The GST Council, along with the government, has accepted a new set of GST return forms with the aim to remove the ongoing issues and simplify the overall return process. The new forms would be implemented from 2019.

A number of changes have been made in the new GST forms, which are being explained here. Source: Harpreet Singh, Partner at KPMG India.

Five Major Changes in the Upcoming GST Returns

- The first change is in the form of a reduced number of returns. The Council has decided to replace the existing multiple returns with a single return filing. So now, there would be one return filing against multiple returns which are filed presently. As of today, we file multiple returns, including GSTR-1, GSTR-3B, GSTR-2A (for reconciliation purpose), etc. All these will be replaced with one return form.

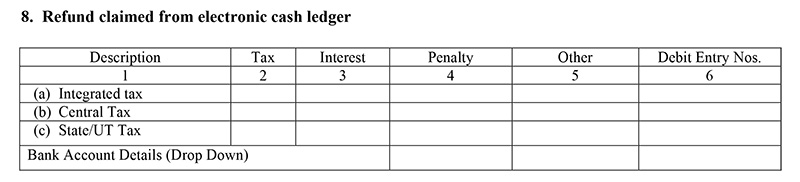

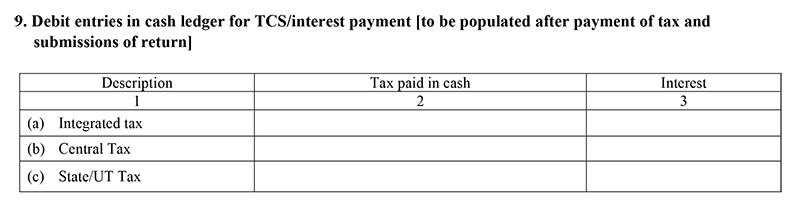

- The new return will be simpler than what we have today. The simpler return will only have 5 to 6 tables, one of which will contain details of supply and one is for purchase/input details. Another benefit is that the information in both these tables will be auto-populated, based on the invoices uploaded by the taxpayers. Around 80% of the tables will auto-fetch data from invoices. The dealer will only have to fill the remaining 20% details.

- Another change is a new return filing method through SMS. The portal will soon start the facility to allow taxpayers to file their GST returns through SMS.

- Also, there is a change in the way dealers could amend their returns. As of today, there is no provision to amend a return once it is filed. Upon receiving several requests from dealers for introducing a provision for amendments, the Council has decided to do it. The new return filing system would allow taxpayers to amend each of their returns twice and also report negative balance or liability.

- The new system will have profile-based dealer’s filing of returns. That means a dealer’s profile will be selected based on which they will fill out a questionnaire and proceed to file the return.

Singh summarizes the new return as “upload – lock – pay” system where suppliers upload their invoices (and provide return details), the recipients accept them and thus lock the returns and then the GST is paid.

As for the Sahaj and Sugam schemes, Singh goes on explaining that the option is for dealers whose annual turnover is less than 5 crores and file quarterly returns. Such dealers can either continue with quarterly returns or they can opt for a simpler two return system – one is Sahaj return and another one is Sugam return.

Read Also: Free Download Gen GST Software for Simple GST Return Filing

Sajah return is for B2C suppliers. It is a much simpler return with less number of fields and easy to file. It will be filed monthly. Sugam is for those dealers who are involved in both B2B and B2C supplies. Rest process is the same. The Sajah and Sugam option are only available to dealers with less than 5 crore turnover.

Source: https://economictimes.indiatimes.com/

{kind=link}