Providing a sigh of relief to exporters, the centre announced to pay the input tax credit (ITC) refunds of state taxes which will translate into lesser transaction time and costs. while the manual interface is being said under processing.

As the industry claims, there is a huge difference between the amount claimed for ITC to amount sanction amount for state goods and services tax (SGST) from central tax authority to the amount actually payout.

As proposed in the 2019-20 budget, “The central government has been authorised to pay the amount of refund towards state taxes to the taxpayers”. Till now, the central tax officer received claim filing for a refund, was responsible for payment of half of the amount and later the file passed to the state tax authorities for sanctioning of the remaining amount which leads to more time-consuming in refund claim and sanction process.

Not even this, the partly electronic and partly manual nature of ITC claim process also makes it time-consuming for the exporters. They have to file refund application at the portal and further to provide its printout along with acknowledgement and necessary documents in hard copy to the GST authorities. The documents set also vary from authorities to authorities. This manual interface of ITC return claim results increases transaction time and cost.

Mr Ajay Sahai, director general at Federation of Indian Export Organisations said, “The states and Centre did their own respective approval of ITC refund but now only one will approve both. This is a relief for exporters as it would reduce transaction time and costs”.

Centre granted relaxation for exporters who have to combat with stringent credit norms amid slow pace global trade growth. In December 2018, sanctioned export credit amount to exporters was accounted INR 7.38 lakh crore, translates into a fall of 20% on Year on Year basis. The PSU banks’ share in amount sanctioned as export credit has been reduced from 65% in FY 16 to 45% in FY 18.

In addition to this, exporters revealed a huge difference in the number of filed refund application on the portal and processed to the state tax office.

As per a tax expert, “The ability for Centre to give the refund for both the CGST and SGST will ease the problems being faced currently especially by the exporters and remove the delay in getting the entire cash post the sanction of refunds”.

Under the provisions of Section 194C and Section 194J, an individual or HUF are not liable to pay tax if they are not liable to get the tax audited under Section 44AB(a)/44AB(b).

So, an individual or HUF need not get the tax deducted from the payment which they made to contractor or professional for the services received exclusively for personal benefits and for the business/profession if the payer is not subject to tax audit under section 44AB(a)/(b).

This exemption led the substantial payments, which were made by individuals or HUFs for contractual work or professional services, out of TDS ambit which further led the loophole for tax evasion.

Amendment for a New TDS Section 194M

So a proposal has been made to add a new section- Section 194M in the act for levying 5% TDS on the amount paid or credited for the contractual work, including the supply of labour for any work, or professional fees in a year by an individual or a HUF if aggregate annual amount is more than Rs. 50 lakhs.

It should be noted that it excludes the individuals who need to get the tax deducted as per the provisions of section 194C or section 194J. However, to abbreviate the compliance burden, an amendment is proposed which states that such individuals or HUFs can deposit the tax deducted using their PAN and will not have to mandatorily obtain the TAN. This amendment will come into effect from 1st September 2019.

Meaning of Work, Contract and Professional Services for the Purpose of this Section

Cause (iii) and Clause (iv) of the Explanation to Section 194C defines the meaning of “contract” and “work” for the purpose of TDS deduction, while clause (a) of the Explanation to section 194J defines the meaning of professional services for the same purpose.

Procedural Aspects of TDS Section 194M

Let’s have a look on the procedural aspects of TDS section 194M given below:

Challan-cum-statement for TDS Payment u/s 194M

Under section 194IB, there is challan-cum-statement in Form 26QC for the payment of TDS by individual or HUF paying a monthly rent of more than Rs 50,000. Under section 194IA, there is challan-cum-statement in Form 26QB for the payment of TDS by a person paying consideration for the transfer of immovable property of 50 lacs or above. Similarly, Govt. may prescribe challan-cum-statement for the payment of TDS under the new section 194M.

Nil / Lower TDS Certificate Under Section TDS 194M

Under Section 197, a deductee can apply for nil or lower TDS certificate if his estimated tax liability approves no or tax deduction. The scope of Section 197 has been extended to this provision. So a payee can make an appeal to the Assessing Officer regarding obtaining such certificate for the amount paid or payable which are subject to TDS u/s 194M.

Due Date Under TDS Section 194M

Under section 194M, no due date has been prescribed separately for depositing the tax deducted. So, the due dates for the TDS payment under the new Section 194M shall remain the same, i.e., the timeframe of 30 days from the end of the month in which tax is deducted.

Note: Liability for tax audit and purpose of maying payment plays an insignificant role in TDS payment under section 194M

GST practitioner is personnel who is approved by the government (state or central) to take charge of all the tax-related activities on behalf of taxpayers and business firm. GST practitioner is a person concerned for fresh registrations under GST, applying for amendments or cancellation of registration. No shells of GST are left uncovered for a GSTP.

He is the one responsible for all the detailing like monthly, quarterly or annual returns of the business unit or furnishing of ITR on a taxpayer’s behalf. He represents the company on legal grounds and takes the sole credibility for any legal action of the company.

Whether it is Tax Deducted at Source (TDS) or Tax Collected at Source (TCS) or Non-Resident Taxable Person (NRTP) or OIDAR or UN Body or Embassy or ONP, a taxpayer (individual or business unit) needs a GST practitioner to file all the necessary Amendments of Registration of Core and Non-Core fields.

To be noted – GST officer can only make necessary changes and save in the drafts which enable the taxpayer to further work on the basis of the drafts saved. Final application has to be filed by the taxpayer.

What a GST practitioner can do in favour of a taxpayer?

Amendments of Registration – GSTP is responsible to generate an application for amendments of registration, filing clarifications, Composition Levy, the official cancellation of the registration and save it for later proceedings by the taxpayers. He is also concerned with tracking of application status.

Ledger Tasks – GSTP can examine Electronic Cash Ledger, Electronic Credit Ledger, and Electronic Liability Registers on behalf of the taxpayer. This helps the taxpayer to keep a record of all the GST payments he has done in the past.

Keeping a track of returns – On taxpayer’s behalf, GSTP can check Return Dashboard, transition forms, ITC forms, and return status. They can even prepare Annual Returns along with different other returns (including invoice uploading).

Payments – GSTP can see the taxpayer’s Saved challans and History of other challans on GST portal. It is possible to partially create a challan and save. To be noted, the challan generated by the GST Practitioner can be utilized by the taxpayer on later stages.

User Applications – A GSTP can create a new application for advance Ruling, Rectifying Order, Form DRC-03, Letter of Undertaking, Restoration of Provisional Attachment, Deferred Payment, Instalments to be paid in future, Provisional Assessment ASMT-01. He can check all new, old and submitted applications.

He can download certificates, check the clause list, look for six-digit HSN code or Service Classification Code.

Refunds – GSTP can help taxpayers with checking saved or filed refund applications, keeping the update of refund application status preparing a refund application, track refund application status.

Above mentioned are the business which a GST practitioner can perform on GST portal on a taxpayer’s behalf.

To keep in mind, GST practitioner can save a partial application as a draft. It is the taxpayer who has to file an application using those drafts.

GST practitioner is personnel who is approved by the government (state or central) to take charge of all the tax-related activities on behalf of taxpayers and business firm. GST practitioner is a person concerned for fresh registrations under GST, applying for amendments or cancellation of registration. No shells of GST are left uncovered for a GSTP.

He is the one responsible for all the detailing like monthly, quarterly or annual returns of the business unit or furnishing of ITR on a taxpayer’s behalf. He represents the company on legal grounds and takes the sole credibility for any legal action of the company.

Whether it is Tax Deducted at Source (TDS) or Tax Collected at Source (TCS) or Non-Resident Taxable Person (NRTP) or OIDAR or UN Body or Embassy or ONP, a taxpayer (individual or business unit) needs a GST practitioner to file all the necessary Amendments of Registration of Core and Non-Core fields.

To be noted – GST officer can only make necessary changes and save in the drafts which enable the taxpayer to further work on the basis of the drafts saved. Final application has to be filed by the taxpayer.

What a GST practitioner can do in favour of a taxpayer?

Amendments of Registration – GSTP is responsible to generate an application for amendments of registration, filing clarifications, Composition Levy, the official cancellation of the registration and save it for later proceedings by the taxpayers. He is also concerned with tracking of application status.

Ledger Tasks – GSTP can examine Electronic Cash Ledger, Electronic Credit Ledger, and Electronic Liability Registers on behalf of the taxpayer. This helps the taxpayer to keep a record of all the GST payments he has done in the past.

Keeping a track of returns – On taxpayer’s behalf, GSTP can check Return Dashboard, transition forms, ITC forms, and return status. They can even prepare Annual Returns along with different other returns (including invoice uploading).

Payments – GSTP can see the taxpayer’s Saved challans and History of other challans on GST portal. It is possible to partially create a challan and save. To be noted, the challan generated by the GST Practitioner can be utilized by the taxpayer on later stages.

User Applications – A GSTP can create a new application for advance Ruling, Rectifying Order, Form DRC-03, Letter of Undertaking, Restoration of Provisional Attachment, Deferred Payment, Instalments to be paid in future, Provisional Assessment ASMT-01. He can check all new, old and submitted applications.

He can download certificates, check the clause list, look for six-digit HSN code or Service Classification Code.

Refunds – GSTP can help taxpayers with checking saved or filed refund applications, keeping the update of refund application status preparing a refund application, track refund application status.

Above mentioned are the business which a GST practitioner can perform on GST portal on a taxpayer’s behalf.

To keep in mind, GST practitioner can save a partial application as a draft. It is the taxpayer who has to file an application using those drafts.

It is a moral duty of every organization and taxpayer to file an income tax return and pay the taxes. Recently the budget 2019 income tax amendments have stated that the ITR is important to be filed in case the electricity bill is more than 1 lakh and more than 2 lakh for foreign travel expense. The income tax return form 7 is to be filed by all the Charitable /Religious trust u/s 139 (4A), Political party u/s 139 (4B), Scientific research institutions u/s 139 (4C), University or Colleges or Institutions or Khadi and Village industries u/s 139 (4D). These organizations have to file the form for claiming the exemptions.

What is ITR 7 Form?

The Firms, Companies, Local authority, Association of Person (AOP) and Artificial Judiciary Person are eligible for filing Income Tax Return through ITR-7 Form if they are claiming exemption as one of the following categories:

Under Section 139 (4A)- if they earn from a charitable /religious trust

Under Section 139 (4B)- if they earn from a political party

Under Section 139 (4C)- if they earn from scientific research institutions

Under Section 139 (4D)- if they earn from university or colleges or institutions or khadi and village industries

Who are Not Eligible to File ITR 7 Form Online?

Taxpayers who are not claiming exemption under Section 139 (4A), Section 139 (4B), Section 139 (4C) or Section 139 (4D) are not liable to file ITR-7 Form for Income Tax Return.

What is the Eligibility Criteria for Filing Online ITR 7 Form?

Any taxpayer can use ITR-7 Form for filing Income Tax Return if they file as a Trust, Company, Firm, Local authority, Association of Person (AOP) or Artificial Judicial Person and claims exemption under Section 139 (4A), Section 139 (4B), Section 139 (4C)or Section 139 (4D).

What is the Last Date for Filing ITR 7 Form?

The due date for filing ITR-7 Form is different depending upon the audit of the accounts. Tax Assessees whose accounts are required to be audited can file till 30th September while those whose accounts are not required to be audited can file until 31st July.

Name (as mentioned in deed of creation/ establishing/ incorporation/ formation)

PAN

Flat/Door/Block No

Name Of Premises/Building/Village

Date of formation/incorporation

Road/Street/Post Office

Area/Locality

Office Phone Number with STD code/Mobile No. 1

Fax Number/Mobile No. 2

Email Address 1

Email Address 2

Whether any project/institution is run by the assessee? (Yes/No) If Yes, then please furnish the details: Details of the projects/institutions run by you

Details of registration or approval under the Income-tax Act (Mandatory, if required to be registered)

Details of registration or approval under any law other than Income-tax Act

Filing Status

Return filed u/s (Tick)

Return furnished under section

139(4A)

139(4B)

139(4C)

139(4D)

Others

If revised/ defective/Modified, then enter Receipt No. and Date of filing original return (DD/MM/YYYY)

If filed, in response to a notice u/s 139(9)/142(1)/148/153A/153C or order u/s 119(2)(b), enter date of such notice/order, or if filed u/s 92CD enter date of advance pricing agreement

Residential status?

Resident

Non-resident

Whether any income included in total income for which claim under section 90/90A/91 has been made?

Whether this return is being filed by a representative assessee?

Whether you are Partner in a firm?

Whether you have held unlisted equity shares at any time during the previous year?

Schedules To The Return Form (Fill As Applicable)

Schedule I: Details Of Amounts Accumulated / Set Apart Within The Meaning Of Section 11(2)) Or In Terms Of Third Proviso To Section 10(23C)

Schedule J: Statement Showing The Funds And Investments As On The Last Day Of The Previous Year [To Be Filled If Registered under Section 12A/12Aa Or Approved Under Section 10(23C)(Iv)/10(23C)(V)/ 10(23C)(Vi)/10(23C)(Via)/10(21)]

Schedule K: Statement Of Particulars Regarding The Author(S) / Founder(S) / Trustee(S) / Manager(S), Etc., Of the Trust Or Institution (To Be Mandatorily Filled In By All Persons Filing Itr-7)

Schedule LA: Political Party

Schedule ET: Electoral Trust

Schedule VC: Voluntary Contributions (To Be Mandatorily Filled In By All Persons Filing Itr-7)

Schedule AI: Aggregate Of Income Derived During The Previous Year Excluding Voluntary Contributions [To Be Filled By Assesses Claiming Exemption U/S 11 And 12 Or U/S 10(23C)(Iv)/(V)/(Vi)/(Via)]

Schedule ER: Revenue Expenditure Incurred During The Year And Amount Applied To Stated Objects Of The Trust/Institution During The Previous Year – Revenue Account [To Be Filled By Assessee Claiming Exemption U/S 11 And 12 Or U/S 10(23C)(Iv),(V),(Vi),(Via)]

Schedule EC: Amount Applied To Charitable Or Religious Purposes In India Or For The Stated Objects Of The Trust/Institution During The Previous Year–Capital Account [Excluding Amount Exempt U/S 11(1A)] [To Be Filled By Assesses Claiming Exemption U/S 11 And 12 Or U/S 10(23C)(Iv)/(V)/(Vi)/(Via)]

Schedule IE- 1: Income & Expenditure Statement (Applicable For Assessees Claiming Exemption Under Sections 10(21), 10(22B), 10(23Aaa), 10(23B), 10(23D), 10(23Da), 10(23Ec), 10(23Ed), 10(23Ee), 10(29A), 10(46), 10(47) And Other Clauses Of Section 10 Where Income Is Unconditionally Exempt)

Schedule IE- 2: Income & Expenditure Statement (Applicable For Assessees Claiming Exemption Under Sections 10(23A), 10(24)

Schedule IE- 3 Income & Expenditure Statement (Applicable For Assessees Claiming Exemption Under Sections 10(23C)(Iiiab) Or 10(23C)(Iiiac) (Please Fill Up Separate Schedule For Each Institution):

Schedule IE- 4 Income & Expenditure Statement (Applicable For Assessees Claiming Exemption Under Sections 10(23C)(Iiiad) Or 10(23C)(Iiiae)( (Please Fill Up Separate Schedule For Each Institution):

Schedule HP: Details Of Income From House Property (Please Refer To Instructions) (Drop Down To Be Provided Indicating Ownership Of Property)

Schedule CG: Capital Gains

Schedule OS: Income From Other Sources

Schedule OA: General

Schedule BP: Computation Of Income From Business Or Profession

Schedule CYLA: Details Of Income After Set-Off Of Current Years Losses

Schedule PTI: Pass-Through Income Details From Business Trust Or Investment Fund As Per Section 115Ua, 115Ub

Schedule SI: Income Chargeable To Tax At Special Rates

Schedule 115TD: Accreted Income Under Section 115Td

Schedule FSI: Details Of Income From Outside India And Tax Relief

Schedule TR: Summary Of Tax Relief Claimed For Taxes Paid Outside India

Schedule FA: Details Of Foreign Assets And Income From Any Source Outside India

Schedule SH: Shareholding Of Unlisted Company

Part B – TI Statement Of Income For The Period Ended On 31St March, 2019

Voluntary Contributions other than Corpus fund

Voluntary contribution forming part of corpus [(Ai + Bi) of schedule VC]

Aggregate of income referred to in sections 11, 12 and sections 10(23C)(iv), 10(23C)(v), 10(23C)(vi) and 10(23C)(via) derived during the previous year excluding Voluntary contribution included in 1 and 2 above (10 of Schedule AI)

Application of income for charitable or religious purposes or for the stated objects of the trust/institution:

Additions

Income chargeable u/s 11(4) [as per item No. E36 of Schedule BP]

Total (2+3-4viii+5viii+6)

Amount eligible for exemption under sections 10(21), 10(22B), 10(23A), 10(23AAA),10(23B), 10(23EC), 10(23ED), 10(23EE), 10(29A)

Amount eligible for exemption under section 10(23C)(iiiab), 10(23C)(iiiac), 10(23C)(iiiad), 10(23C)(iiiae), 10(23D), 10(23DA), 10(23FB), 10(24), 10(46), 10(47)

Amount eligible for exemption under any other clause of section 10 (other than those at 8 and 9)

Income chargeable under section 11(3) read with section 10(21)

Income claimed/ exempt under section 13A in case of a Political Party

Income claimed/ exempt under section 13B in case of an Electoral Trust (item No. 6vii of Schedule ET)

Income not forming part of item No. 7 to 12 above

Gross income [7+11+13v-8-9-10-12a-12b]

Losses of current year to be set off against 13v (total of 2ix, 3ix and 4ix of Schedule CYLA)

Gross Total Income (14-15)

Income chargeable to tax at special rate under section 111A, 112 etc. included in 16

Deduction u/s 10AA

Total Income [16-18]

Income which is included in 19 and chargeable to tax at special rates (total of col. (i) of schedule SI)

Net Agricultural income for rate purpose

Aggregate Income (19-20+21) [applicable if (19-20) exceeds maximum amount not chargeable to tax]

Anonymous donations, included in 22, to be taxed under section 115BBC @ 30% (Diii of Schedule VC)

Income chargeable at maximum marginal rates (22-23)

Part B – TTI Computation of tax liability on total income

Tax payable on total income

Surcharge

Health and Education cess @ 4% on (1f+ 2iii)

Gross tax liability (1f+ 2iii + 3)

Tax relief

Net tax liability (4 – 5c)

Interest and fee payable

Aggregate liability) (6 + 7e)

Taxes Paid

Amount payable (Enter if 8 is greater than 9e, else enter 0)

Refund(If 9e is greater than 8) (refund, if any, will be directly credited into the bank account)

Details of all Bank Accounts held in India at any time during the previous year (excluding dormant accounts) (In case of nonresidents, details of any one foreign Bank Account may be furnished for the purpose of credit of refund)

Do you at any time during the previous year

14 Tax Payments

Details of payments of Advance Tax and Self-Assessment Tax

Details of Tax Deducted at Source (TDS) on Income [As per Form 16 A issued or Form 16B/16C furnished by Deductor(s)]

Details of Tax Collected at Source (TCS) [As per Form 27D issued by the Collector(s)]

Verification

I, son/ daughter of, solemnly declare that to the best of my knowledge and belief, the information is given in the return and the schedules, statements, etc. accompanying it is correct and complete is in accordance with the provisions of the Income-tax Act, 1961. I further declare that I am making this return in my capacity as _________________ and I am also competent to make this return and verify it. I am holding permanent account number (if allotted) (Please see instruction). I further declare that the critical assumptions specified in the agreement have been satisfied and all the terms and conditions of the agreement have been complied with. (Applicable, in a case where the return is furnished under section 92CD) Place……. Date…… Sign here……

GST was always an ambitious plan when one takes into consideration the diversity that India as a nation subsumes within its territorial boundaries. From conflicted Kashmir in North to Kanyakumari in the south and Kutch in East to hills of Arunachal in the west, Indian Subcontinent witnesses a diversity matched by no other nation on the planet. Hence, a unified tax system was always going to take months of drafts coupled with frequent editions to bring one and all on board.

Hence, the Central Governments successful effort of drawing a consensus within a three month period deserves praise and accolades. However, a common agreement that binds all states of India to the GST is the compensation agreement between the state and the Central Government.

This agreement ensures that the Centre will compensate for the initial losses accrued by states as a result of GST implementation. It has been more than a year since the new tax law was introduced and that states and union territories have been paid Rs 52,077 crore in compensation during the period. Experts believe that this agreement coupled with the center’s recent decision of GST tax relaxation on essential goods and services in the light of increasing GST accrues could be a recipe for disaster.

One key highlight from the current fiscal year is that of the states reporting shortfall in revenue of up to 43%. This was a topic of discussion in the last GST Council meeting as well. Amidst these recurring state losses, the center’s decision to relax GST rates will only burden states further. This could mean more revenue loss and greater compensation cheques for the Central Government. Unless GST accrues increase drastically, the tax black hole will only get bigger and denser by each fiscal quarters,

The Economy Softpoints:

Non-buoyant Revenues

The tax base has no doubt increased but tax revenues have remained the same or gained small spikes. This is clearly evident in the monthly accrues for current Fiscal Year with that of previous. Hence GST revenues it seems will make up little for the increased compensation burden post rate relaxations.

Tax Evasions

NAA State bodies in 17 of the 29 states have reported zero cases of anti-profiteering may reflect a robust center-state machinery. However, beneath the surface, there are reports of new adaptive methods of tax evasions. This cannot be entirely faulted on the administration alone. GST is a complete technology reliant tax mechanism. Hence, it will not err as long as people and businesses adhere to the rules in a straight line. But human nature is unpredictable. Especially when they have been used to open hand tax evasions in the previous regimes.

The Prime Minister Narendra Modi states GST as a celebration of Honesty. In some way, we can regard that the failure of GST will more due to the will of the people than the administration. And this is absolutely right.

The GSTN Network can no doubt be used to check false practices via sellers and buyers invoices matching. However, in a country like India where 95% of the tax collections come from a meager 5% of the businesses, invoice matching is a partial solution to long-standing issues that till date are used to bypass as well as benefit from GST complexities by businesses of all size and scale.

These practices include:

Misclassification of Goods and Services

Under and Over invoicing of their sales and purchases

Fake invoices for overheads, like transportation, entertainment and so on

Manipulation and bypassing complex rules which are hard to scrutinize and detect at a single glance.

The above issues contribute greatly to India’s long flourishing yet unchecked black money assets as well as the branches of the indirect economy. Hence, Demonetisation despite the naysayers was a strong counter administrative move to lay the ground for GST embracement by India as a nation. However, for this to have completely gone as planned, a more simple and easy compliant GST could have better placed both states and the Centre to accelerate adoption.

A golden example is that of the e-Way bill which by far appears to be the most leak-proof and technically efficient Central Scheme to come into effect till date to track the movement of goods and check black income generation has been accused guilty of reinstating the yesteryears Inspector Raj. But this a narrative that the so-called blue-collar media will use every day. A greater question that remains unquestioned is the willingness of the people to abide by the new norms and participate in Nation Growth. However, this would need a complete overhaul of the present pay structure and power centers in the Police Administration. This would indirectly burden the state finance machinery. A ying-yang point of modern Indian Politics-Administration to say the least.

In conclusion, the success of Demonetisation will always be questioned by one and all which includes the modern-day media puppets as well as political foes too. GST is to early to be evaluated and certified. The GST rate relaxation is more a political necessity than an economic one. However, for the greater good of the Nation that even eclipses the outcome of the upcoming elections, it is important that India as a Nation wakes to the call for a more self-policing and honesty adhering nation. And GST even though troubled by complexities and ambiguities offers a faint little yet plausible opening to that reality where India acts a United Nation with one and only goal of ‘development for the people, of the people and by the people’.

One of the Kirana merchants who is engaged in the business of selling pulses, spices, and dry fruits in the APMC market, in Vashi Mumbai, doesn’t seem to people these days with the current GST system enforced by the central government.

This particular medium scale retailer has been active in APMC, Mumbai, for the last three decades but expressed deep melancholy when discussed about his business sales figures in the past three years.

The APMC trader stated, “There is no demand, the big malls are pulling away our customers. We used to do Rs 2 lakh business on a daily basis; we are not even doing Rs 50,000 these days.”

The APMC merchant business has been performing poorly in the past two years due to steep competition and a general slowdown in consumption by Indian customers. This small merchant is also facing intense competition from both large online & offline retailers.

To be more specific, the introduction of Goods and Service Tax (GST) by the central government alongside the promotion of digital transactions has worsened the situation of mostly every small & medium scale traders in India, who transacts in cash daily and find it difficult to file GST returns. “We are not against GST, but we expect the government to simplify the filing procedure,” said the APMC retailer.

To add more, the increasing usage of digital wallets and electronic swiping machines post demonetization has been made it difficult for the small traders to stay in the market.

The APMC trader, on this issue, said, “I find it difficult or most uncomfortable with using cards and electronic payment systems, for small traders like us, cash is easier and way to go in business.”

Those who don’t know, APMC market in Mumbai is one of the largest wholesale market in Asia, spread across 300 hectares, where traders deal in fruits, pulses, vegetables, food grains, onion and potato, spices, and sugar. It is an evergrowing place where farmers sell their produce whereas wholesalers & retailers sell farmer-sourced items to general customers. Although, the imposition of the GST system, steep competition from large multi-chain retailers, and economic slowdown has put down brakes on the business profits of small traders here.

Well, it’s not only this particular small trader from APMC market in Mumbai who has found it difficult to deal with the GST burst, but other traders in the country also have similar tales.

A similar situation has been faced by small & medium traders in other retail sectors too. For instance, an anonymous trader from fast-moving consumer goods (FMCG) section at Dana Bazar expressed his grief that with the current GST regime, he always needs a tax expert & accountant for the bookkeeping purpose, in an attempt to make consistency while filing his tax returns.

“Tax filing under the new GST system is not at all easy, and we always need a tax expert to fulfil that purpose. It had increased our costs, while our business hasn’t seen any improvement,” said the anonymous FMCG trader at Dana Pani. The business of this particular FMCG trader has dropped 20 per cent as expressed by him.

Similarly, a rice & wheat trader, who wanted to stay unidentified said, “The traders were never ready, when GST was introduced, as most of us have never used computers. Glitches were evident in the GST portal, classification of goods and their tax slabs was unclear, refunds were not easily coming and return forms were complicated too.”

The unnamed rice & wheat trader, further said, “I agree that situation has improved now, but still it would be better if the government work towards a more simpler tax filing system. We all want to see GST consolidation under three slabs of zero percent, five percent, and 16 percent.”

The life of small traders has not been easy at all with the current GST system imposed by the ruling party, i.e., BJP and majority of the ruling NDA government in the country.

There are close to seven crore small and medium scale traders in the country who offers employment to approx 45 crore people in India by generating an overall net business profit of INR 42 lakh crores. Despite this, the community feels that they were sidelined by the governed without putting their interests on the table. They also feel dejected due to the witch-hunt on them by tax authorities.

Keeping the small & medium traders interest in the account, the central government this year has double the exemption limit for traders who have an annual turnover between INR 20 lakh to 40 lakh. To decrease the compliance burden, the eligibility for composition scheme has also been stretched till 1st April 2019 for the small businesses having an annual income of INR 1.5 crores. Traders enrolled under GST composition scheme are now allowed to file their annual returns on a quarterly basis.

Despite such efforts, the traders are still ungratified and want the government to do more. The proposal for simplification in the filing of GST returns has been recently put forward by The Confederation of All India Traders (CAIT), who represents the country-wide traders on a big stage.

CAIT is in constant talks with the current ruling government and newly appointed Finance Minister to stretch the tax exemption limit from INR 2.5 lakh to somewhere between INR 5 lakh to 7 lakh for small & medium traders, owing to constantly increasing consumer index price in past many years. Apart from this, CIAT has also forced the central government to fulfil its promise of offering INR 50 lakh loan without any collateral for small & medium traders.

The Indian small & medium traders are also demanding the ruling government to stop permitting the foreign direct investment in the retail & e-commerce sector, eating a vast chunk of their business currently.

Government is pressing pedals to curb tax evasion by widening the taxpayer base and by augmenting the class of people for compulsory filing of ITR. According to the official data, the total number of income tax returns (ITRs) filed in 2017-18 is 6.86 crore which registers an elevation of 23 per cent over the last year. This apparently shows the improvement in tax compliance in the last few years. But in the nation with a population of approx 130 crores, the Government further sees more scope of improvement and so it is eyeing on taking high-value transactions in consideration for ITR filing.

“People evading tax have to be dealt with differently. The 2 per cent TDS (in case of withdrawal of more than ₹1 crore cash from a bank account in a year) is actually for those who are getting away. You must have seen in the budget that there are several measures such as those whose electricity bill is more than ₹1 lakh would need to file the return. We may notify some other class of people who would be required to file tax returns,” said Ajay Bhushan Pandey, Revenue Secretary.

Under the proposed Union Budget for 2019-20, filing an ITR becomes mandatory for the individuals whose annual deposit in a current account is more than ₹1 crore, whose foreign travel expenses are more than ₹2 lakh or whose annual electricity bill expenses is more than ₹1 lakh. According to the experts, high hotel bills, hefty expenditures incurred on party or buying a car may also require people to file ITR.

“The government has already said that those doing high-value transactions would be covered. The next could be high hotel bills, clubs, expenditure on holding a party, purchase of cars and investment above a certain level,” said Riaz Thingna, Director, Grant Thornton.

“If someone is buying a car for ₹5 lakh, it is unlikely that his income would be less than ₹5 lakh. Today, people are buying ₹75 lakh car and still not paying taxes. So, I think there are enough opportunities to take up so many different areas.” He added.

The Modi government has been continuously working against the generation of black money and it has taken many measures to transform the Indian economy into the cashless economy. Among them, demonetisation was the major step to discard the loopholes of tax evasion and avoidance. Now the next step adopted by the government is based on the principle of – “higher the earning higher the tax”.

As a result, the surcharge of 15 per cent has been elevated to 25 per cent for the individuals with annual income between ₹2 to ₹5 crore. Similarly, for those with the annual earnings of ₹5 crore or more, the surcharge has been raised from 15 per cent to 37 per cent. In this way, the effective tax rate will lift up to 39 and 42.74 per cent for those in the ₹2-5 crore and ₹5 crore & above income slab, respectively.

Fed up to the back teeth, big industrialists discontents the decision to which the Revenue Secretary argued in a defending way by giving an example of many countries like the US, France and China where the higher tax rate is liable on high earnings and proving that India still taxes its super-rich class at lower rates.

“In India, before the (proposed) increase, for the highest tax bracket, the tax rate was 35.8 per cent. In Brazil, it is 27.5 per cent. In Canada, it is 33 per cent plus 21 per cent state taxes. It is more than 45 per cent in China, 66 per cent in France and 50 per cent in the US,” Pandey explained.

He also explained that economic decisions are taken on the basis of overall economic conditions and not on the basis of if someone would take advantage of the provisions in an illegal way, in response to the apprehension that the increment in customs duty on gold would consequence smuggling, while confirming that enforcement agencies would handle the problem of gold smuggling.

“We should not be using our forex for non-essential imports. So, the proposal goes along with this policy. The issues related to smuggling or anything will be dealt with by the enforcement agencies,” the revenue secretary said.

The Modi-led government has recently announced that it will sort out all the major issues or glitches in the new GST system, which was also the key reason for the decline in indirect tax revenue.

At the time when the GST regime was launched, the government has promised that the full benefits of GST reform and revenue will take some time, and the stabilization phase will continue till FY 2019-20.

The GST collections recently show an alarming sign for the government as it has fallen below the INR 1 lakh crore threshold.

As per the data, the tax collection under GST has observed INR 99,936 crores in June 2019, which is way below the revenues of the last three months, i.e., INR 1,06,577 crores, INR 1,13,865, and INR 1,00,289 (from March to May respectively).

Although, the experts believe that GST collections are in line with the current pace of economic growth and are acceptable in terms of signifying the success of the new tax regime.

The disagreements over GST rates and procedural issues between the state and central government is one of the key reasons why the new tax system hasn’t stabilized yet.

Regular Demand for Reduction in GST Tax Rate

The demand for reduction in rates of GST has been seen across almost every industry where the GST is applicable to multiple product or services. As per the statistics, close to 1350 items are covered by GST, and a very high tax rate of 18 per cent is applicable for 632 items (46.8 % of the goods).

The government is working continually to reduce the GST rates as discussed by the new finance minister in her recent budget speech. But, given the shaky flow of indirect tax revenues, the further cut down in GST rate seems highly unlikely.

Complex GST Filing Procedure

The mess over the GST return filing procedure is yet to be solved by the central government.

In the recent budget speech, the finance minister, Nirmala Sitaraman has said that the government is working wholeheartedly to simply the GST process and return filing procedure. Actions like fully automated GST refunds module, tax filing through AADHAR, and simple monthly returns will be taken by the government to simplify the existing GST system. The new return system is scheduled to be rolled in phases from October 2019.

Inconsistent GST revenues

The inconsistent flow of GST revenue flow is forcing the government to look for the durable flow of direct taxes, i.e., personal and corporate taxes to achieve the target revenue for taxes. Given the current shaky scenario of GST revenues, the situation is likely to retain the same for the next two years.

As per the budget document, “Direct taxes are expected to show a growth rate of 13.4 per cent and 14 per cent compared with the previous year in 2020-21 and 2021-22, respectively. On the other side, the growth rate in indirect taxes is expected to be 7.3 per cent and 10.3 per cent in 2020-21 and 2021-22, respectively”.

Therefore, the government is relying heavily on direct tax collections to make up for the stumbling GST revenue. The direct tax-GDP ratio will easily reach 6.6 per cent of GDP in 2021-22.

For the filing of income tax returns, salaried individuals can utilize forms ITR-1 and ITR-2. The individual resident taxpayers with an annual income of up to INR 50 lakh are required to file ITR-1 while the others who do not earn from business or profession will go with the ITR-2 for filing income tax returns.

In the ITR-1, one can report details such as income from salary, income from other sources, one house property, and the income of up to INR 5k from agriculture. While the ITR-2 bounds individuals to mention information like income from more than one house property, unlisted equity shares, capital gains and directorship in any company.

Form 16 now keeps an improved salary TDS certificate which allows taxpayers for mentioning of more detailed information of provided several tax-exempt allowances and deductions under the income tax law. While the part B of Form 16 has also been rectified in order to mention particulars in details like the provided several rebates and deductions under the income tax law.

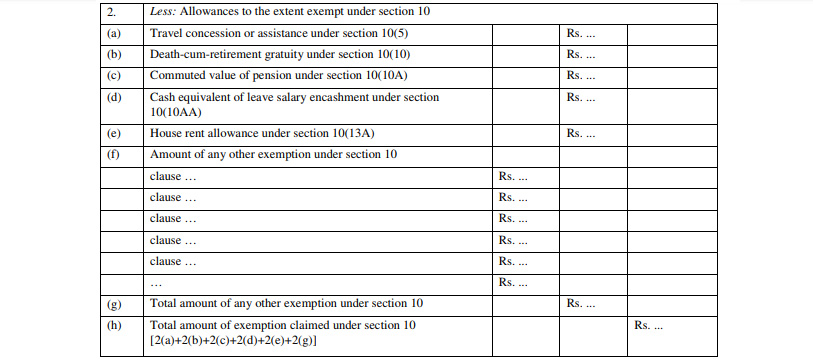

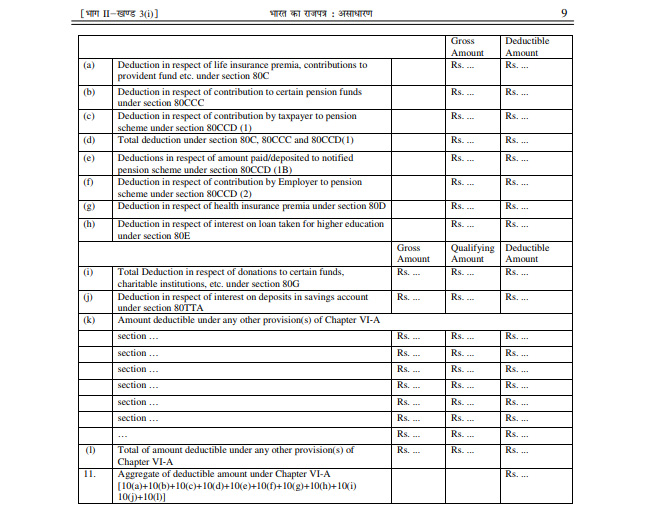

Given below are the snapshots of provided exemptions and deductions under the Income-tax law:

Exemptions Allowed

Deductions Allowed – Chapter VI-A

ITR Filing of Taxpayers:

ITR-1: The exact figures of the comprehensive sections of the salary are mustfill by the taxpayers such as

Salary

Perquisites

Profit instead of salary

In addition to this, all the exempted allowances under section 10 would also be required to be mentioned likewise

Gratuity

Leave travel allowance

House rent allowance

Along with it, there is a need for separate mentioning of allowed deductions under chapter VI-A from section 80c to 80U. For example

PPF investment, life insurance premium, tuition fee for children under section 80c.

Donations under section 80D

Medical insurance premium under section 80D

ITR-2: As like the ITR-1, while filing for the ITR-2, taxpayers required to mention all the exempt allowance and deductions in detail. In addition to this, there is a need for reporting complete break up of several aspects of salary which cumulatively makes a specific amount likewise salary, prerequisites and profits in place of salary. To get this information one can go through the annexure provided with Form 16 from an employer.

If in case, the taxpayers are getting a salary from more than one employers in a financial year, he/she requires to present employer wise details. With improved Form 16, one can easily report details of one or more employers while filing for the ITR-2.

The filling up of details required in ITR-1 and ITR-2 would no longer be a tedious task for employers. Because the revised Form 16 format to file ITR makes easier to get all the required details.

In case of filing for ITR via online mode, these details automatically occupied to your ITR which not only helps in reducing efforts but also guarantee an accurate e-filing.

Any Joint Development Agreement or JDA of commercial project or sale of development rights is not exempted from GST. For now, it is mandatory to clear all sorts of confusion on GST rates for Joint Development Agreement or development right sale, especially for commercial projects.

While certain exemptions are allowed for the transfer of development rights in a residential or housing JDA, commercial developments are denied of any exemptions. Clearly, because of the GST being imposed, the taxes on development in commercial projects is more than taxes on development in residential projects.

Hopefully, the issue will be considered by the Union Government and the transactions related to development rights will not be included under GST rather such transactions will come under the impact of immovable property.

If we talk about the transfer of development rights under joint development agreements, GST is imposed on the transfer of development rights by the landowner to the real estate developer. The category is clearly of indirect tax and should not be included under GST. So, this calls for the attention and re-examination on the Government’s part.

According to managing director of an organization; to effectively achieve the target of giving Housing To All by 2022, the Union Government must check the requirements of home loan borrowers. In addition, the government also needs to consider the issue of affordability and stamp-duty. All the issues related to affordability and stamp duty should be included in GST.

The point that needs to be instantly considered by the government is to increase the threshold amount of affordable housing under Pradhan Mantri Jan Awas Yojna (PMAY) scheme to Rs. 75 Lakhs which is presently Rs. 45 Lakhs. In today’s market, the prices of lands are touching skies, making it impossible for the developer to deliver homes at the cost of only Rs. 45 Lakhs.

As per the recent database, approx 85% of the housing projects land under Rs. 45 Lakhs to Rs. 75 Lakhs, therefore it is recommended that the carpet area threshold value of affordable housing should be increased from 60 sqr mtr to 90 sqr mtr in metropolitan cities and in non-metro cities 90 sqr mtr to 120 sqr mtr.

By redesigning the policies of threshold values under affordable housing, the government can pack the number of projects under ‘affordable housing’, thus ensuring the vast portion of the market to avail income tax benefits.