The government has announced a new feature into the GST system which will allow all the taxpayers to change the mobile number and email id of the particular taxpayers himself within the GST system.

The complaint earlier came in the scanner that most of the time authorized personnel who were designated for the application of registration had used their own contact details at the time of registration.

The finance ministry mentioned in the statement that, “the intermediaries who were authorized by them to apply for GST registration on their behalf had used their own email and mobile number during the process.”

This particular reason had let the government take such a technical step allowing taxpayers for modification in the contact details i.e. mobile number and email id.

Step by Step Procedure to Change Email ID & Mobile Number on Portal

The taxpayer will have to reach the applicable jurisdictional Tax Officer for the password of GSTIN allowed of his business

To check jurisdiction of the particular taxpayer one can log in to https://www.gst.gov.in where the jurisdiction allotted will be displayed in red text

The documents will be mandatorily required for the validation of its business according to its GSTIN

The tax officially will cross check the details and validate if the person is a stakeholder in the given GSTIN of business

The authentication will be done further after the tax office will upload the documents on the GST portal

Now the tax officer can modify the mobile number and email id of the taxpayers

After the documents uploading, the officer will reset the password for the GSTIN

The given email id will receive the username and temporary password

The login link can be used for the further modification of the password on GST portal login page https://www.gst.gov.in/

Finally, the taxpayer after login with a temporary password will be asked to change the username and password

The said procedure can be used for changing the old username and password by the taxpayer.

In the budget 2019, several GST related rules and regulations have changed which have been presented in the Finance Bill. Finance Minister Nirmala Sitharaman presented the budget 2019 on July 5, 2019. The budget promulgates the tax payment facilities in addition to the changes made in composition schemes. Most of the things presented in the Finance Bill are related to rules and regulations.

Changes in GST associated rules will increase taxpayers’ convenience while the introduction of the Amnesty Scheme will lead to the resolution of old cases.

GST council takes all the big decisions about GST in the presence of finance ministers of all states, wherein the President of this Council is the Finance Minister of the Central Government. All the decisions regarding the GST rate are taken in the GST council meeting.

List of All GST Changes Made in Budget 2019

Proposals regarding the cash transfer have also been made in the Finance Bill which proposes that from now on, any amount of taxes, interest, penalties and fees available in Taxpayers electronic cash ledger can be transferred as Central Tax, State Tax or Cess, subject to the condition that this amount should available in taxpayers’ electronic cash ledger.

Now taxpayers will be able to rectify the mistakes made during tax payments. New SubSection has been added to Section 49 of the CGST Act. Under this section, any tax or penalty which has been mistakenly paid in CGST by any registered person will now be able to get adjusted in IGST, SGST.

In the Finance Bill, it has been stated that interest will be charged only on the Net Tax liability. For instance, if a taxpayer’s liability is INR 1 lakh and he has an input tax credit of INR 50,000 and this taxpayer files a return after a fixed date, then interest will be charged only on INR 50,000 and not on INR 1 lakh.

If any company earns profits on speculation, then it will have to give 10 per cent of the profits as a penalty to the Anti-Profiteering Authority. The penalty must be given within 30 days of when Authority passes the order.

The option to fill the quarterly tax is also proposed in the Finance Bill. Now composition dealers will have to file the GST returns once a year and they can pay taxes on a quarterly basis. The other taxpayers who are filling monthly returns will be given the option to fill the UCO quarterly returns.

Another new proposal has been given in the Finance Bill which allows the Central Government to refund the amount of state tax to taxpayers.

The verification of the Aadhar card of all the taxpayers for GST has now become mandatory. Some taxpayers are kept out of this verification ambit.

The composition scheme has been provided for the people who supply intrastate goods or services and whose previous year turnover did not exceed Rs 50 lakh. 3 per cent GST rate is leviable it.

The budget also holds a proposal regarding the creation of a National Appellate Authority for Advance Ruling. If the appellate authority of 2 or more states gives separate rulings, then the National Appellate Authority will consider it.

Additionally, the new amnesty scheme under GST has been brought in the budget to resolve the old cases of service tax and excise. The name of this scheme is ‘Sabka Vishwas Legacy Dispute Resolution Scheme’. Under this scheme, the old cases related to these taxes will be resolved.

Apart from this, a 100 per cent discount will be allowed in late fees and a 70 per cent discount will be given in cases where there is a dispute regarding the tax figures. These benefits will be available only after the fulfilment of certain conditions.

SAG Infotech provides the best unlimited return filing, e-waybill, and billing GST software available for a free download. The Gen GST Version 2.0 software for FY 2019-20 being in-house developed by SAG Infotech which is a panacea for all the complex GST filing operations and tasks being assigned to the traders and business community by the government of India. It is available on both platforms i.e. desktop and online versions according to the users’ preference. Also to note down, Gen GST software is a product of utmost hard work and excellent skilled developers who have earlier given their services in the making of highly reputed taxation software i.e. Genius software, Gen XBRL etc. The GST software free download version works for PC/desktop smoothly.

Now one can also download the Gen GST Software free Demo is available absolutely free giving you insights on one of the most trusted and valuable GST software. Also, the company is giving a 10% discounton the paid version and lifetime free GST billing software available on SaaS version. The company has also decided to give GST software free download in full version with minimum conditions. The Gen GST software is ultra secured GST filing software which is developed with the most reliable JAVA language commonly used in the banking sector while the software is adaptable to any OS available or running in the market. The Gen GST software is capable of providing invoice format in excel, unlimited client return filing, GSTR 9 annual return filing with annual composition and audit form, credit ledger, cash ledger based upon data filled within the authorised format and also represents the availability of ITC Match/Mismatch report giving an error-less report result.

Steps to Download Free Gen GST Software (Trial Version for PC/Desktop)

First of all, open the https://saginfotech.com in the address bar of the browser

Click on the products tab and select GEN GST, Also you can click the topmost box to directly go to the product page

Now Click on the download free demo on the starting of the page for offline tool

After that fill the details in the orange enquiry box including Name, Email address and Mobile no. and Click send

You will receive the download link at the email address given by the interested user providing the chance for getting GST invoice software for free download

Outstanding Features of GEN GST Software (Desktop/PC):

Apart from e-filing and billing of tax, the GEN GST also provides numerous extraordinary features to its clients including,

Gen GST Online Desktop Features

GSTR 9 Annual Return Filing

GSTR 9A & 9C Annual Composition & Audit Forms

Unlimited Client Return Filing

Platform Independent

Java, Highly Secured Language

Generate, consolidate, update GST e waybill

Import Facility From Renowned Accounting Software

Creation of Masters

Industry Specific Billing Format

e-Filing

Summarized and rate wise sales figures report

Facility to export client data into excel via GST Software

Reconciliation of GSTR-3B with input credit register

Difference between GSTR 1 and GSTR 3B

Delete all data of GSTR-1 from the portal

Download all the return data from the GSTN portal on the single click

Tax system in India keeps on reforming for good. The Government and other tax-related departments are constantly working to make the tax system more rigid. One such reform is recently brought in practise by the Tax Department related to ‘Income Tax Refund’. Valid from the prevailing year onward, the one who claims Income Tax Refund has to pre-validate the bank account in which he wishes to receive the refund. Apart from that, the IT Department demands the bank accounts to be linked with the taxpayer’s PAN and if in any case the taxpayer fails to link the PAN, then the refund will not be credited in his account.

Experts say, “a taxpayer who is looking to claim the refunds must link the PAN to his bank account and also pre-validate the bank account on income tax e-filing website”. From now onward e-refund will be issued by the tax department and the refund will be credited to the bank account linked with PAN. Visit your bank branch to register your PAN with your bank account.

A Step-wise Guide to Pre-Validate your bank account:

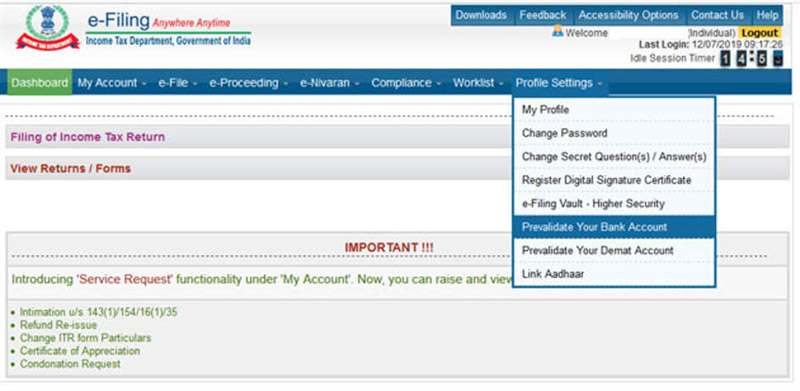

Step 1: Log in to your account on www.incometaxindiaefiling.gov.in. Your user ID is your PAN number.

Step 2: On the dashboard, select Profile Setting Tab and from the drop-down select ‘Prevalidate your bank account’ option.

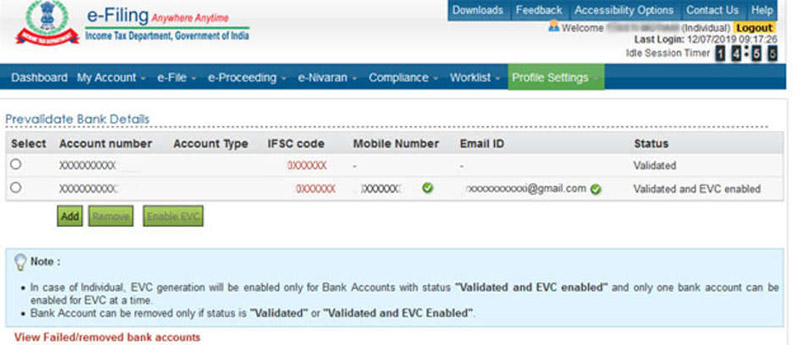

Step 3: The details of Pre-validated bank account (if any) will flash on the screen. If you don’t have a pre-validated account or if you want to pre-validate a new account, click on the ‘Add’ button.

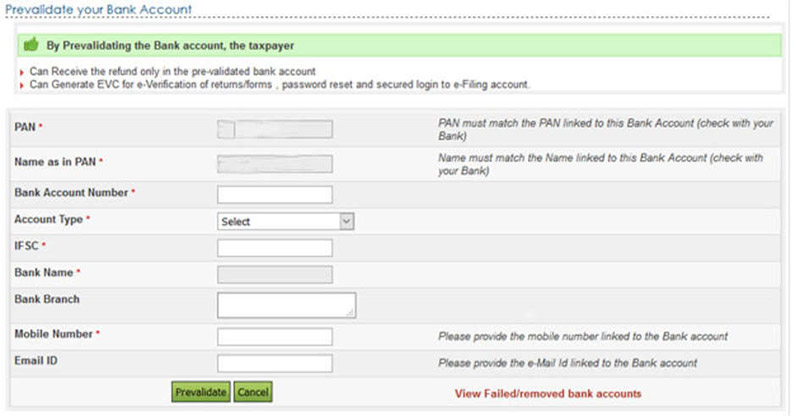

Step 4: You will land on the application form for Pre-validating the bank account. You need to fill the relevant details such as bank account number, account type, bank name, branch name, IFSC, your mobile number and your email id. Take note on the mobile number and email id as they should match with the bank records.

Step 5: As soon as you click the pre-validate button visible in the bottom of the form you will see a message saying “Your request for pre-validating bank account is submitted. Status of your request will be sent to your registered email id and mobile number”.

Quick Tips that might help you while pre-validating your bank account:

You can even check the status of your bank account by going back to Pre Validate your bank account under Profile Settings Tab. If your account is pre-validated it will appear on the screen.

In case if you want to remove a bank account, go to the ‘Pre Validate your bank account’ under Profile Settings Tab, select the account you want to remove then click on the ‘Remove’ tab.

To see the bank accounts where pre-validation has failed, you can click on ‘View Failed/removed bank accounts’ visible at the bottom of the web page. After clicking, it will display the details of the removed or rejected bank accounts with the reason for removal or rejection.

In today’s ambitious aeon, having a graduate degree is generic. To get triumph in the cut-throat competition, a postgraduate degree or a professional qualification is an ad hoc. It is like an eligibility to begin the journey to the crest of success, to become a part of esteemed organisations, to work under big names, to seize the opportunities for your own business.

For the commerce students, Chartered Accountancy (CA) and Master of Business Administration (MBA) in Finance are two of the most rewarding career paths that grow aspirants intellectually, financially & theoretically while breaking the ice for exemplary opportunities with high-income packages.

WhereChartered Accountancy is one of the most sought after and prestigious professional stream for graduate and under-graduate commerce students, Finance is also one of the most coveted options by young professionals and graduates. Both are the most demanding courses which assist in getting an edge in the industry.

Now lets us compare both the courses in terms of duration, scopes, packages etc.

Colleges and Entrance Exams:

CA is three-stage program – the Foundation course, Intermediate course, and the Final course, which is offered by the Institute of Chartered Accountants of India (ICAI) and C.P.T is the entrance exam for it. MBA in finance can be done from government universities, private colleges as well as from Foreign universities. The entrance exam for the same is the Common Aptitude Test (CAT), SNAP, MAT, CMAT, XAT, etc. Some private colleges may have different admission criteria which include their own entrance exams, management quota and merit-based admissions.

Eligibility Criteria:

For a CA aspirant, the minimum eligibility for pursuing the course is 10+2 examination (or equivalent) from an accredited board while for pursuing an MBA in Finance, the minimum eligibility is Graduation. This means one may inaugurate the avenue to become a CA professional just after his/her schools. But M.B.A can be done only after graduation.

Duration:

If one starts his/her CA journey just after the school then it will take an average duration of 4.5 years tobecome a CA professionalwhile if it begins after graduation than it takes three years of time frame. However, the time span for completing full-time MBA in Finances varies from 18 to 24 months i.e. a maximum of 2 years.

Subjects Covered:

Financial accounting and reporting, law, taxation, audit, finance, business environment and concepts, are the main subjects of CA course. Business Finance, investment banking, credit risk management, asset management, etc. are the pivotal subjects for MBA in Finance course.

A Chartered Accountants can work in accounts and finance departments of eminent firms. The wide array of career options for CA includes financial and accounting management, internal audit, taxation, statutory audit, investment decisions, banking and so on. A well-versed CA can practice the profession privately also and can impart freelancing services to the organisations. MBA in Finance unplugs career opportunities and infinite possibilities for candidates in private as well as government sectors that include financial bodies, financial consultancies and banks. Most promising and popular career scopes for MBA in Finance are accounts and finance management, investment banking, business analyst, credit management, insurance & risk management, financial analyst, etc.

Salary Packages:

An average earning of a fresher CA is approx INR 6-7 lakh per year. While an average salary package of MBA Finance graduates from top universities/colleges is around INR 10-15 lakh.

Both the courses requires diligent hard work, dedication & continuous efforts which in turn open global opportunities to work in diverse industries and MNCs.

The integration of technology with accounting is giving the edge to the companies in the digital scenarios where competition is soaring at a high pace. The company adopting the technological advancements are able to cash in on more opportunities than those who are still stuck with the conventional method of working, thinking that “Old is Gold“.

“To stay ahead, you must have your next idea waiting in the wings.” Rosabeth Moss Kanter

The companies, which accept the changes and move ahead with the advancement and innovation, automate & ease their work and attract more financial gains and organised internal functioning. Automatic intelligence is one of those innovations that automates the processes and yield remarkable results. It knocks off the monotonous and tiresome human activities and replaces it with technology that adds efficiency & accuracy and let employees invest their creativity & skills in other productive tasks.

“Opportunities are like sunrises. If you wait too long, you miss them.” William Arthur Ward

Automatic intelligence is like an opportunity which should be availed by every organisation today if it wants to move forward with the same pace as technology & other industries. One should not wait for enough to accost the latest innovations in business because that restricts you to avail the advantages it comes up with. The outmoded methods not only hamper the growth of the company but also of the employees because they keep doing the humdrum activities and learn nothing new.

Although many people are well-acquainted with the benefits of this innovation, some people still spell out Artificial intelligence, as a technology that replaces human employees. But it is not true, AI does not oust employees, rather it helps employees by reducing their tedious job and enhancing their experience, particularly in the management of Voluminous data and adjustment of Complex mutating patterns.

Recent surveys claim that above 80% of people think that AI gives competitive advantage and 79% thinks that AI boosts the company’s productivity. Nowadays many accounting firms use Artificial intelligence to analyze hefty data at a high pace which would have been very difficult for humans.

Reasons & Advantages of Introducing Artificial Intelligence with Accounting Business.

Streamline Data Entry and Analysis

The financial information of a company is stored in diversified accounts, spreadsheets and PDFs. Entering data in various files & spreadsheet and analysing them thoroughly is a time taking, a troublesome & tiresome job which is prone to errors. A human accomplishing this task may get completely baffled and may need more people to help him in this complicated job.

Artificial intelligence, here, plays a pivotal role by compiling the spreadsheet, accounts & PDFs, together and by creating & keeping the reports related to different issues separately. AI not only brings accuracy but also quickens the tasks that lead employees to focus on strategies which can lead businesses to the crest.

AI foresees long term objectives in a much more organized way, compiles past data for a comprehensive view of work accomplished and analyse the current information to bring more efficiency.

Fraud Deduction and Reduction

A business entity is exposed to internal as well as external frauds. A big company with many employees have more chances of internal fraud because every employee needs funds at different levels for different needs which is hard to be tracked by a human.

A techno deficient company can not ensure fraud-free ambience because they do not have any particular way to transfer the financial data or funds without human intervention. Here artificial intelligence plays the role of a defender. It knocks off the need to hand over the financial data to one or the other person and thus maintain confidentiality.

In addition to this, artificial intelligence audit all the expenditures at every employee’s level and so leaves no space for ambiguity. This curtails down the chances of internal fraud and leads to a safe and protected work environment.

Corporate Policy Implementation

Every business organisation has some policies to adhere to. These policies safeguard the organisation from internal and external inconvenience & abuse. The policies are formulated with an aim to maintain the financial stability of the company by combating with any disparities and errors. Artificial intelligence automates human work and so reduce their intervention in technical data. This yields correct calculations and accuracy while allocating more time to employees to focus on pivotal strategic aspects.

Most common discrepancies and lapse which results in the incurrence of the loss to the company include Purchase orders, Employ receipts, Credit card transactions, Travel bookings and so on. It is quite apparent that the companies who are lacking behind in introducing new techniques in their organisation are more inclined to risks.

Artificial intelligence comes with a vast array of benefits and infinite possibilities that includes simplification, automation, efficiency, accuracy and so on.

A well-organized method of artificial intelligence compiles the data from different sources and concludes results. For example, an AI gathers the survey to conclude the consequences of newly formulated policies of the company. So in this way, AI assists in getting reviews and better outlook about the current system.

Wrapping up: To deal with lofty demands from clients and increasing regulations, many firms are now switching on to a new type of workforce where new technologies streamline their business activities. Accounting is one of the topmost business operations and so companies today are implementing AI in accounting to ensure positive results like booming productivity, improved accuracy, and curtailed cost.

This is for the employees to notice, the due date for employers to provide Form 16 to their employees is 10 July. some might have received and if not then one must ask the authorities for the same. Another thing to keep in mind is that the form must be downloaded from TRACES.

About TRACES

TRACES stands for TDS Reconciliation Analysis and Correction Enabling System. TRACES online servicesallows registered TDS deductor or employer to download Form 16. TRACES are the detailed records of the TDS Tax Deducted at Source which allows the taxpayer to effortlessly file an income tax return.

Mandatory for Employers to Provide Form 16 to the employees only From TRACES Portal

I-T Department has already alerted the employers about downloading and generating Form 16 only from the TRACES. Now the department also wants the employees to make sure about the same.

To be remembered, the final date for the taxpayer to file an ITR is 31st July 2019. TRACES is an online application operated by Income Tax Department which facilitates the taxpayer to view and download challan status, Form 16 or Form 16A (verifying the status of TDS) and Form 26A (the annual tax credit form).

For salaried individuals, verifying Form 16 and Form 26A is mandatory. Form 16 has details of income received from the employer, TDS deducted by the employer, and other tax deductions in FY 2018-19. Form 26A has all the calculated knowledge of deducted tax by the deductor, collected tax, advance or self-assessment tax, and refunds paid by Income Tax Department.

To avoid future faults, here are the tips to check the validity of Form 16 from TRACES:

There will be a unique 7 character alphabet certificate number on original Certificate downloaded from TRACES.

The document will contain a TDS-CPS logo on the left corner and on the right corner there will be an image of the national emblem.

Form 16 Re-designed Under New Laws

Form 16 is re-designed under new laws, therefore it is important to download the new format of Form 16 from TRACES. Form 16 has two segments A and B. Segment B of Form 16 was reviewed recently by the Central Board of Direct Taxes (CBDT). CBDT has already issued a notice for the employers to issue Part-B of Form 6 to the employees received only from TRACES portal.

To be noted, Part B of Form 16 contains details of all the allowances and other requisites employer has provided to the employee.

Lastly, it is mandatory for employers to file form 24Q which requires the salary description in the last quarter of FY 2018-19.

Last four months from February to May have witnessed continuous drop-off in the number of return filings. The data count total decline of approx 8 lakh, i.e. 10% of the total GST return filed in India, in return filings in these months.

The total number of GSTR-3B filed in the month of May this year is around 75 lakh which is considerably lesser than the number of GSTR-3B required to be filed which is 1.03 crore. This apparently implies that around 1/4th of the business entities who were under obligation to file returns as per GST law didn’t do so.

When questioned by the Rajya Sabha about the measures that need tax officials to inspect the concerned business premises who failed to file GSTR, Anurag Thakur, minister of state for finance said: “The government is considering to put in place an extensive plan to hunt for these missing GST payers,”.

The total number of businesses registered under the GST is more than 1 crore, from which around 84 lakh business entities filed the returns in the month of February this year.

But in the march of the total number of GST return filers ((GSTR-3B) curtailed to 82.5 lakh. The downward trend continued in the month of April as well when the number of GST filers dwindled to 79 lakh business which further dropped over 75 lakh in the same month.

The gross GST collection by GOI (government of India) was undergoing the antrorse trend from February to April this year with the total collection of Rs 97,247 lakh crore, Rs 1,06,577 crore and the highest Rs 1,13,865 crore in the month of February, March and April respectively. But the month of May encountered sudden collapse with Rs 1,00,289 crore GST collection.

An incongruous scenario has emerged out when there is an increment by 23 lakhs in the number of businesses registered under the GST and the GST registered business gone up to 1.03 crore whereas, in the same period, the number of GSTR-3B filed decreased by more than 10% which means around 8 lakh corporate entities have been lackadaisical in filing GSTR-3B.

In such a paradoxical situation, minister of state for finance is stepping ahead with the measure to quest such defaulters of GSTR filing.

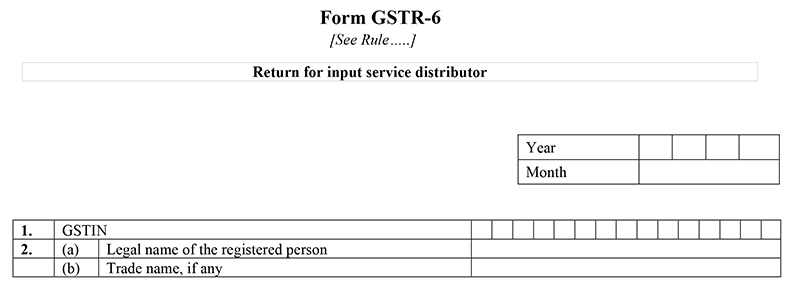

GSTR 6 Return form for all the input service distributors who have registered under the Goods and Services Tax (GST). Every Input Service Distributor (ISD) will require to furnish the details of invoices in GSTR- 6 form at GSTN portal. After correcting, modifying, removing and adding the details of form GSTR-6A, the GSTR 6 is furnished and most of the information is auto-populated. The details of the received credit taken from different invoices are covered under GSTR 6.

The due date of GSTR 6 form is 13th July 2019 for the month of June 2019. Form GSTR 6 now available to fill for Input service Distributors (ISDs) on the GST official portal.

Salient Features of GSTR 6 Return Form

The form GSTR 6 is filled by all the Input Service Distributors who are registered under the Goods and Service Tax (GST)

It should be filled by 13th of succeeding month

The taxpayer is required to furnish the details of tax invoices on which the credit has been received

Who Should File GSTR 6

All the Input Service Distributors required to file the return excluding:

Composition Dealers

Taxpayers liable to collect TCS

Taxpayers liable to deduct TDS

Suppliers of OIDAR (Online Information and Database Access or Retrieval)

Compounding taxable person

Non-resident Taxable Person

Definition of Input Service Distributor

Input Service Distributor works as an intermediary between the manufacturer businesses or final product producers. According to Rule 2(m) of Cenvat Credit Rules, 2004:

ISD is the office of the supplier of goods and /or services

The ISD receives tax invoices towards receipt of input services

It distributes credit of CGST/SGST/IGST to a supplier of goods/ services having the same PAN from office referred above

ISD issues documents or invoices for distribution of Credit

In GSTR-6, an ISD requires filling information regarding the distribution of credits. Here are the revised dates to file the GSTR-6 for the months after GST rollout:

For the Year 2017, ISD needs to file the form until 31st December 2017

For all the coming month, ISD needs to file the form before or on 13th of the succeeding month of the tax period

The Following Information Is Needed To Be Added To File GSTR 6:

Table 1&2: Details Of The Taxpayer

GSTIN: GSTIN stands for Goods and Services Taxpayer Identification Number. The GSTIN is a 15-digit number includes 2-digit state code,10-digit permanent account number, and 3-digit includes state, future use, and check-digit. It is auto-populated when we file returns.

Name of Taxpayer: This is the name of a Non-resident taxpayer owning business outside of India and supplies goods and services. This field is also auto-populated at the time of return filing.

Month-Year(Period): The taxpayer requires to choose the date from drop down for which month and year for which GSTR-6 is being filed.

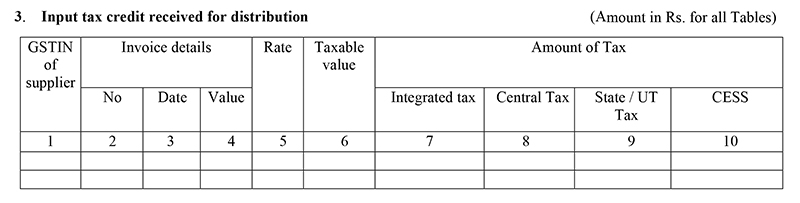

Table 3: Details Of Input Credit Received

Details Of Inward Supplies From Registered Taxpayer: ISD fills out the details of supplies received and input credit amount from a registered taxpayer. Most of the information especially inward supply details are auto-populated from GSTR-1 and GSTR-5 of the counterparty. The person has to fill all the credit covered under CGST/SGST, and IGST. If the received supplies are in more than one lot, then the taxpayer needs to mention only the last lot information

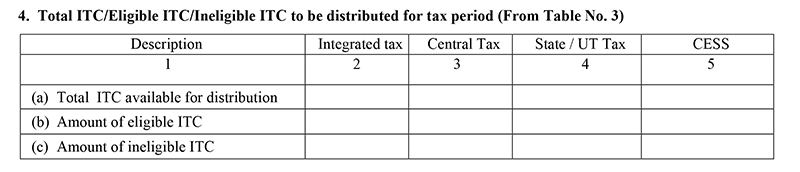

Table 4: For The Given Tax Period Eligible/ Ineligible ITC

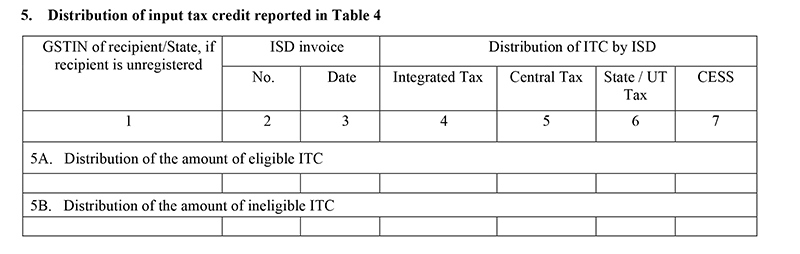

Table 5: The Available Credit Under CGST, SGST, And IGST

This head includes the information regarding the available credit under CGST, SGST, and IGST. the details in this head is of the ITC mentioned in table-4. Here we need to fill the details of the invoices to furnish the fields

Table 6: Any Changes For Table 3

Interest on Late Payment of GST Tax & Missing GST Return Due Date PenaltyModification To Details Of Inward Supplies: Taxpayer provides modified and revised invoices and information along with CGST/SGST and IGST charged if there is any modification or change to the earlier tax period

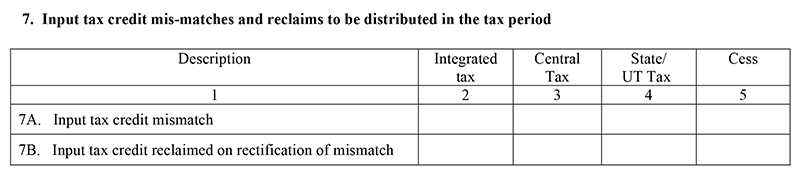

Table 7: Mismatches And Reclaims To The ITC Should Be Cleared Here

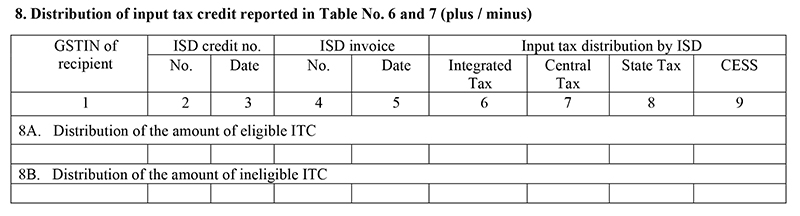

Table 8: Distribution Of The Input Tax Credit Which Is Mentioned In Table 6&7

The amount distribution for table 6 & 7 under CGST, IGST, and SGST is covered in this head

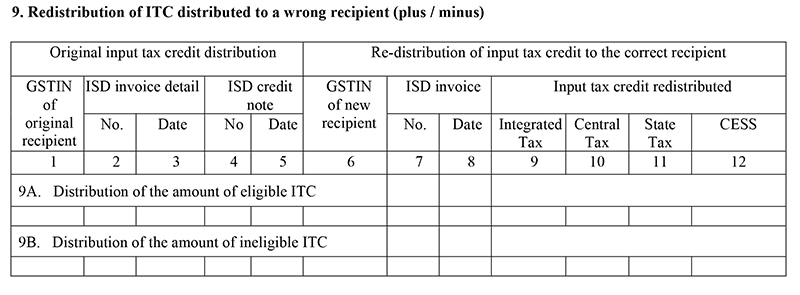

Table 9: Re-distribution If Distribution Is Done Wrong

If wrongly above mentioned tables are filled by distributed money to the wrong person, the changes and redistribution is possible under this head

Table 10: Late Fee Payable

In case of late fee payable or paid, this head is separately mentioned for it. The taxpayer fills the details in it regarding the late fee if applicable

Table 11: Refunds

As the heading suggests it covers the refund amount and information of the electronic cash ledger

At the end of filing the form, Input Service Distributor needs to sign the form electronically to verify the correctness of the information.

Interest on Late GST Payment & Missing GSTR Due Date Penalty

Among the many rules of GST, there are also rules of penalties and the late fee for the negative aspects of the implementation part, like late payment or taxes or delay in filing returns. The GST rules say that the delay in the payment of GST taxes will lead to an 18 percent annual interest rate, in which a late fee will be charged on each day for the period after the due date of tax payment. Read more details about GST interest mechanism at the URL below. https://cbec-gst.gov.in/CGST-bill-e.html

Example: As a taxpayer, if you miss the deadline of GST payment for a particular month, you will still be required to pay the tax but will also have to pay additional interest at the rate of 18% or 1000*18/100*1/365= Rs. 4.93 per day approx Where Rs. 1000 is your assumed tax liability. For each day you do not pay tax after the due date, the interest will grow by Rs. 4.93 approx.

In case if a taxpayer does not file his/her return within the due dates mentioned above, he shall have to pay a late fee of Rs. 50/day i.e. Rs. 25 per day in each CGST and SGST (in case of any tax liability) and Rs. 20/day i.e. Rs. 10/- day in each CGST and SGST (in case of Nil tax liability) subject to a maximum of Rs. 5000/-, from the due date to the date when the returns are actually filed.

General Queries on GSTR 6 Form

Q.1 What is Form GSTR-6?

GSTR-6 form is a monthly return which is required to be filed by all the Input Service Distributor’s (ISD) for the distribution of credit (ITC) among its units.

Q.2 Who is supposed to file Form GSTR-6. Is filing this form mandatory?

GSTR-6 is to be filed by only those taxpayers who are registered as Input Service Distributor (ISD). It is a mandatory return which is required to be filed on a monthly basis. In the case of no business activity, a nil return is required to be filed.

Q.3 What is the last date for filing GSTR-6 form?

We are trying to make you understand the same through an example.

The ISD return for a month, say M, could be filed on or after the 11th of month M+1 and on or before the 13th of month M+1 or the extended date if any.

Q.4 From where can a taxpayer file the Form GSTR-6?

After logging in to the Returns Dashboard, GSTR-6 form is accessible through the GST Portal.

We assist you with the path below:-

Services > Returns > Returns Dashboard

Q.5 When and where we can see the auto-populated invoices in the Form GSTR 6?

Once the Form GSTR-1/Form GSTR-5 is got successfully saved by the supplier, the auto-populated invoices would reflect in Form GSTR-6A, (Table 3 and 4) and Form GSTR 6 (Tables 3, 6A, 6B, and 6C). An action could be taken on these invoices once GSTR 1/5 form has been submitted by the supplier.

Q.6 Is it required as mandatory to take action on all invoices/CDN which have been auto-populated in Form GSTR-6?

Yes, action on a mandatory basis is required to be taken against all such invoices/CDN which have been auto-populated in your Form GSTR-6. Not doing so, would lead the taxpayer unable filing GSTR-6 Form.

Q.7 What actions could be taken on invoice data which are auto-populated in table 3 & 6 of Form GSTR-6?

The below actions could be taken for invoices or credit/debit notes against the data received in Form GSTR-6, you can take the following actions:

Accept

Reject

Modify

Keep Pending

Q.8 What all actions could be taken on invoice data auto-populated in table 6A & 6C of Form GSTR-6?

For data received in Form GSTR-6 in the invoices or credit/debit notes, the following actions could be taken;

Accept

Reject

Keep Pending

Q.9 Can one file the ISD return if their counterparties have not filed Form GSTR-1/5?

Yes, one is eligible to file the GSTR-6 return even if their counterparties have not filed their respective Form GSTR-1 or Form GSTR-5.

This could be simply done by uploading the missing invoices using the ADD MISSING INVOICE functionality and thus filing the return within the prescribed timeline.

Q.10 What would happen if Form GSTR 6 is filed before Form GSTR-1/5 and then Form GSTR-1 and Form GSTR-5 are filed?

In the case where Form GSTR-1 and Form GSTR-5 did not get filed till 10th of the succeeding month of the tax period by the counterparties, no auto-population of the B2B details would take place in Form GSTR-6A and Form GSTR-6 for that tax period.

In such a case, it is the ISD who would add the missing invoices/CDN by using the functionality – ADD MISSING INVOICE DETAILS/ADD CREDIT NOTE/DEBIT NOTE. These details would be available under “Uploaded by supplier” table. Again, the uploaded B2B details would flow directly to the Form GSTR-1/Form GSTR-5 of the suppliers.

Q.11 Is there any Offline Tool for filing Form GSTR-6?

Yes, there is an offline tool available for filing Form GSTR-6.

Q.12 Is there any late fee attached to the system in case of the delayed filing of Form GSTR-6?

Yes, as per the prescribed law there is a late fee which is required to be paid in the case where the form GSTR-6 is filed late.

Q.13 Is there a system for Electronic Credit Ledger available for ISD Registrations?

No, there is no such Electronic Credit Ledger maintained for ISD Registrants. ISD is responsible to distribute credit available during a tax period.

Q.14 Could a taxpayer mark the eligibility of ITC at the invoice-level?

No, the provision is that the eligible Input Tax Credit gets auto-updated in Table no. 4 based on the invoice/CDN uploaded (based on the action taken on the Auto drafted from Form GSTR-1/5) in Table no 3 & 6. The eligibility is required to be taken concern of only at the time of distribution of Credit to units.

Note: – Input Tax Credit (ITC) for distribution should be available only against those inward supplies where the Place of Supply (POS) and the State where ISD is registered is the same.

Q.15 Is an ISD liable to pay tax on a reverse charge basis? OR Is reverse charge mechanism applicable to ISDs?

Reverse charge liability is not applicable for an ISD.

Q.16 How could one allocate credit to his/her other units in GSTR 6 Form?

With the help of Table 5 and Table 8 of the Form GSTR-6, both eligible and ineligible ITC could be conveniently distributed to the units.

Q.17 Could Amendment be made to the credit allocated to the units in Form GSTR 6 of earlier tax periods? If yes, how?

Yes, the credit allocated to a unit in a previous tax period could be redistribute using Table 9 of the Form GSTR-6.

Q.18 Can the date of filing of Form GSTR-6 be extended?

Yes. The date of filing of Form GSTR-6 could be extended by the Government through a notification.

Q.19 What are the pre-conditions for filing GSTR-6 returns?

Pre-conditions for the filing of Form GSTR-6 are:

The recipient should have been Registered as ISD and must be retaining an active GSTIN.

The Recipient should be having valid login credentials (i.e., User ID and password).

It is required that the Recipient should have a valid and non-expired/ unrevoked Digital Signature Certificate (DSC which is mandatory for companies, LLPs and FLLPs).

It is required that the Recipient should an active mobile number which is mentioned in his registration details at the GST Portal at the time of enrolment/ registration or amendment thereof for authentication through EVC.

The recipient would be given an option to file Form GSTR-6 for a canceled GSTINs for the period in which it was active.

Q.20 What happens after Form GSTR-6 is filed?

Let us look broadly for what happens after the Form GSTR-6 is filed:

On successfully filing of the Form GSTR-6 Return an ARN is generated.

An SMS and an email for acknowledgment sent to the applicant on his registered mobile and email id.

In case, if there is any modification or addition made in Form GSTR-6, these modified details are auto-populated in Form GSTR-1//5 of counterparty supplier.

Q.21 What are the modes of signing Form GSTR-6?

Form GSTR-6 could be filed using DSC, or EVC.

Digital Signature Certificate (DSC)

Digital Signature Certificates (DSC) are the digitized forms of physical or paper certificates. A Digital certificate presented electronically could prove one’s identity. It is also used to access the information or services available on the internet and to sign certain documents digitally.

It is important to know that in India, Digital Signature Certificates (DSCs) are issued by authorized Certifying Authorities.

The GST Portal is designed such that it accepts only PAN-based Class II and III DSC.

Electronic Verification Code (EVC)

The Electronic Verification Code (EVC) is aided to authenticate the identity of the user at the GST Portal. EVC does this by generating an OTP. The OTP is sent to the registered mobile phone number of the Authorized Signatory filled in part A of the Registration Application.

Q.22 Could the Form GSTR-6 be previewed before submission?

Yes, we can preview the Form GSTR-6 before submitting it on the GST Portal.

Gen GST is the best and ultra-secure GST software created by SAG Infotech Pvt Ltd to simplify and accelerate the taxation procedures such as return filing, invoice generation, ITC claims and so on.

Gen GST software comes in three variants – Desktop offline and mobile & cloud online variants. One can easily download and use the desktop variant of the software on a compatible PC or laptop, while the online version is platform- independent and can be accessed and used anywhere anytime.

The mobile app is also available and accessible at just a little additional amount. All the variants are completely reliable, safe and confidential, backed with the restoration of up to the minute data. An integrated feature in the software lets you upload data directly to the GST portal.

With the price as low as Rs. 5,000 for the desktop version, Gen GST is envisioned as the most affordable and best GST billing software for all your taxation needs. It is attuned with Statutory Compliances and gets well-updated with latest government amendments and notifications.

A vast array of its innovative solutions includes – Invoice (Sale & Purchase) for Goods & Services, Import-Export Facilities, e-Filing, GST E Waybill, and so on. Here we shall discuss Invoicing for Goods and Services.

Gen GST Billing Software is a complete solution for automating all billing and invoicing related work while ensuring accuracy and alacrity.

Unique Features of Gen GST Billing Software

Gen GST is a complete and the only GST billing solution you will ever need. You can use the software for creating all types of GST compliant bills & invoices, e-way bills, etc. in an easy and hassle-free manner. Here’s why Gen GST is the best GST billing and invoicing software.

Customized Billing

Customized billing opens avenues for easy, quick and economical invoicing for the taxpayer with user convenient interface.

Digitally Signed Invoices

Invoices are attested with digital signatures and they get dispatched directly to the customers.

Bill Book Feature

Bill Book facility in the software maintains and updates records and transactions accurately and timely.

Bill Generation Facility

Bill is generated automatically or manually with the bill number of the client’s choice.

Purchase Invoice for Unregistered Dealers under RCM

The software maintains a separate list of dealers under RCM and generates purchase RCM invoice for them.

Mailing facility to the Customers

Gen GST offers an immediate mailing service every single time an invoice is generated.

Advance Receipt

The software can prepare the receipt and compute GST on it in advance.

Debit Credit Note

Software prepares and maintains reports on invoices, credit notes, debit notes, credit notes and revised invoices of purchase & sales.

Refund Voucher

The software allows you to get refund vouchers from clients and assure you to maintain refund timeline.

Industry-based Billing Format

Create billing software according to the Industry’s compliance with GST norms.

Other notable features of Best GST Billing Software include:

Bulk SMS/Email Facility to Clients

With this feature, one can directly inform unlimited clients about Returns status through emails and messages.

Instant Registration

Instant Registration facility for every taxpayer whether its Regular, Composition or Practitioner under GST with govt accredited forms.

Unique Client Authentication Tool

Unlimited password for unlimited clients. Every taxpayer will have his/her own password for any alterations in tax-related data.

e-Payment

Secure single click online payments for GST returns, TDS & taxes while maintaining Challan Register and Challan Printing.

To find complete information about the best GST billing software (Gen GST), download a free demo now!