP-led governance is undoubtedly a promising tax structure, but it still needs more rigidity and applicability.

Permanent Account Number (PAN) is marching forward towards becoming an inevitable number for any transaction or deal made by an individual. Time is approaching when there is a need to link all the transactions with the Income Tax Department through PAN.

PAN basically assists the tax authorities in identifying an individual or a corporate body which is getting into a deal or making a transaction. Transactions may be a tax payment, money withdrawal, cash deposition or encashment of amount deposited in the bank for any deal.

Budget 2019 has proposed some changes and inclusion in the current PAN associated rules and provisions. We are highlighting the four most important of them which one must be acquainted with.

Here we go for the new PAN related norms which will become effective post the Budget 2019 announcement:

Effect of Not linking PAN with Aadhaar

At present, u/s 139AA (2), the PAN issued to an individual shall be considered ‘invalid’, if the individual is unsuccessful in intimating the Aadhaar number. However, when a person is unsuccessful in intimating the Aadhaar number and fails to link PAN with Aadhaar, the PAN card will deem to be inoperative.

Note: 30th September 2019 is the due date to link PAN with Aadhaar.

As per Budget 2019, the word ‘invalid’ will be replaced with ‘Inoperative’, on 1st September 2019.

Equivalence of PAN and Aadhaar for ITR Filing

For filing of ITR, a PAN linked with Aadhaar is an ad hoc. But in cases when someone doesn’t hold a PAN, Budget 2019 has proposed to permit the use of Aadhar number in place of PAN. According to the proposal, any person who needs to quote his PAN under the legal section but he doesn’t have any PAN and possesses only the Aadhaar number, may furnish or quote the Aadhaar number in place of PAN. PAN will be issued to the person based on Aadhar details.

Involuntary Quoting of PAN in Statutory Stated Deals

Having PAN is indispensable in some cases like when the income of an individual exceeds the basic exemption limit, when ITR has to be filed or when the turnover of a business exceeds Rs 5 lakh. In other cases, PAN is not mandatory.

However, the government has been witnessing that in multiple instances when people are engaging in high-value transactions like the purchase of foreign currency or withdrawal of hefty amount from the banks, they do not hold a PAN.

So to keep an audit record of these transactions and for expanding the tax base, Budget 2019 proposed to add a new clause (vii) in section 139A (1) which makes it makes it mandatory for every person, who is willing to enter into some statutorily stated deals and do not hold a PAN, to apply for a PAN allotment.

TDS Deduction for Professional Service

As per the new Permanent Account Number (PAN) rule, you will need to deduct the TDS before making payment when you appoint a professional contractor, designer or an architect for the construction or renovation of your home. The new rule counts in any professional service availed for personal purpose, so now the TDS has to be deducted before making the payment for such professional service and deposited with the government using the professional’s PAN. At present, TDS need not be deducted when payment is made for professional services availed for personal use.

Further, if the individual is engaged in business or profession which is not accountable for audit, there is no need to deduct TDS even when the payment is made business or profession purpose.

However, the government realised that because of this exemption, a good amount of monetary payment made by individuals for the professional service or the contractual work creates a loophole for levying TDS which leads to tax evasion.

So to seal this escape, Budget 2019 has proposed to include a new section 194M in the Act to levy 5% TDS on the amount paid for the contractual work or professional services by a person if such amount goes above Rs 50 lakh in a year.

At the same time to lessen the compliance, it is also proposed that such persons will be needed to acquire the Tax deduction Account Number (TAN) and will be allowed to deposit the tax deducted with their PAN and the PAN of professional.

These are the mutation which will be introduced in the rules and regulations which are related to PAN. It is always advantageous to be on board with the upcoming changes so that it will not feel like clash on later dates when they will finally step on the legal paths. Further penalties and mistakes can be averted easily if you move parallel with the latest notifications and norms.

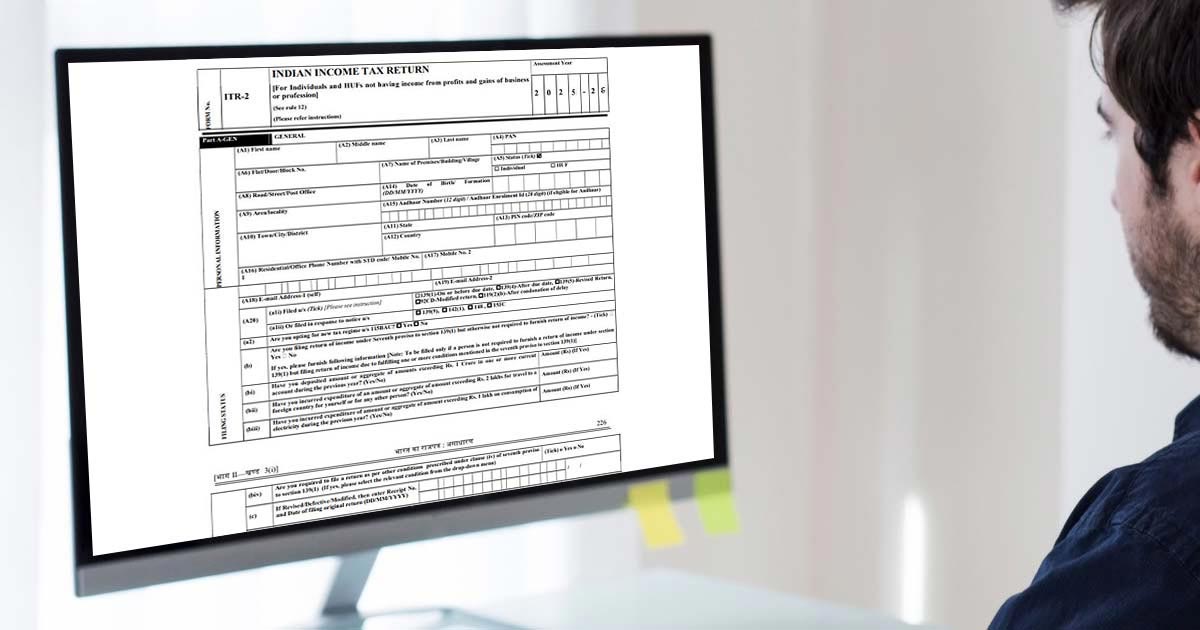

The ITR-2 is filed by the individuals or HUFs not having income from profit or gains of business or profession and to whom ITR-1 is not applicable. It includes income from capital gains, foreign income or any agricultural income more than Rs 5,000.

Eligible Taxpayers for Filing ITR 2 Online AY 2019-20

The taxpayers who are eligible for filing ITR-2 form are the persons whose source of income is as mentioned below:

A resident having any asset located outside India or signing authority in any account.

A non-resident or not-ordinary resident.

Taxpayers who earn agriculture income above Rs. 5000/-.

Income from winnings of a lottery, horse race, gambling, etc. under the head of other sources.

Both short and long-term capital gains/losses from the sale of property/investments/securities. (if there is only long term capital gain exempt u/s 10(38) then ITR-1 can be filed)

The taxpayers who do not require to file ITR-2 form are as follow:

Every year on or before 31st July is termed as the last date for filing ITR 2 (Non-audit cases). Note: The IT department has extended the due date till 31st August 2019. Notification here

Structure of ITR 2 Filing for AY 2019-20 Online

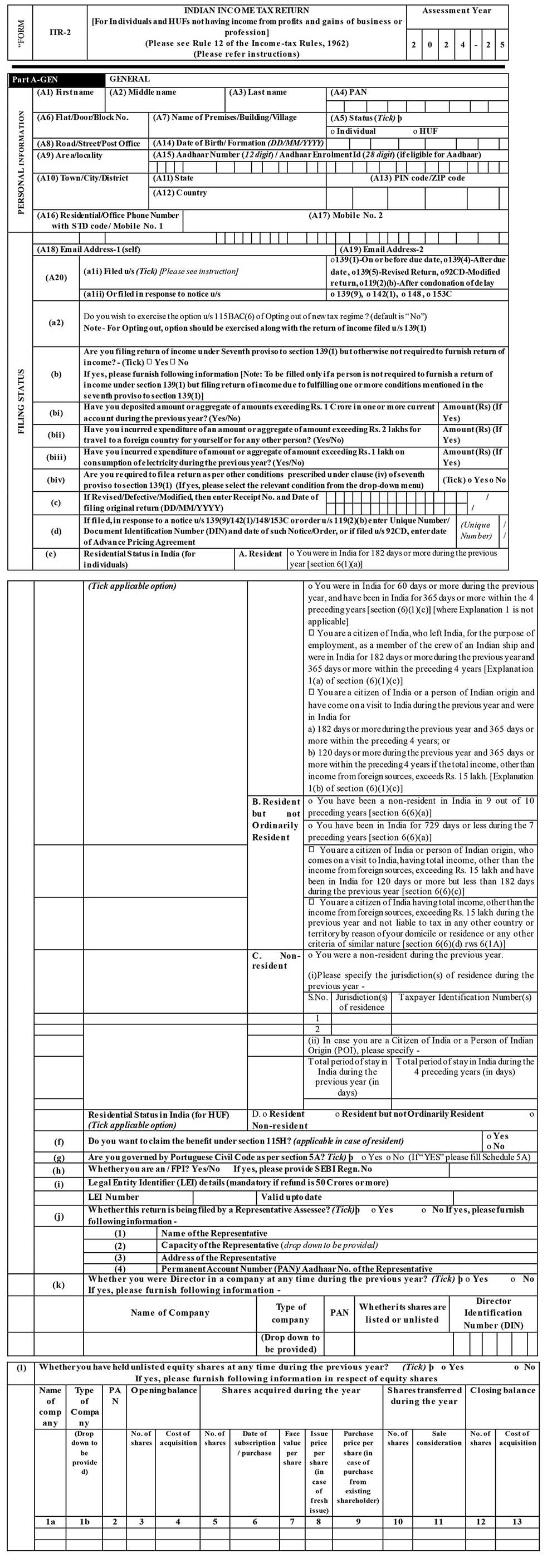

Part A: General Information

The general information is enclosed with the following details of the taxpayer to furnish with:

Name

Address

DOB

PAN number

Aadhar number

Contact Number

Email Address

A – Filed u/s 139(1)-On or before the due date, 139(4)-After due date, 139(5)-Revised Return, 92CD-Modified return, 119(2)(b)-after condonation of delay.

Or

Filed in response to notice u/s 139(9), 142(1), 148, 153A 153C

B – If revised/defective/modified, then enter Receipt No. and Date of filing an original return (DD/MM/YYYY)

C – If filed, in response to a notice u/s 139(9)/142(1)/148/153A/153C/119(2)(b) enter the date of such notice/order, or if filed u/s 92CD, enter the date of advance pricing agreement

D – Residential Status in India (for individuals)

E – Do you want to claim the benefit under section 115H? (applicable in case of resident)

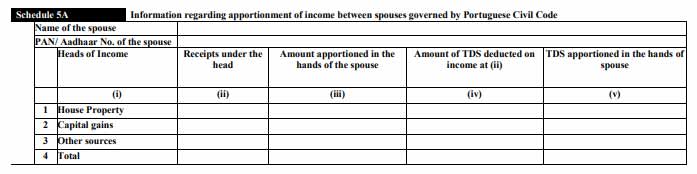

F – Are you governed by Portuguese Civil Code as per section 5A?

G – Whether this return is being filed by a representative assessee? If yes, please furnish following information –

Name of the representative

The capacity of the Representative (drop down to be provided)

Address of the representative

Permanent Account Number (PAN) of the representative

H – Whether you were Director in a company at any time during the previous year?

I – Whether you have held unlisted equity shares at any time during the previous year?

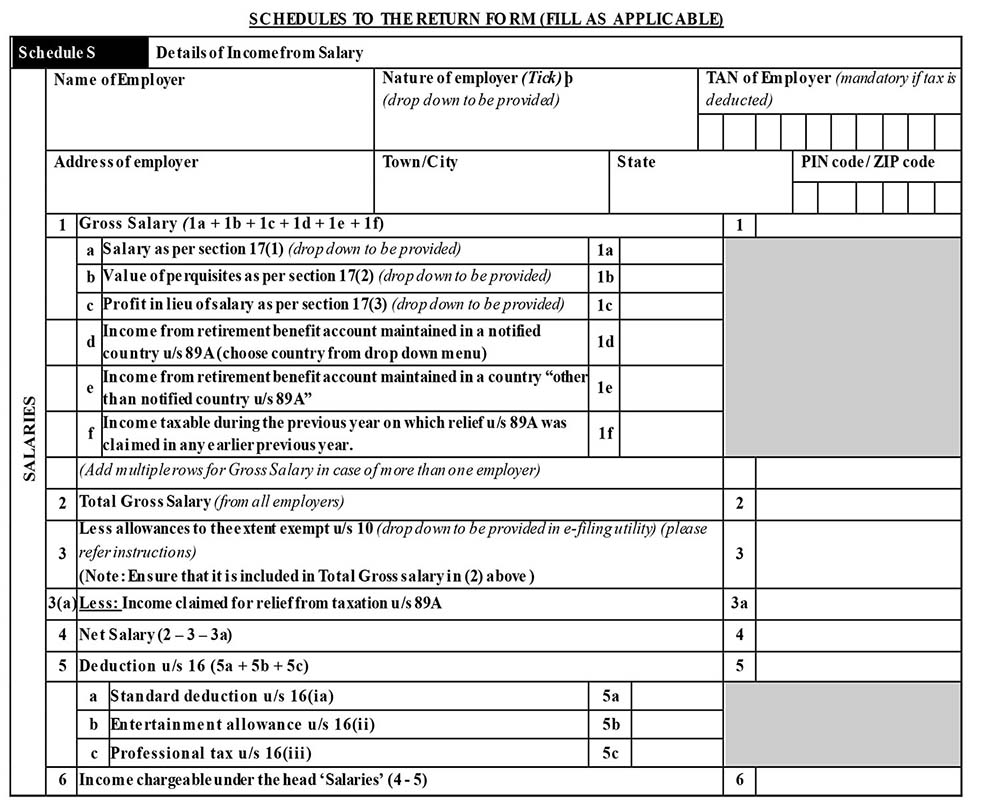

Schedule S: Details of Income from Salary

The information regarding Details of Income from Salary is enclosed with the following details of the taxpayer to furnish with:

Name of Employer

Address of employer

Gross Salary (excluding all allowances and perquisites and profit in lieu of salary)

Allowances not exempt

Value of perquisites

Profits in lieu of salary

Deduction u/s 16

Income chargeable under the Head ‘Salaries’

Schedule HP: Details of Income from House Property

The information regarding Details of Income from House Property is enclosed with the following details of the taxpayer to furnish with:

Address of property 1:

a – Gross rent received or receivable or letable value

b – The amount of rent which cannot be realized

c – Tax paid to local authorities

d – Total (1b + 1c)

e – Annual value (1a – 1d)

f – Annual value of the property owned (own percentage share x 1e)

g – 30% of 1f

h – Interest payable on borrowed capital

i – Total (1g + 1h)

j – Arrears/Unrealised rent received during the year less 30%

k – Income from house property 1 (1f – 1i + 1j)

Address of property 2:

a – Gross rent received/ receivable/ letable value

b – The amount of rent which cannot be realized

c – Tax paid to local authorities

d – Total (2b + 2c)

e – Annual value (2a – 2d)

f – Annual value of the property owned (own percentage share x 2e)

g – 30% of 2f

h – Interest payable on borrowed capital

i – Total (2g + 2h)

j – Arrears/Unrealised rent received during the year less 30%

k – Income from house property 2 (2f – 2i + 2j)

Pass through income if any *

Income under the head “Income from house property” (1k + 2k + 3)

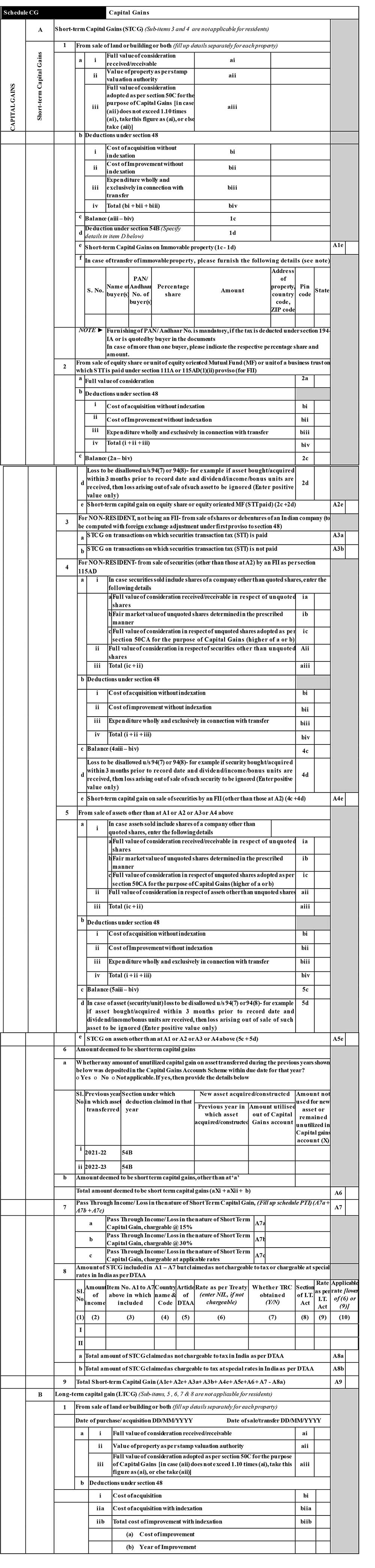

Schedule CG: Capital Gains

The information regarding Capital gains is enclosed with the following details of the taxpayer to furnish with:

A. Short-term Capital Gains (STCG)

1. From the sale of land or building or both

a

i Full value of the consideration received/receivable

ii Value of property as per stamp valuation authority

iii Full value of consideration adopted as per section 50C for the purpose of Capital Gains [in case (aii) does not exceed 1.05 times (ai), take this figure as (ai),

b – Deductions under section 48

i Cost of acquisition without indexation bi

ii Cost of Improvement without indexation bii

iii Expenditure wholly and exclusively in connection with transfer biii

iv Total (bi + bii + biii) biv

c – Balance (aiii – biv) 1c

d – Deduction under section 54B (Specify details in item D below) 1d

e – Short-term Capital Gains on Immovable property (1c – 1d) A1e

f – In case of transfer of immovable property,

2. From the sale of equity share or unit of an equity oriented Mutual Fund (MF) or unit of a business trust on which STT is paid under section 111A or 115AD(1)(ii) proviso (for FII) 3. For NON-RESIDENT not being an FII- from the sale of shares 4. For NON-RESIDENT- from the sale of securities 5. From the sale of assets other than mentioned above 6. Amount deemed to be short term capital gains 7. Pass-Through Income in the nature of Short Term Capital Gain 8. Amount of STCG included in A1 – A7 but not chargeable to tax or chargeable at special rates in India as per DTAA 9. Total Short-term Capital Gain

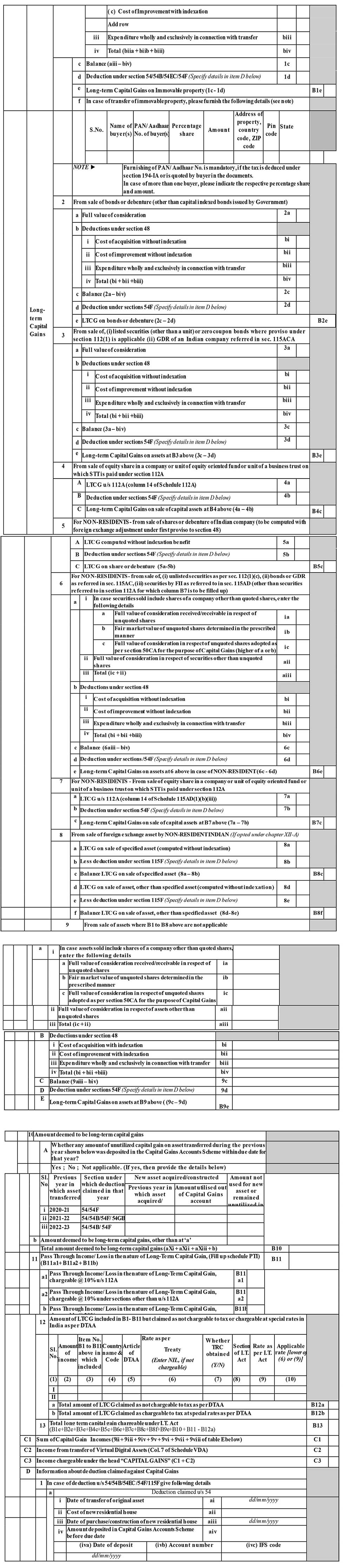

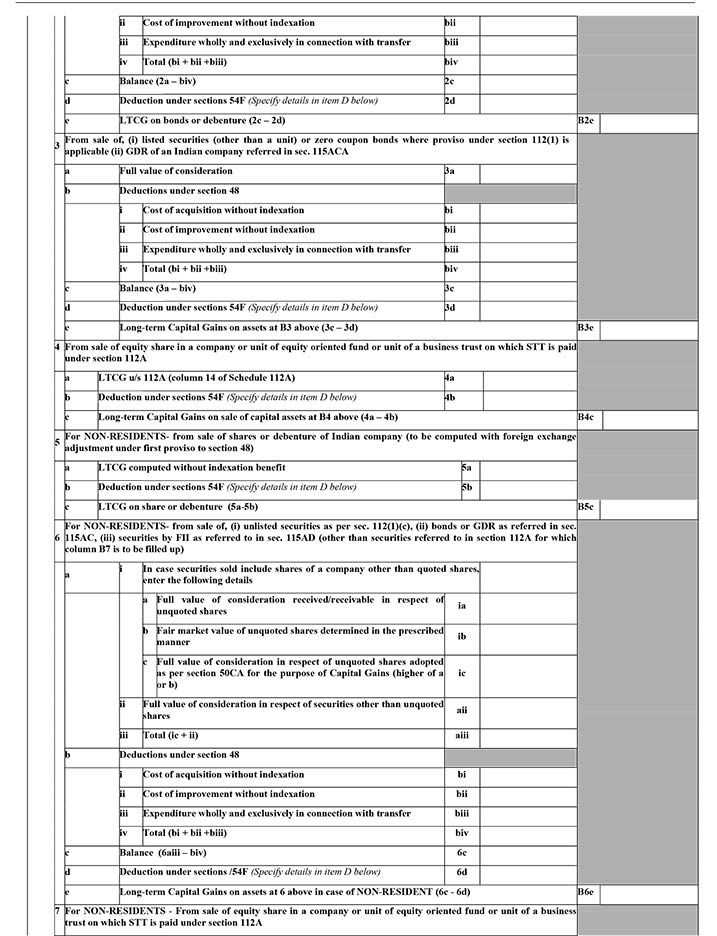

B. Long term Capital Gains

From the sale of land or building or both

From the sale of bonds or debentures

From the sale of listed securities or zero coupon bonds where proviso u/s 112 is applicable or from the sale of GDR referred to in section 115ACA

From the sale of equity share in a company or unit of equity oriented fund or unit of a business trust on which STT is paid under section 112A

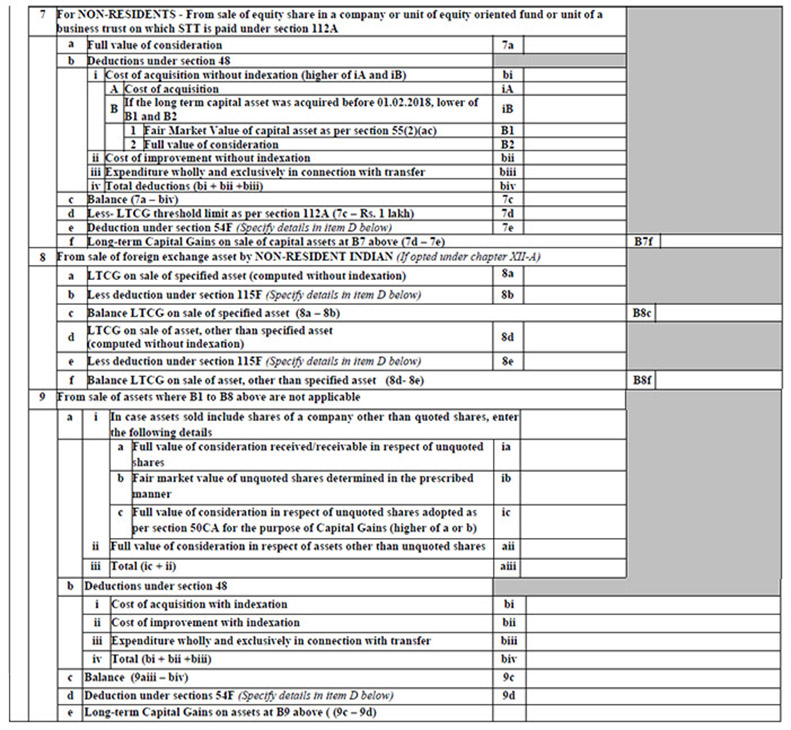

For NON-RESIDENTS- from the sale of shares or debenture of an Indian company

For NON-RESIDENT- from the sale of unlisted securities/bonds/ securities by FII

For NON-RESIDENTS – From the sale of equity share in a company or unit of equity oriented fund or unit of a business trust on which STT is paid under section 112A

From the sale of foreign exchange asset by NRI

From the sale of assets where B1 to B8 above are not applicable

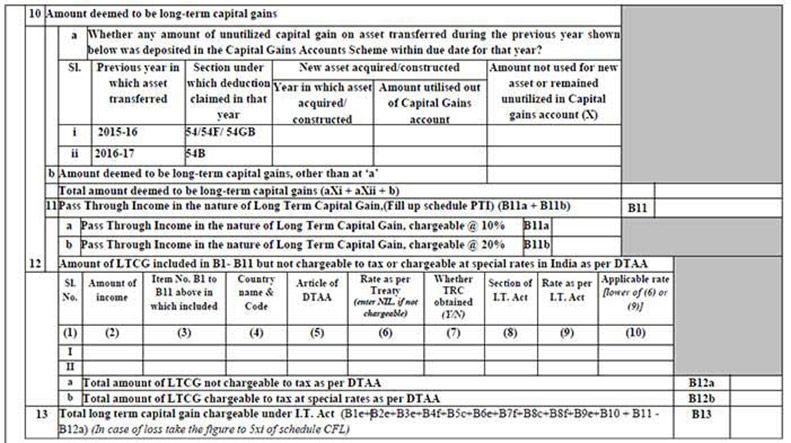

Amount deemed to be long term capital gains

Pass-Through Income in the nature of Long Term Capital Gain,(Fill up schedule PTI) (B11a + B11b)

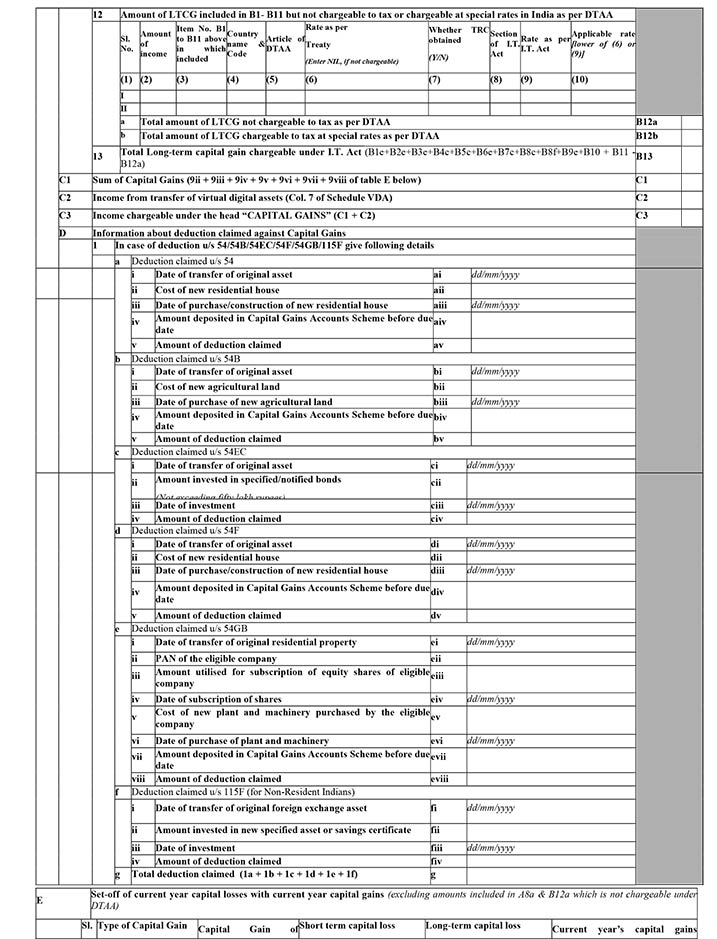

Amount of LTCG included in B1-A8 but not chargeable to tax or chargeable at special rates in India as per DTAA

Total long term capital gain chargeable under I.T. Act

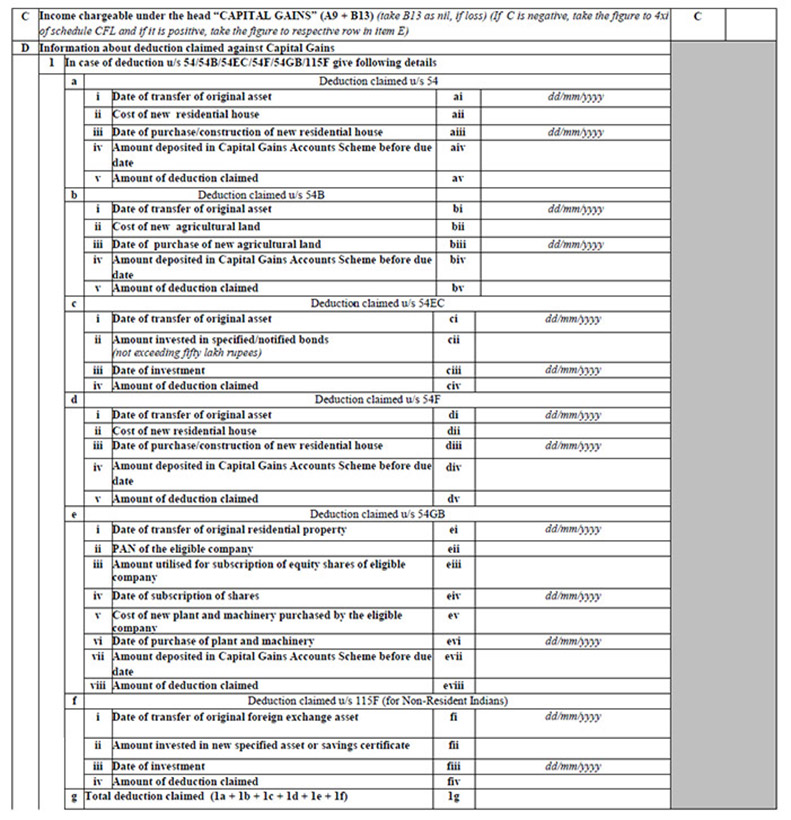

C. Income chargeable under the head “CAPITAL GAINS” (A9 + B13)

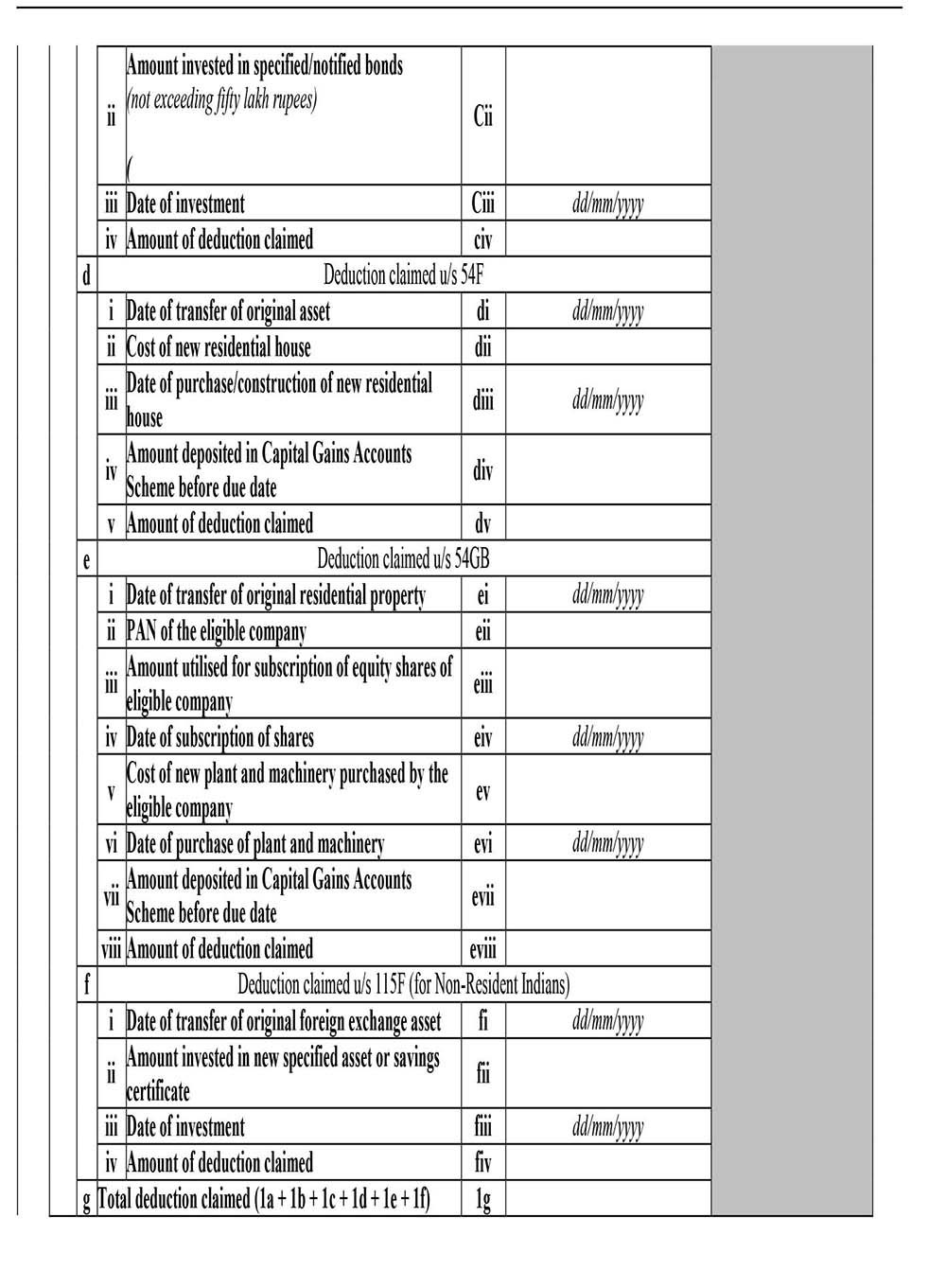

D. Information about deduction claimed against Capital Gains

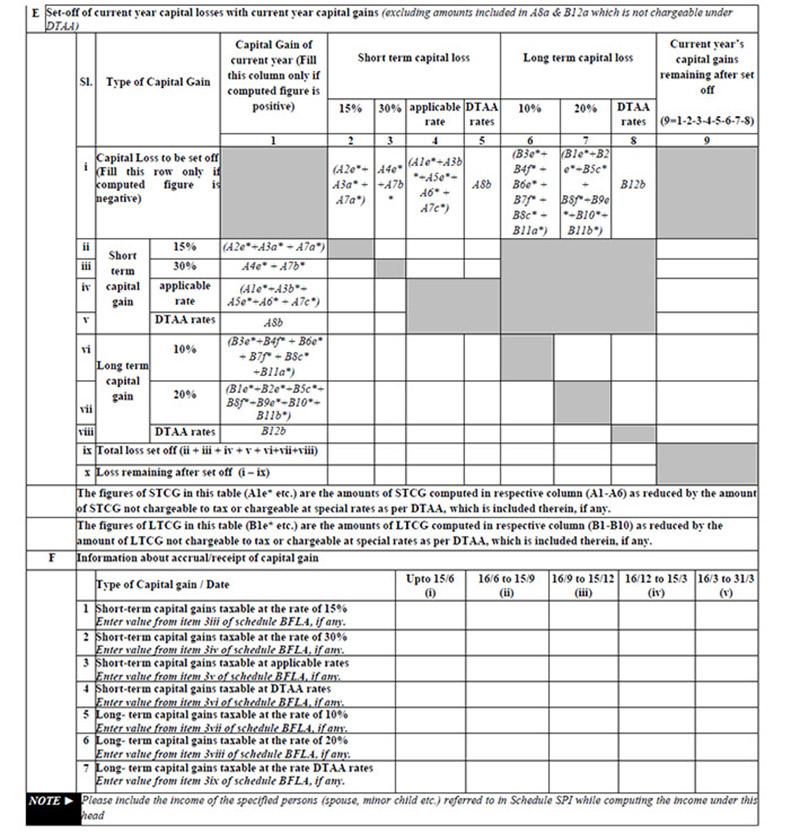

E. Set-off of current year capital losses with current year capital gains

F. Information about accrual/receipt of capital gain

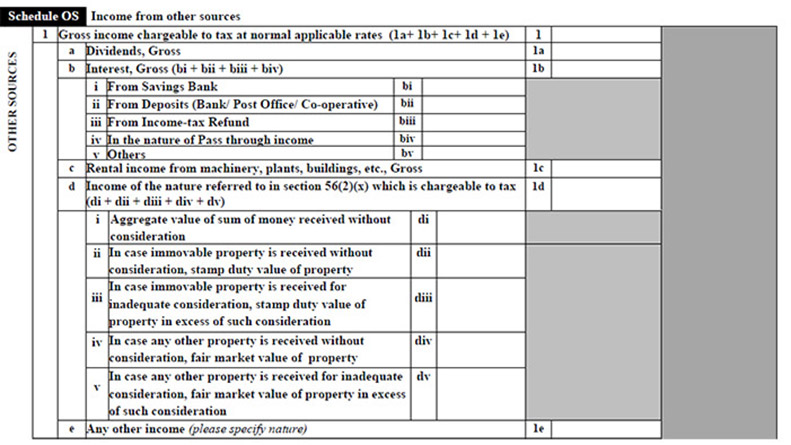

Schedule OS:

Income from other sources: The information regarding income from other sources is enclosed:

Gross income chargeable to tax at normal applicable rates (1a+ 1b+ 1c+ 1d + 1e)

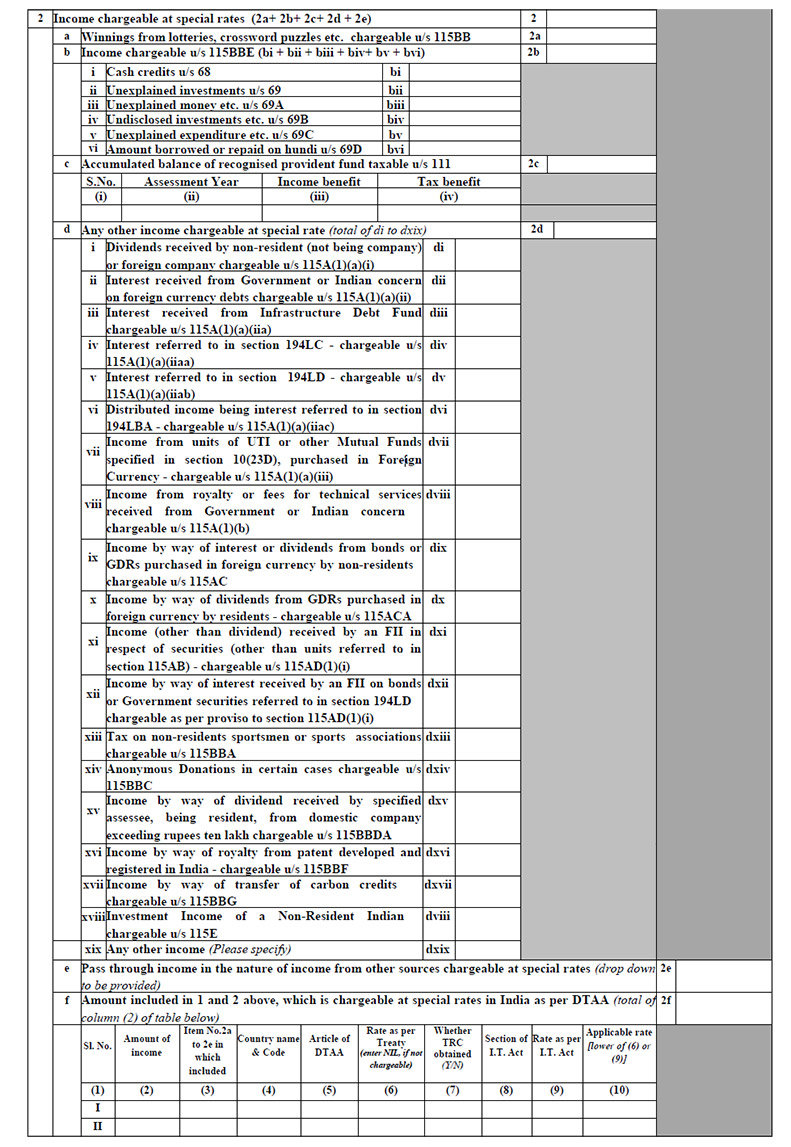

Income chargeable at special rates (2a+ 2b+ 2c+ 2d + 2e)

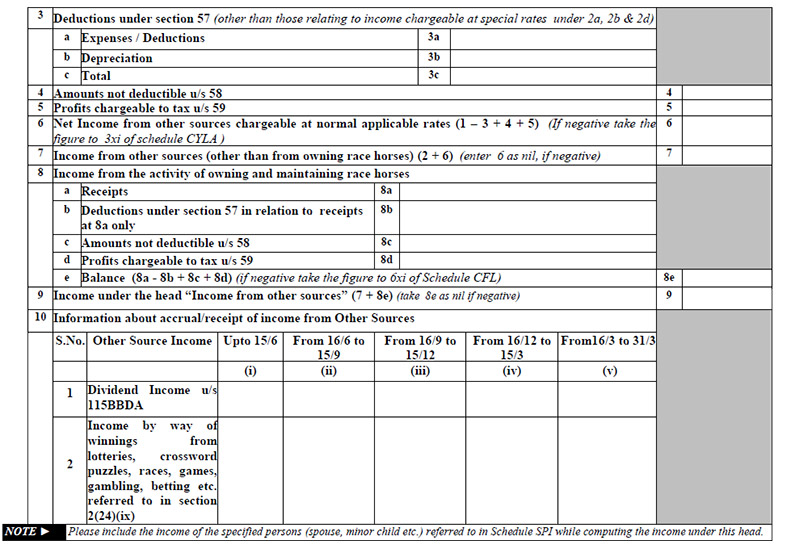

Deductions under section 57

Amounts not deductible u/s 58

Profits chargeable to tax u/s 59

Net Income from other sources chargeable at normal applicable rates

Income from other sources (other than from owning race horses)

Income from the activity of owning and maintaining race horses

Income under the head “Income from other sources” (7 + 8e)

Information about accrual/receipt of income from Other Sources

Schedule CYLA:

Details under this heading are enclosed with the following details of the taxpayer to furnish with:

Head/ Source of Income

Income of current year

House property loss of the current year set off

Other sources loss (other than the loss from race horses) of the current year set off

Current year’s Income remaining after set off

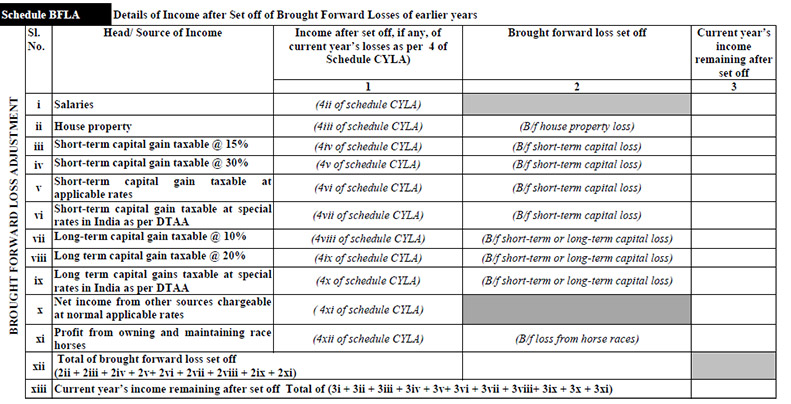

Schedule BFLA:

Details under this heading are enclosed with the following details of the taxpayer to furnish with:

Head/ Source of Income

Income after set off, if any, of current year’s losses as per 4 of Schedule CYLA)

Brought forward loss set off

Current year’s income remaining after set off

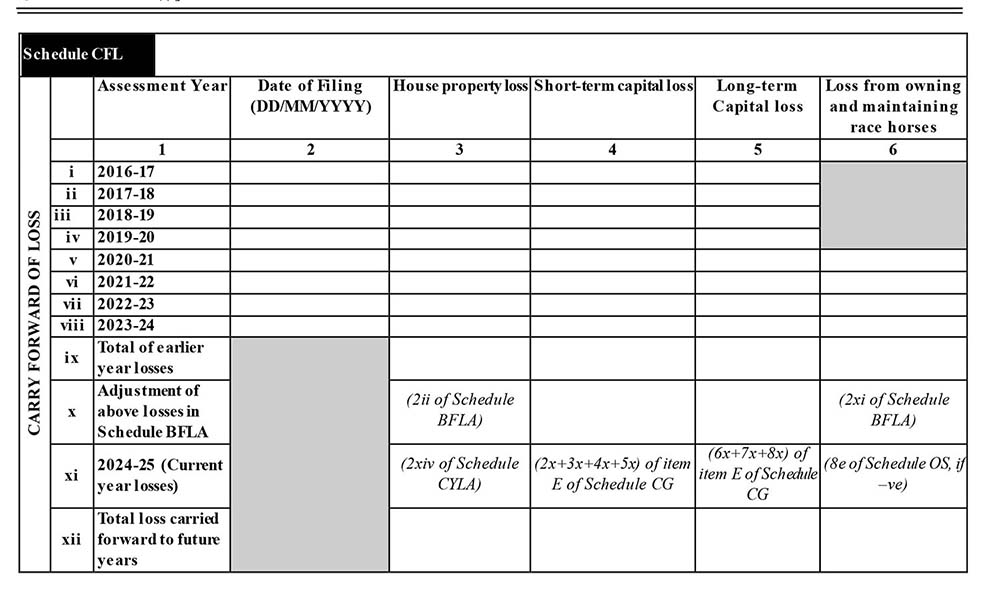

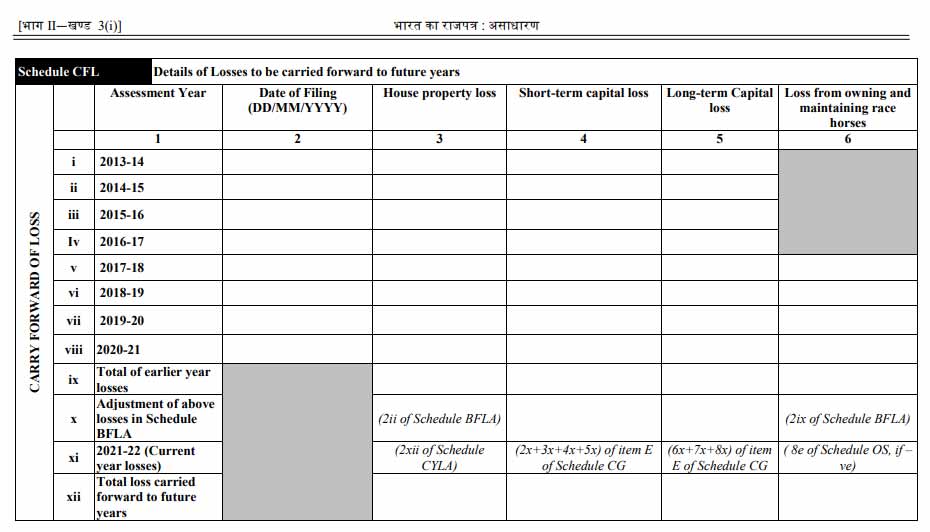

Schedule CFL:

Details under this heading are enclosed with the following details of the taxpayer to furnish with:

Assessment Year

Date of Filing

House property loss

Short-term capital loss

Long-term Capital loss

Loss from owning and maintaining race horses

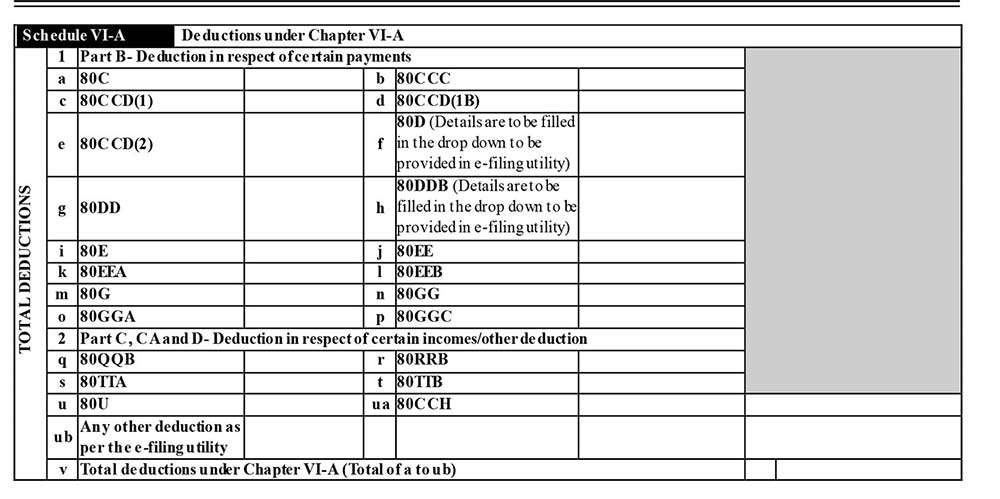

Schedule VI-A: Deductions under Chapter VI-A

Details under this title are enclosed with the following details of the taxpayer to furnish with:

1. Part B- Deduction in respect of certain payments 2. Part C, CA and D- Deduction in respect of certain incomes/other deduction

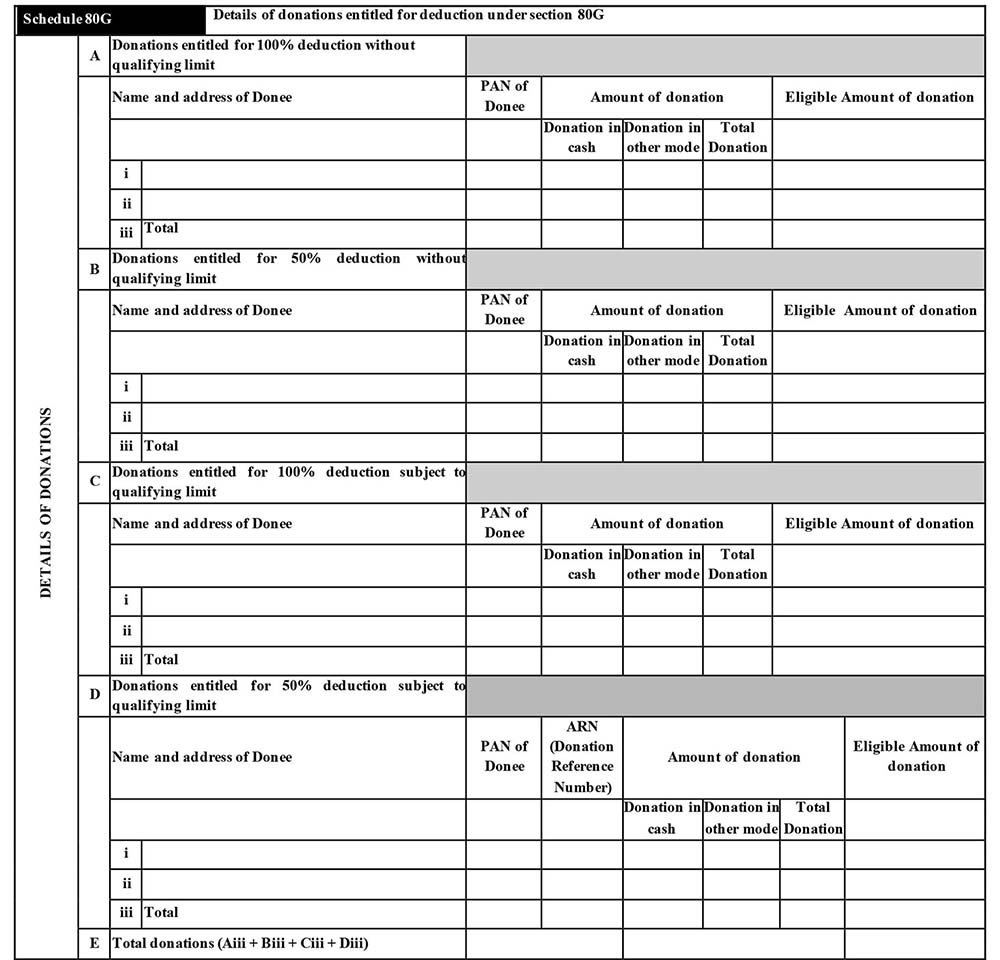

Schedule 80G: Details of donations entitled for deduction under section 80G

Donations entitled for 100% deduction without qualifying limit

Donations entitled for 50% deduction without qualifying limit

Donations entitled for 100% deduction subject to qualifying limit

Donations entitled for 50% deduction subject to qualifying limit

Total donations

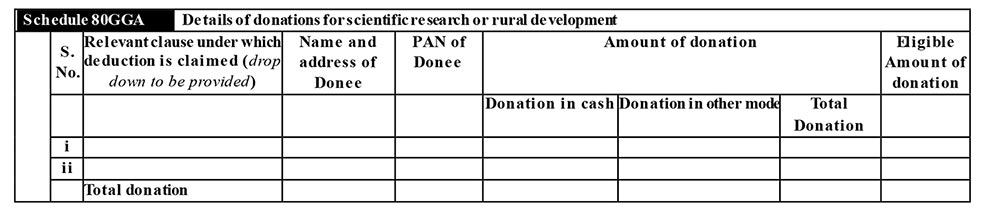

Schedule 80GGA:

R Details of donations for scientific research or rural development relevant clause under which deduction is

Claimed Name and address of donee

PAN of Donee

Amount of donation

Eligible Amount of donation

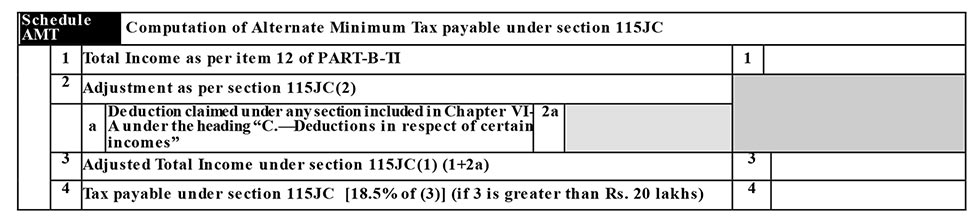

Schedule AMT: Computation of Alternate Minimum Tax payable under section 115JC

Total Income as per item 12 of PART-B-TI

Adjustment as per section 115JC(2)

Adjusted Total Income under section 115JC(1) (1+2a)

Tax payable under section 115JC [18.5% of (3)] (if 3 is greater than Rs. 20 lakhs)

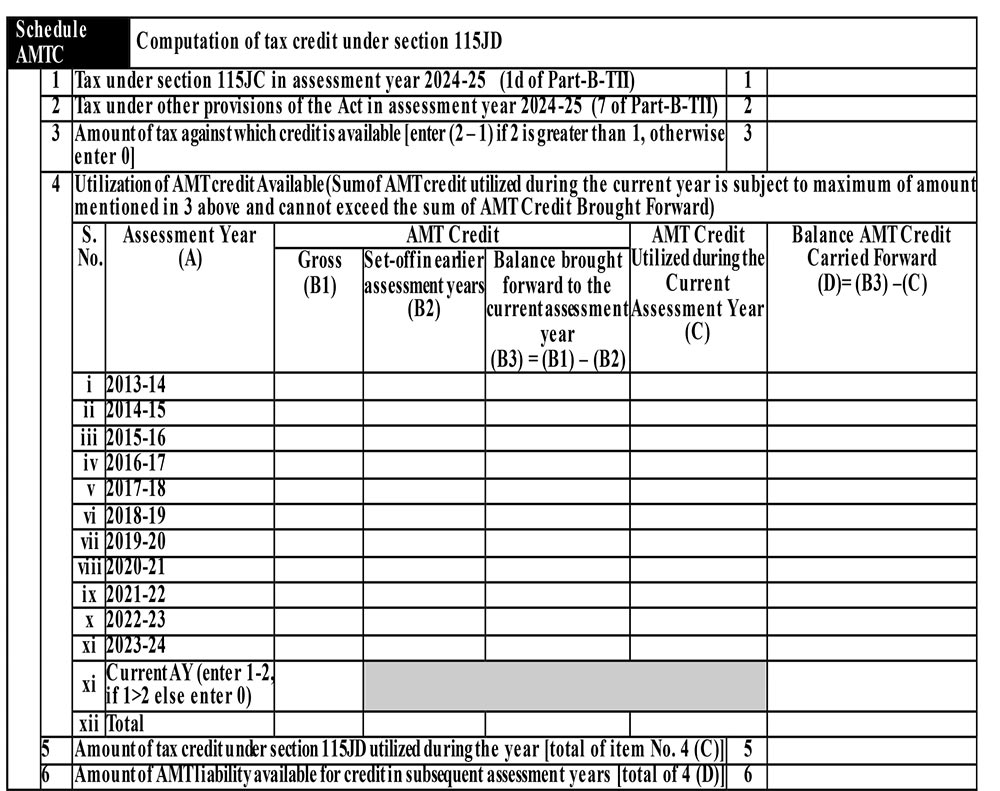

Schedule AMTC: Computation of tax credit under section 115JD

The tax under section 115JC in the assessment year 2019-20 (1d of Part-B-TTI)

The tax under other provisions of the Act in the assessment year 2019-20 (7 of Part-B-TTI)

Amount of tax against which credit is available [enter (2 – 1) if 2 is greater than 1, otherwise enter 0]

The utilisation of AMT credit Available

Amount of tax credit under section 115JD utilised during the year [total of item No. 4 (C)]

Amount of AMT liability available for credit in subsequent assessment years [total of 4 (D)]

Schedule SPI:

Income of specified persons (spouse, minor child etc.) includable in income of the assessee as per section 64

Name of person

PAN of person (optional)

Relationship

Amount

Head of Income in which included

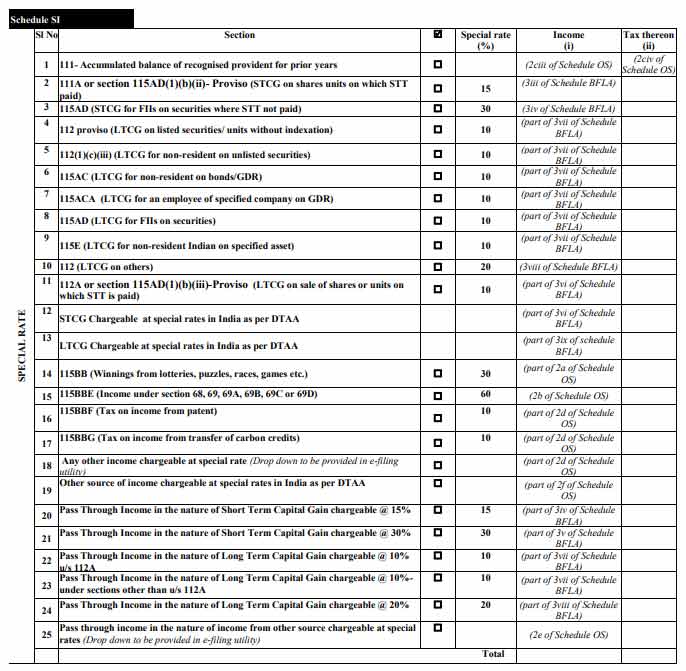

Schedule SI: Income chargeable to tax at special rates

1. 111A (STCG on shares units on which STT paid) 15 (3iii of schedule BFLA) 2. 115AD (STCG for FIIs on securities where STT not paid) 30 (3iv of schedule BFLA) 3. 112 proviso (LTCG on listed securities/ units without indexation) 10 (part of 3vii of schedule BFLA) 4. 112(1)(c)(iii) (LTCG for non-resident on unlisted securities) 10 (part of 3vii of schedule BFLA) 5. 115AC (LTCG for non-resident on bonds/GDR) 10 (part of 3vii of schedule BFLA 6. 115ACA (LTCG for an employee of the specified company on GDR) 10 (part of 3vii of schedule BFLA) 7. 115AD (LTCG for FIIs on securities) 10 (part of 3vii of schedule BFLA) 8. 115E (LTCG for non-resident Indian on specified asset) 10 (part of 3vii of schedule BFLA) Page S15 9. 112 (LTCG on others) 20 (3viii of schedule BFLA) 10. 112A (LTCG on the sale of shares or units on which STT is paid) 11. STCG Chargeable at special rates in India as per DTAA (part of 3vi of schedule BFLA) 12. LTCG Chargeable at special rates in India as per DTAA (part of 3ix of schedule BFLA) 13. 115BB (Winnings from lotteries, puzzles, races, games etc.) 30 (part of 2a of schedule OS) 14. 115BBDA (Dividend income from domestic company exceeding Rs.10 lakh) 10 (part of 2d of schedule OS) 15. 115BBE (Income under section 68, 69, 69A, 69B, 69C or 69D) 60 (2b of schedule OS) 16. 115BBF (Tax on income from the patent) 10 (part of 2d of schedule OS) 17. 115BBG (Tax on income from transfer of carbon credits) 10 (part of 2d of schedule OS) 18. Any other income chargeable at a special rate (Drop down to be provided in e-filing utility) (part of 2d of schedule OS) 19. Other sources of income chargeable at special rates in India as per DTAA (part of 2f of schedule OS) 20. Pass-Through Income in the nature of Short Term Capital Gain chargeable @ 15% 15 (part of 3iv of schedule BFLA) 21. Pass-Through Income in the nature of Short Term Capital Gain chargeable @ 30% 30 (part of 3v of schedule BFLA) 22. Pass-Through Income in the nature of Long Term Capital Gain chargeable @ 10% 10 (part of 3vii of schedule BFLA) 23. Pass-Through Income in the nature of Long Term Capital Gain chargeable @ 20% 20 (part of 3viii of schedule BFLA) 24. Pass through income in the nature of income from other sources chargeable at special rates

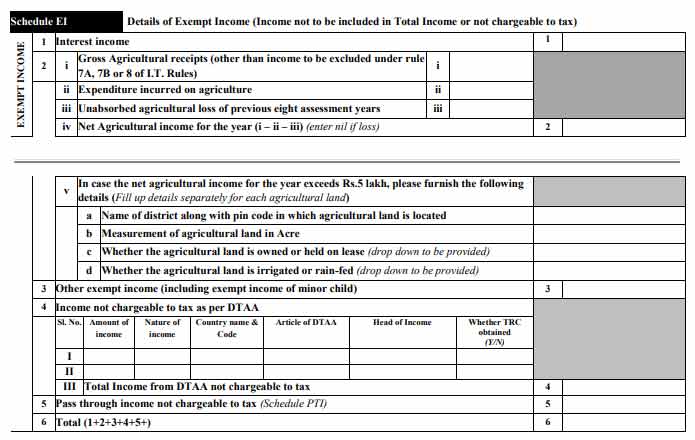

Schedule EI:

Details of Exempt Income (Income not to be included in Total Income or not chargeable to tax)

1 Interest income

2 Dividend income from the domestic company (amount not exceeding Rs. 10 lakh)

3

i Gross Agricultural receipts (other than income to be excluded under rule 7A, 7B or 8 of I.T. Rules)

ii Expenditure incurred on agriculture ii

iii Unabsorbed agricultural loss of previous eight assessment years iii

iv Net Agricultural income for the year (i – ii – iii) (enter nil if loss) 3

v In case the net agricultural income for the year exceeds Rs.5 lakh, please furnish the following details (Fill up details separately for each agricultural land)

a Name of the district along with pin code in which agricultural land is located

b Measurement of agricultural land in Acre

c Whether the agricultural land is owned or held on lease (drop down to be provided)

d Whether the agricultural land is irrigated or rain-fed (drop down to be provided)

4 Other exempt income (including exempt income of minor child) 4

5 Income not chargeable to tax as per DTAA

Sl. No. Amount of income

Nature of income

Country name & Code

Article of DTAA

Head of Income

Whether TRC obtained

(Y/N) I, II, III Total Income from DTAA not chargeable to tax 5

6 Pass through income not chargeable to tax (Schedule PTI) 6

7 Total (1+2+3+4+5+6)

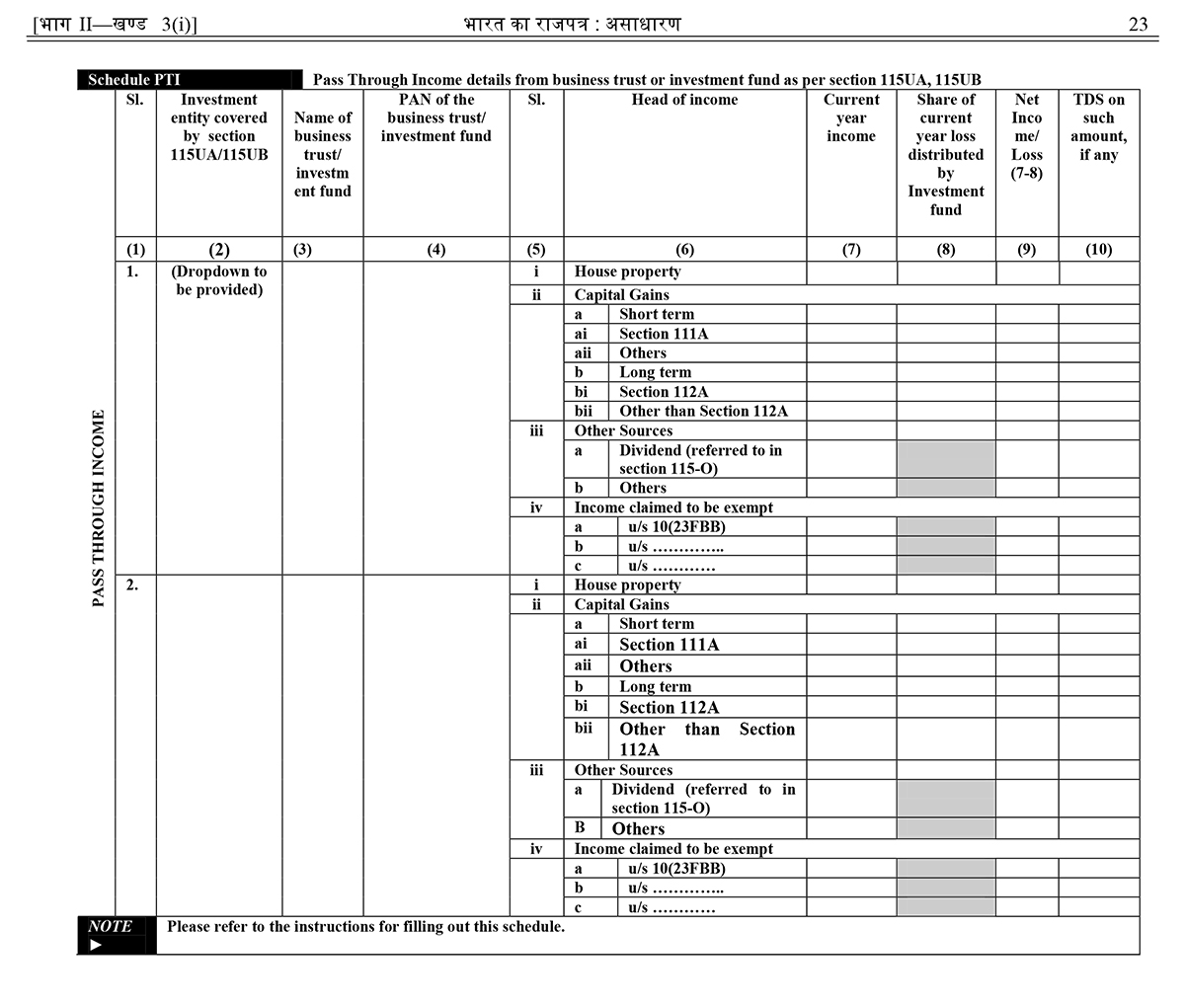

Schedule PTI:

Pass-Through Income details from the business trust or investment fund as per section 115UA, 115UB

Name of business trust/ investment fund

PAN of the business trust/ investment fund

Head of income

Amount of income

TDS on such amount, if any

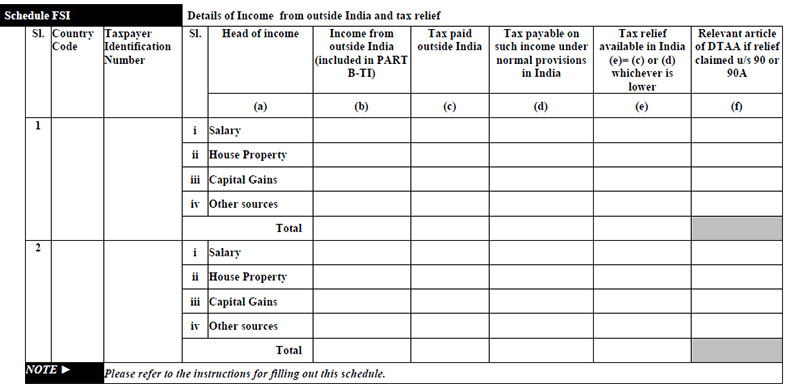

Schedule FSI:

Details of Income from outside India and tax relief

Country Code

Taxpayer Identification Number

Head of income

Income from outside India (included in PART B-TI)

Tax paid outside India

Tax payable on such income under normal provisions in India

Tax relief available in India (e)= (c) or (d) whichever is lower

Relevant article of DTAA if relief claimed u/s 90 or 90A

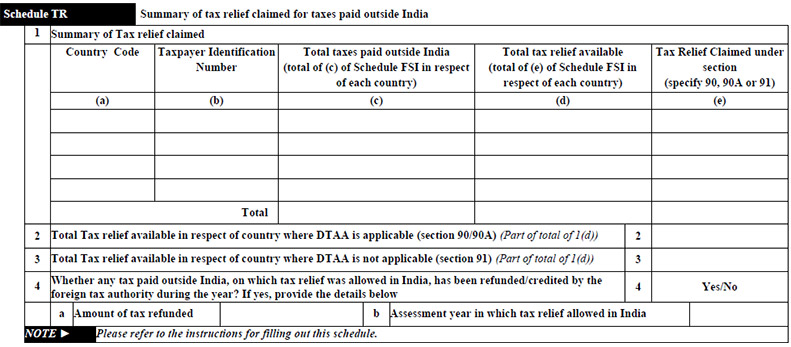

Schedule TR:

Summary of tax relief claimed for taxes paid outside India

1 Summary of Tax relief claimed

2 Total Tax relief available in respect of country where DTAA is applicable (section 90/90A)

3 Total Tax relief available in respect of country where DTAA is not applicable (section 91)

4 Whether any tax paid outside India, on which tax relief was allowed in India, has been refunded/credited by the foreign tax authority during the year?

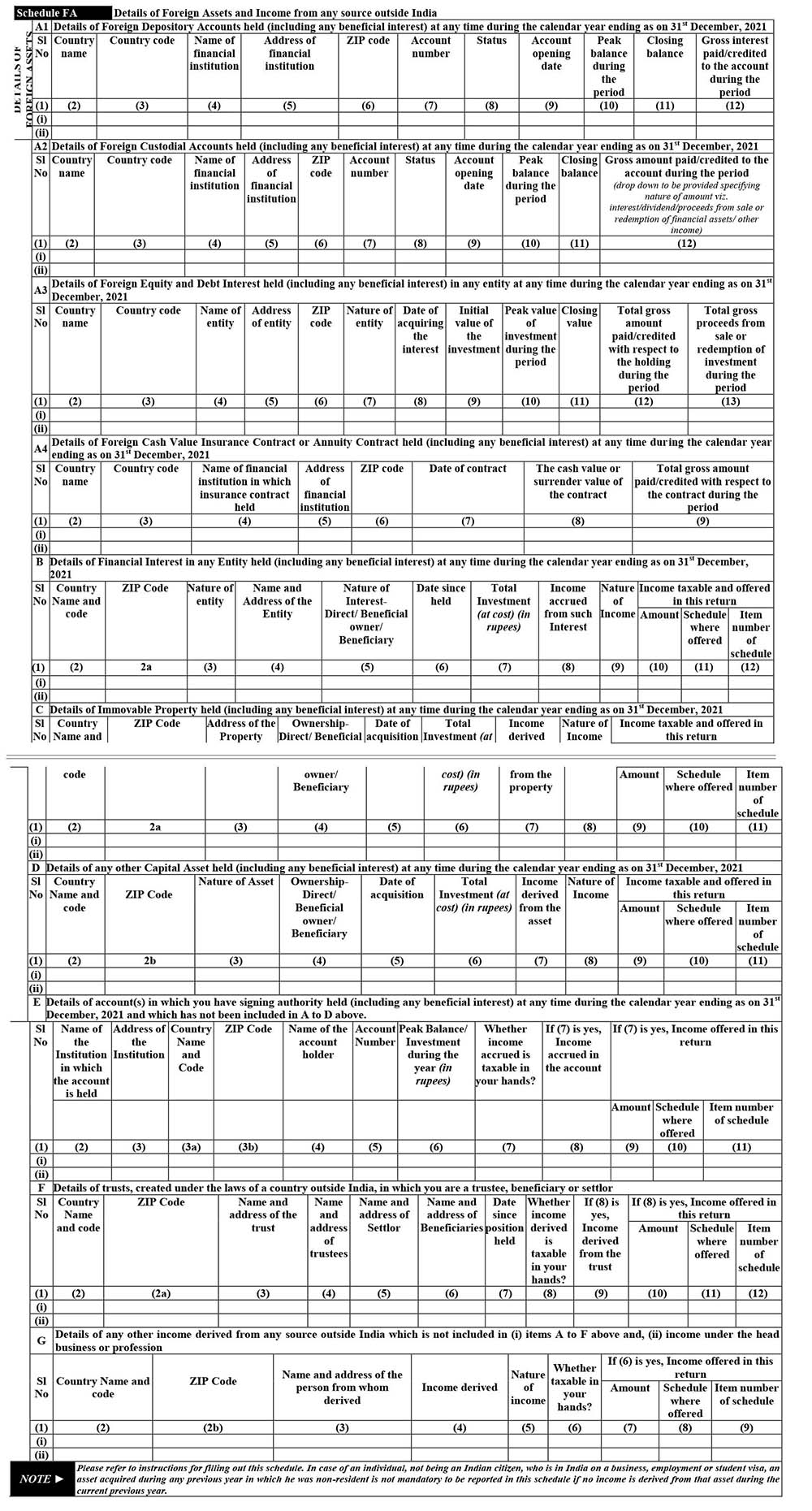

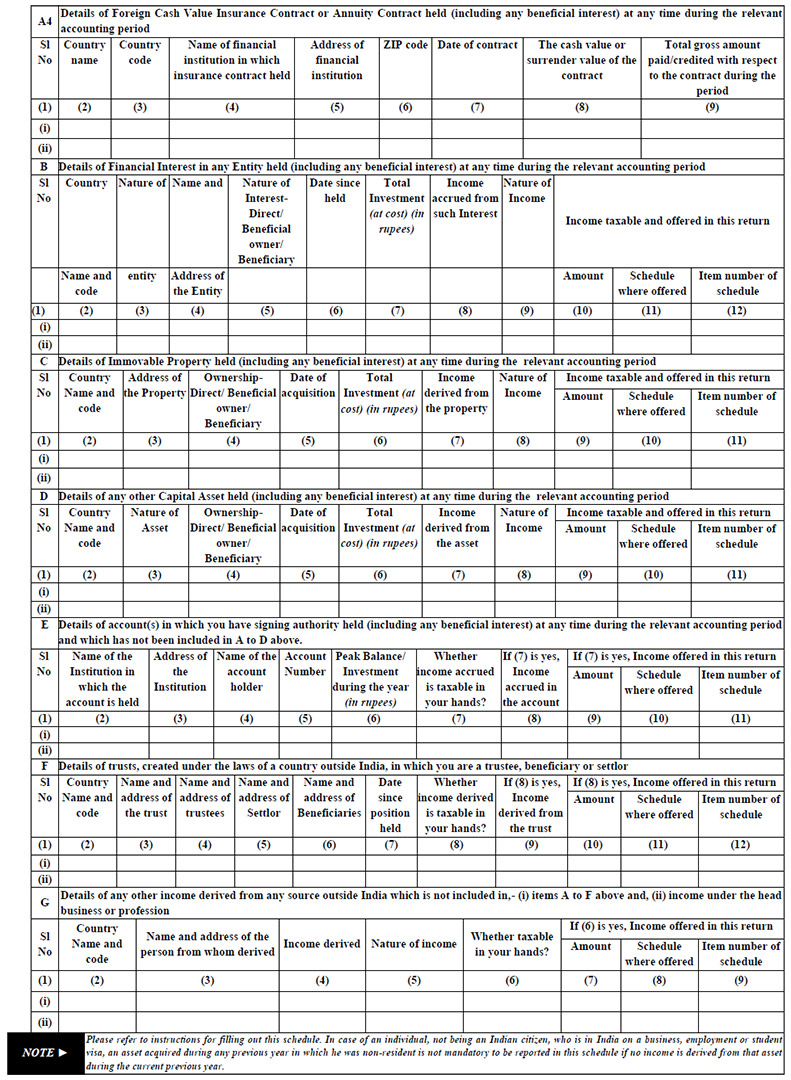

Schedule FA:

Details of Foreign Assets and Income from any source outside India

A1 Details of Foreign Depository Accounts held (including any beneficial interest) at any time during the relevant accounting period

A2 Details of Foreign Custodial Accounts held (including any beneficial interest) at any time during the relevant accounting period

A3 Details of Foreign Equity and Debt Interest held (including any beneficial interest) in any entity at any time during the relevant accounting period

A4 Details of Foreign Cash Value Insurance Contract or Annuity Contract held (including any beneficial interest) at any time during the relevant accounting period

B Details of Financial Interest in any Entity held

C Details of Immovable Property held

D Details of any other Capital Asset held

E Details of account(s) in which you have signing authority held (including any beneficial interest) at any time during the relevant accounting period and which has not been included in A to D above.

F Details of trusts, created under the laws of a country outside India, in which you are a trustee, beneficiary or settlor

G Details of any other income derived from any source outside India which is not included in,- items A to F above and, (ii) income under the head business or profession

Schedule 5A:

Information regarding apportionment of income between spouses governed by Portuguese Civil Code

Name of the spouse

PAN of the spouse

Heads of Income

Income received under the head

Amount apportioned in the hands of the spouse

Amount of TDS deducted on income at (ii)

TDS apportioned in the hands of the spouse

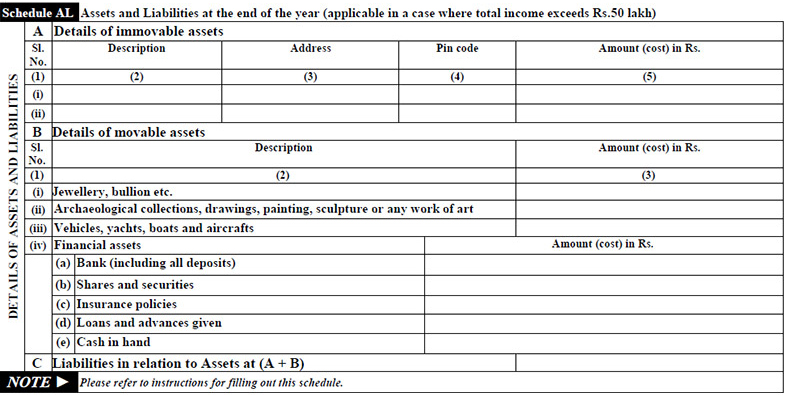

Schedule AL:

Assets and Liabilities at the end of the year (applicable in a case where the total income exceeds Rs.50 lakh)

A Details of immovable assets

B Details of movable assets

C Liabilities in relation to Assets at (A + B)

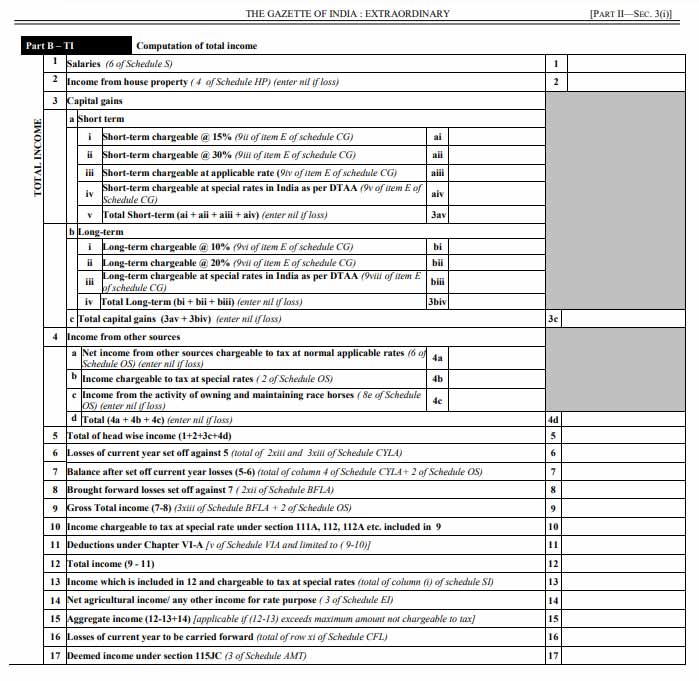

Part B-TI: Computation of Total Income

The information regarding total income is enclosed with the following details of the taxpayer to furnish with:

Salaries

Income from house property

Capital gains

Income from other sources

Losses of the current year set off

Balance after set off current year losses

Brought forward losses set off

Gross Total income

Income chargeable to tax at the special rate under section 111A, 112 etc

Deductions under Chapter VI-A

Total income

Income chargeable to tax at special rates and included in the above point

Net agricultural income/ any other income for rate purpose

Aggregate income

Losses of the current year to be carried forward

Deemed income under section 115JC

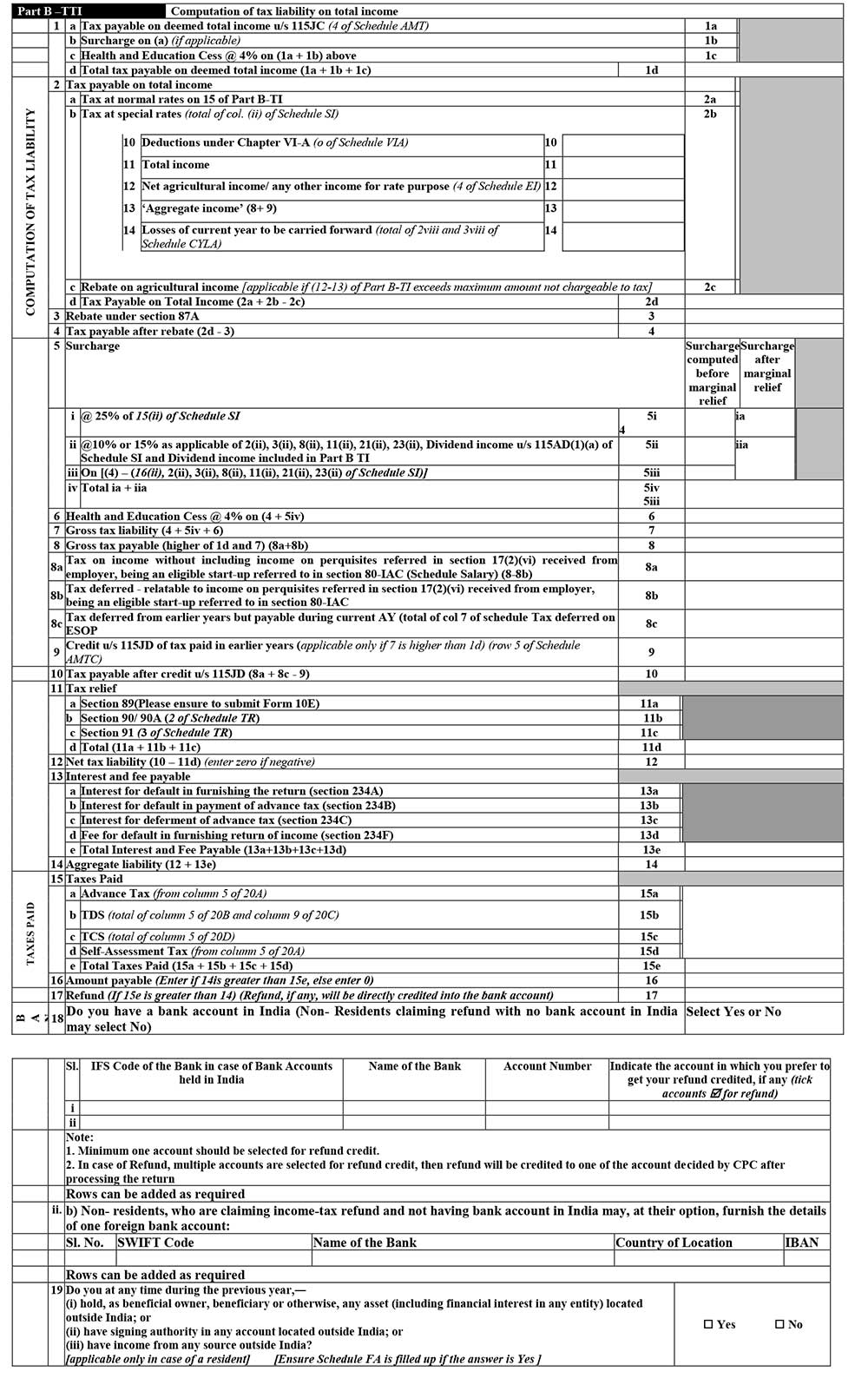

Part B-TTI: Computation of tax liability on total income

The information regarding the Computation of tax liability on total income is enclosed with the following details of the taxpayer to furnish with:

Tax payable on total income

Rebate under section 87A

Tax payable after rebate

Surcharge

Health and Education Cess

Gross tax liability

Gross tax payable

Credit u/s 115JD of tax paid in earlier years

Tax payable after credit u/s 115JD (8 – 9)

Tax relief

Net tax liability

Interest and fee payable

Aggregate liability

Taxes Paid

The amount payable/refundable

Refund

Details of all Bank Accounts held in India at any time during the previous year

Do you at any time during the previous year

(i) hold, as beneficial owner, beneficiary or otherwise, any asset (including financial interest in any entity) located outside India; or

(ii) have signing authority in any account located outside India; or

(iii) have income from any source outside India?

20 If the return has been prepared by a Tax Return Preparer (TRP) give further details below:

Identification No. of TRP

Name of TRP

Counter Signature of TRP

21 If TRP is entitled for any reimbursement from the Government, amount thereof 21

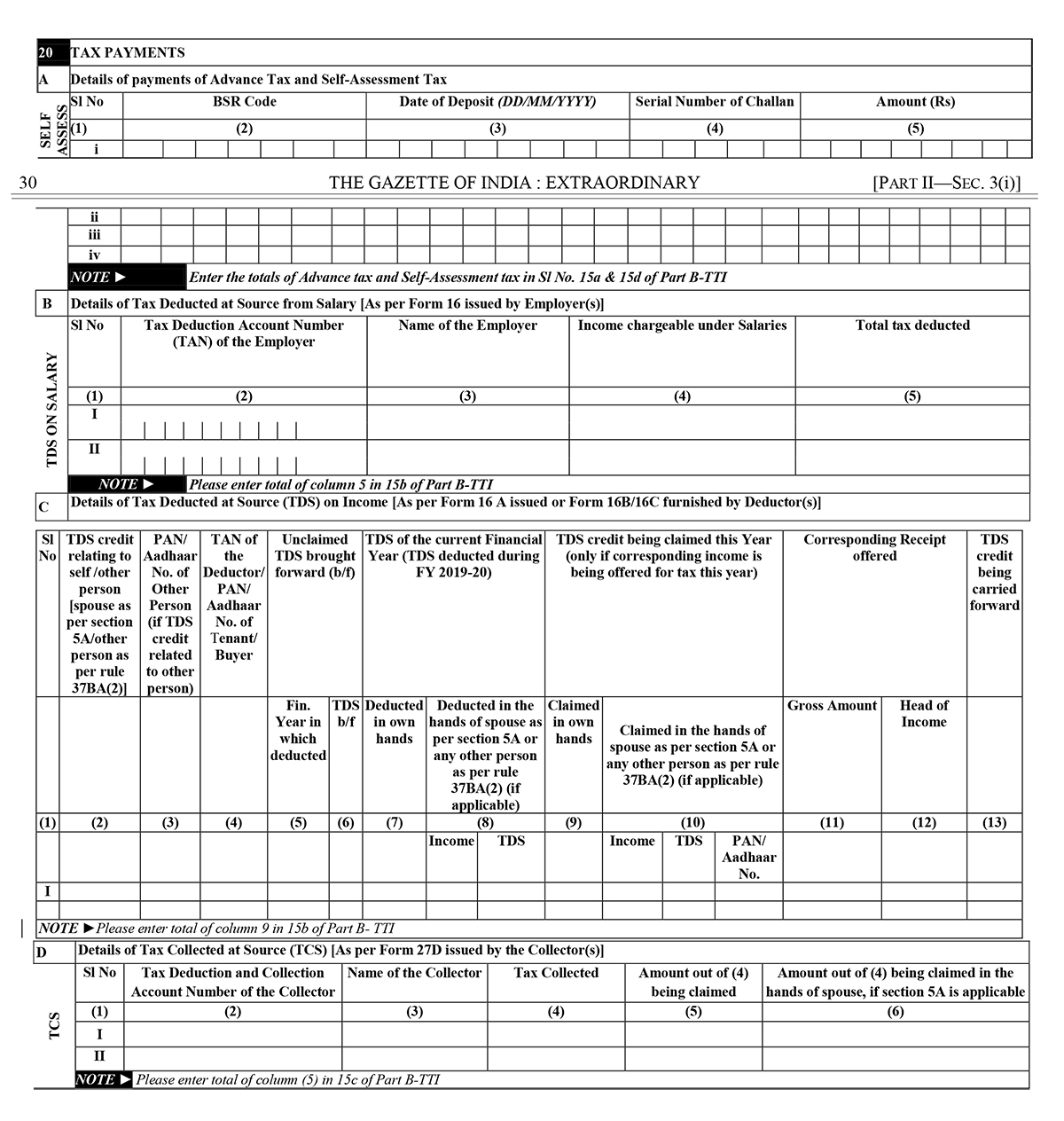

22 TAX PAYMENTS

A Details of payments of Advance Tax and Self-Assessment Tax B Details of Tax Deducted at Source from Salary [As per Form 16 issued by Employer(s)]

Verification: There will be verification at the end of all the General, Part B TI and Part B TTI ensuring that the details given are factually correct and self-attested by the taxpayer.

Income Tax Return 2 Form Filing Mode

An ITR-2 form can be furnished either in online or offline mode. In online mode, either XML needs to be uploaded or client can directly login to income tax portal and select the submission mode as “prepare and submit online”. In the case of online filing, some data can be imported from the latest ITR or form 26AS. Super senior citizens (Age of 80 years or more) are exempted from the online filing of ITR. Offline here means to furnish the return form in paper format.

Online:

While furnishing ITR-2 online, feed the details and e-verify return using EVC via Bank Account/Net Banking/Demat Account/Aadhar OTP or

2. Feed the details using electronic medium and send a physical copy of ITR V to Centralized Processing Centre (CPC), Bengaluru through speed post or normal post. When you furnish the ITR-2 return form using electronic medium, the receipt will be seen in the inbox of the registered email id. It can also be downloaded from the official income tax website manually. After downloading the acknowledgement, you need to sign the form and then send CPC office, Bangalore before completing 120 days counting from the e-filing date. On the other side, it is not required to send the ITR V to the CPC if EVC/OTP option is used

Offline:

If the age of the person is 80 or more years during the respective tax period or in the previous year, he/she can opt for offline return filing.

Modifications In ITR 2 For Assessment Year AY 2019-20:

Pensioners column has been added in the nature of employment.

A new deduction of 80TTB has been added in the deductions column.

From this assessment year, assesse is required to disclose his Directorship in Unlisted Company if any. Assesse has to provide the name of the Company, it’s PAN and his Director Identification Number

Assesse is required to provide details of shareholding of Unlisted Company wherein he has to provide all the details of shares purchased and sold during the financial year.

Facility of filing paper returns will now be available only to those over 80 years.

Those in possession of foreign assets will need to provide detailed disclosure of foreign depository account, foreign custodian accounts, equity and debt interest and particulars of overseas cash value insurance contract or annuity contract.

Taxpayers having agricultural income will have to provide additional details, including land measurement in acres, the name of the district along with Pincode in which the land is located, quality of land mentioning whether the land is irrigated or rain-fed etc.and whether the land is owned or held on lease.

Income received from the residential house properties would have to furnish details such as Tenant Name, PAN or TAN Number.

B. Long term Capital Gains

From the sale of land or building or both

From the sale of bonds or debentures

From the sale of listed securities or zero coupon bonds where proviso u/s 112 is applicable or from the sale of GDR referred to in section 115ACA

From the sale of equity share in a company or unit of equity oriented fund or unit of a business trust on which STT is paid under section 112A

For NON-RESIDENTS- from the sale of shares or debenture of an Indian company

For NON-RESIDENT- from the sale of unlisted securities/bonds/ securities by FII

For NON-RESIDENTS – From the sale of equity share in a company or unit of equity oriented fund or unit of a business trust on which STT is paid under section 112A

From the sale of foreign exchange asset by NRI

From the sale of assets where B1 to B8 above are not applicable

Amount deemed to be long term capital gains

Pass-Through Income in the nature of Long Term Capital Gain,(Fill up schedule PTI) (B11a + B11b)

Amount of LTCG included in B1-A8 but not chargeable to tax or chargeable at special rates in India as per DTAA

Total long term capital gain chargeable under I.T. Act

C. Income chargeable under the head “CAPITAL GAINS” (A9 + B13)

D. Information about deduction claimed against Capital Gains

E. Set-off of current year capital losses with current year capital gains

F. Information about accrual/receipt of capital gain

Schedule OS:

Income from other sources: The information regarding income from other sources is enclosed:

Gross income chargeable to tax at normal applicable rates (1a+ 1b+ 1c+ 1d + 1e)

Income chargeable at special rates (2a+ 2b+ 2c+ 2d + 2e)

Deductions under section 57

Amounts not deductible u/s 58

Profits chargeable to tax u/s 59

Net Income from other sources chargeable at normal applicable rates

Income from other sources (other than from owning race horses)

Income from the activity of owning and maintaining race horses

Income under the head “Income from other sources” (7 + 8e)

Information about accrual/receipt of income from Other Sources

Schedule CYLA:

Details under this heading are enclosed with the following details of the taxpayer to furnish with:

Head/ Source of Income

Income of current year

House property loss of the current year set off

Other sources loss (other than the loss from race horses) of the current year set off

Current year’s Income remaining after set off

Schedule BFLA:

Details under this heading are enclosed with the following details of the taxpayer to furnish with:

Head/ Source of Income

Income after set off, if any, of current year’s losses as per 4 of Schedule CYLA)

Brought forward loss set off

Current year’s income remaining after set off

Schedule CFL:

Details under this heading are enclosed with the following details of the taxpayer to furnish with:

Assessment Year

Date of Filing

House property loss

Short-term capital loss

Long-term Capital loss

Loss from owning and maintaining race horses

Schedule VI-A: Deductions under Chapter VI-A

Details under this title are enclosed with the following details of the taxpayer to furnish with:

1. Part B- Deduction in respect of certain payments 2. Part C, CA and D- Deduction in respect of certain incomes/other deduction

Schedule 80G: Details of donations entitled for deduction under section 80G

Donations entitled for 100% deduction without qualifying limit

Donations entitled for 50% deduction without qualifying limit

Donations entitled for 100% deduction subject to qualifying limit

Donations entitled for 50% deduction subject to qualifying limit

Total donations

Schedule 80GGA:

R Details of donations for scientific research or rural development relevant clause under which deduction is

Claimed Name and address of donee

PAN of Donee

Amount of donation

Eligible Amount of donation

Schedule AMT: Computation of Alternate Minimum Tax payable under section 115JC

Total Income as per item 12 of PART-B-TI

Adjustment as per section 115JC(2)

Adjusted Total Income under section 115JC(1) (1+2a)

Tax payable under section 115JC [18.5% of (3)] (if 3 is greater than Rs. 20 lakhs)

Schedule AMTC: Computation of tax credit under section 115JD

The tax under section 115JC in the assessment year 2019-20 (1d of Part-B-TTI)

The tax under other provisions of the Act in the assessment year 2019-20 (7 of Part-B-TTI)

Amount of tax against which credit is available [enter (2 – 1) if 2 is greater than 1, otherwise enter 0]

The utilisation of AMT credit Available

Amount of tax credit under section 115JD utilised during the year [total of item No. 4 (C)]

Amount of AMT liability available for credit in subsequent assessment years [total of 4 (D)]

Schedule SPI:

Income of specified persons (spouse, minor child etc.) includable in income of the assessee as per section 64

Name of person

PAN of person (optional)

Relationship

Amount

Head of Income in which included

Schedule SI: Income chargeable to tax at special rates

1. 111A (STCG on shares units on which STT paid) 15 (3iii of schedule BFLA) 2. 115AD (STCG for FIIs on securities where STT not paid) 30 (3iv of schedule BFLA) 3. 112 proviso (LTCG on listed securities/ units without indexation) 10 (part of 3vii of schedule BFLA) 4. 112(1)(c)(iii) (LTCG for non-resident on unlisted securities) 10 (part of 3vii of schedule BFLA) 5. 115AC (LTCG for non-resident on bonds/GDR) 10 (part of 3vii of schedule BFLA 6. 115ACA (LTCG for an employee of the specified company on GDR) 10 (part of 3vii of schedule BFLA) 7. 115AD (LTCG for FIIs on securities) 10 (part of 3vii of schedule BFLA) 8. 115E (LTCG for non-resident Indian on specified asset) 10 (part of 3vii of schedule BFLA) Page S15 9. 112 (LTCG on others) 20 (3viii of schedule BFLA) 10. 112A (LTCG on the sale of shares or units on which STT is paid) 11. STCG Chargeable at special rates in India as per DTAA (part of 3vi of schedule BFLA) 12. LTCG Chargeable at special rates in India as per DTAA (part of 3ix of schedule BFLA) 13. 115BB (Winnings from lotteries, puzzles, races, games etc.) 30 (part of 2a of schedule OS) 14. 115BBDA (Dividend income from domestic company exceeding Rs.10 lakh) 10 (part of 2d of schedule OS) 15. 115BBE (Income under section 68, 69, 69A, 69B, 69C or 69D) 60 (2b of schedule OS) 16. 115BBF (Tax on income from the patent) 10 (part of 2d of schedule OS) 17. 115BBG (Tax on income from transfer of carbon credits) 10 (part of 2d of schedule OS) 18. Any other income chargeable at a special rate (Drop down to be provided in e-filing utility) (part of 2d of schedule OS) 19. Other sources of income chargeable at special rates in India as per DTAA (part of 2f of schedule OS) 20. Pass-Through Income in the nature of Short Term Capital Gain chargeable @ 15% 15 (part of 3iv of schedule BFLA) 21. Pass-Through Income in the nature of Short Term Capital Gain chargeable @ 30% 30 (part of 3v of schedule BFLA) 22. Pass-Through Income in the nature of Long Term Capital Gain chargeable @ 10% 10 (part of 3vii of schedule BFLA) 23. Pass-Through Income in the nature of Long Term Capital Gain chargeable @ 20% 20 (part of 3viii of schedule BFLA) 24. Pass through income in the nature of income from other sources chargeable at special rates

Schedule EI:

Details of Exempt Income (Income not to be included in Total Income or not chargeable to tax)

1 Interest income

2 Dividend income from the domestic company (amount not exceeding Rs. 10 lakh)

3

i Gross Agricultural receipts (other than income to be excluded under rule 7A, 7B or 8 of I.T. Rules)

ii Expenditure incurred on agriculture ii

iii Unabsorbed agricultural loss of previous eight assessment years iii

iv Net Agricultural income for the year (i – ii – iii) (enter nil if loss) 3

v In case the net agricultural income for the year exceeds Rs.5 lakh, please furnish the following details (Fill up details separately for each agricultural land)

a Name of the district along with pin code in which agricultural land is located

b Measurement of agricultural land in Acre

c Whether the agricultural land is owned or held on lease (drop down to be provided)

d Whether the agricultural land is irrigated or rain-fed (drop down to be provided)

4 Other exempt income (including exempt income of minor child) 4

5 Income not chargeable to tax as per DTAA

Sl. No. Amount of income

Nature of income

Country name & Code

Article of DTAA

Head of Income

Whether TRC obtained

(Y/N) I, II, III Total Income from DTAA not chargeable to tax 5

6 Pass through income not chargeable to tax (Schedule PTI) 6

7 Total (1+2+3+4+5+6)

Schedule PTI:

Pass-Through Income details from the business trust or investment fund as per section 115UA, 115UB

Name of business trust/ investment fund

PAN of the business trust/ investment fund

Head of income

Amount of income

TDS on such amount, if any

Schedule FSI:

Details of Income from outside India and tax relief

Country Code

Taxpayer Identification Number

Head of income

Income from outside India (included in PART B-TI)

Tax paid outside India

Tax payable on such income under normal provisions in India

Tax relief available in India (e)= (c) or (d) whichever is lower

Relevant article of DTAA if relief claimed u/s 90 or 90A

Schedule TR:

Summary of tax relief claimed for taxes paid outside India

1 Summary of Tax relief claimed

2 Total Tax relief available in respect of country where DTAA is applicable (section 90/90A)

3 Total Tax relief available in respect of country where DTAA is not applicable (section 91)

4 Whether any tax paid outside India, on which tax relief was allowed in India, has been refunded/credited by the foreign tax authority during the year?

Schedule FA:

Details of Foreign Assets and Income from any source outside India

A1 Details of Foreign Depository Accounts held (including any beneficial interest) at any time during the relevant accounting period

A2 Details of Foreign Custodial Accounts held (including any beneficial interest) at any time during the relevant accounting period

A3 Details of Foreign Equity and Debt Interest held (including any beneficial interest) in any entity at any time during the relevant accounting period

A4 Details of Foreign Cash Value Insurance Contract or Annuity Contract held (including any beneficial interest) at any time during the relevant accounting period

B Details of Financial Interest in any Entity held

C Details of Immovable Property held

D Details of any other Capital Asset held

E Details of account(s) in which you have signing authority held (including any beneficial interest) at any time during the relevant accounting period and which has not been included in A to D above.

F Details of trusts, created under the laws of a country outside India, in which you are a trustee, beneficiary or settlor

G Details of any other income derived from any source outside India which is not included in,- items A to F above and, (ii) income under the head business or profession

Schedule 5A:

Information regarding apportionment of income between spouses governed by Portuguese Civil Code

Name of the spouse

PAN of the spouse

Heads of Income

Income received under the head

Amount apportioned in the hands of the spouse

Amount of TDS deducted on income at (ii)

TDS apportioned in the hands of the spouse

Schedule AL:

Assets and Liabilities at the end of the year (applicable in a case where the total income exceeds Rs.50 lakh)

A Details of immovable assets

B Details of movable assets

C Liabilities in relation to Assets at (A + B)

Part B-TI: Computation of Total Income

The information regarding total income is enclosed with the following details of the taxpayer to furnish with:

Salaries

Income from house property

Capital gains

Income from other sources

Losses of the current year set off

Balance after set off current year losses

Brought forward losses set off

Gross Total income

Income chargeable to tax at the special rate under section 111A, 112 etc

Deductions under Chapter VI-A

Total income

Income chargeable to tax at special rates and included in the above point

Net agricultural income/ any other income for rate purpose

Aggregate income

Losses of the current year to be carried forward

Deemed income under section 115JC

Part B-TTI: Computation of tax liability on total income

The information regarding the Computation of tax liability on total income is enclosed with the following details of the taxpayer to furnish with:

Tax payable on total income

Rebate under section 87A

Tax payable after rebate

Surcharge

Health and Education Cess

Gross tax liability

Gross tax payable

Credit u/s 115JD of tax paid in earlier years

Tax payable after credit u/s 115JD (8 – 9)

Tax relief

Net tax liability

Interest and fee payable

Aggregate liability

Taxes Paid

The amount payable/refundable

Refund

Details of all Bank Accounts held in India at any time during the previous year

Do you at any time during the previous year

(i) hold, as beneficial owner, beneficiary or otherwise, any asset (including financial interest in any entity) located outside India; or

(ii) have signing authority in any account located outside India; or

(iii) have income from any source outside India?

20 If the return has been prepared by a Tax Return Preparer (TRP) give further details below:

Identification No. of TRP

Name of TRP

Counter Signature of TRP

21 If TRP is entitled for any reimbursement from the Government, amount thereof 21

22 TAX PAYMENTS

A Details of payments of Advance Tax and Self-Assessment Tax B Details of Tax Deducted at Source from Salary [As per Form 16 issued by Employer(s)]

Verification: There will be verification at the end of all the General, Part B TI and Part B TTI ensuring that the details given are factually correct and self-attested by the taxpayer.

Income Tax Return 2 Form Filing Mode

An ITR-2 form can be furnished either in online or offline mode. In online mode, either XML needs to be uploaded or client can directly login to income tax portal and select the submission mode as “prepare and submit online”. In the case of online filing, some data can be imported from the latest ITR or form 26AS. Super senior citizens (Age of 80 years or more) are exempted from the online filing of ITR. Offline here means to furnish the return form in paper format.

Online:

While furnishing ITR-2 online, feed the details and e-verify return using EVC via Bank Account/Net Banking/Demat Account/Aadhar OTP or

2. Feed the details using electronic medium and send a physical copy of ITR V to Centralized Processing Centre (CPC), Bengaluru through speed post or normal post. When you furnish the ITR-2 return form using electronic medium, the receipt will be seen in the inbox of the registered email id. It can also be downloaded from the official income tax website manually. After downloading the acknowledgement, you need to sign the form and then send CPC office, Bangalore before completing 120 days counting from the e-filing date. On the other side, it is not required to send the ITR V to the CPC if EVC/OTP option is used

Offline:

If the age of the person is 80 or more years during the respective tax period or in the previous year, he/she can opt for offline return filing.

Modifications In ITR 2 For Assessment Year AY 2019-20:

Pensioners column has been added in the nature of employment.

A new deduction of 80TTB has been added in the deductions column.

From this assessment year, assesse is required to disclose his Directorship in Unlisted Company if any. Assesse has to provide the name of the Company, it’s PAN and his Director Identification Number

Assesse is required to provide details of shareholding of Unlisted Company wherein he has to provide all the details of shares purchased and sold during the financial year.

Facility of filing paper returns will now be available only to those over 80 years.

Those in possession of foreign assets will need to provide detailed disclosure of foreign depository account, foreign custodian accounts, equity and debt interest and particulars of overseas cash value insurance contract or annuity contract.

Taxpayers having agricultural income will have to provide additional details, including land measurement in acres, the name of the district along with Pincode in which the land is located, quality of land mentioning whether the land is irrigated or rain-fed etc.and whether the land is owned or held on lease.

Income received from the residential house properties would have to furnish details such as Tenant Name, PAN or TAN Number.

{kind=link}

{kind=link}

{kind=link}

{kind=link}